International Financial Reporting Standard (IFRS) – 10

CONSOLIDATED FINANCIAL STATEMENTS

1. Scope of IFRS 10

IFRS 10 addresses the scope of consolidated financials statements and the procedures for their preparations. The scope of IFRS 10 covers:

1. The reporting entities (investor / parent entities) that are required to assess control of their investees (subsidiary entities)

2. The investees that the control assessment is applied to

3. Circumstances in which the parent entities are exempt from presenting consolidated financial statements.

The companies which are exempted from presenting consolidated financial statements are:

a. Intermediate parent entities that meet the following conditions:

i. It is a wholly owned subsidiary or is a partially owned subsidiary and all its owners, including those not otherwise entitled to vote, have been informed about, and do not object to, the parent not presenting consolidated financial statements,

ii. Its securities are not publicly traded,

iii. It is not in the process of issuing securities in public securities market, and

iv. Its ultimate or any intermediate parent produces financial statements that are available for public use and comply with this IFRS, in which subsidiaries are consolidated or measured at Fair Value Through Profit or Loss (FVTPL) in accordance with this IFRS.

The following companies have exceptions to consolidated financial statements:

a. The parent entities that are investment entities and they are required to measure all of their subsidiaries at FVTPL.

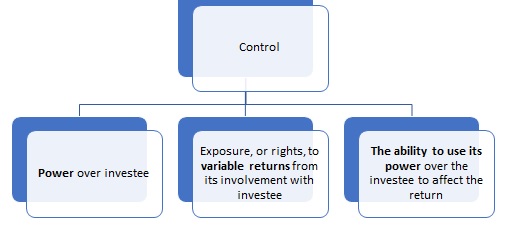

2. Definition of Control

IFRS 10 provides a single model for assessing whether ‘investor controls an investee’.

Three elements of control :

Power: Power is defined as existing rights that give the current ability to direct the relevant activities of the investee. There is no requirement for that power to have been exercised.

Examples of Relevant activities:

1. Selling and purchasing of goods or service

2. Managing financial assets

3. Selecting, acquiring or disposing of assets

4. Researching and developing new products or processes

5. Determining a funding structure or obtaining funds

In some cases, assessing power is straightforward, for example, where power is obtained directly and solely from having the majority of voting rights or potential voting rights, and as a result the ability to direct relevant activities.

In other cases, assessment can be done by considering following factors:

1. Rights in the form of voting rights (or potential voting rights) of an investee

2. Rights to appoint, reassign or remove members of an investee’s key management personnel who have the ability to direct the relevant activities

3. Rights to appoint or remove another entity that directs the relevant activities

4. Rights to direct investee to enter into, or make any changes to, transactions for the benefit of the investor

5. Other rights (such as decision-making rights specified in a management contract) that give the holder the ability to direct the relevant activities.

An investor can have power over an investee even where other entities having significant influence or other ability to participate in the direction of relevant activities.

Potential Voting Power:

An entity may own share warrants, share call options, or other similar instruments that are convertible into ordinary shares in another entity. If these are exercised or converted, they may give the entity voting power or reduce another party’s voting power over the financial and operating activities of the other entity. The existence and effect of potential voting rights, including potential voting rights held by another entity. Potential voting rights are considered only if the rights are substantive. (The holder must have the practical ability to exercise the right).

Returns:

An investor must have exposure, or rights, to variable returns from its involvement with the investee in order to establish control.

This is the case where the investor’s returns from its involvement have the potential to vary as a result of the investee’s performance.

Returns may include:

1. Dividends

2. Remuneration for servicing an investee’s assets or liabilities

3. Fees and exposure to loss from providing credit support

4. Returns as a result of achieving synergies or economies of scale

3. Reporting Dates

In most of the cases, all the group companies will prepare accounts to the same reporting date. One or more subsidiaries may, however, prepare accounts to a different reporting date from the parent.

In such cases the subsidiary may prepare additional statements to the reporting date of the rest of the group, for consolidation purposes. If this is not possible, the subsidiary’s accounts may still be used for the consolidation, provided that the gap between the reporting dates is three months or less.

Where a subsidiary’s accounts are drawn up to a different accounting date, adjustments should be made for the effects of significant transactions or other events that occur between the date and the parent’s reporting date.

4. Uniform Accounting Policies

Consolidated financial statements should be prepared using uniform accounting policies for like transactions and other events in similar circumstances.

Adjustments must be made where members of a group use different accounting policies, so that their financial statements are suitable for consolidation.

5. Date of Inclusion / Exclusion

IFRS 10 requires results of subsidiaries to be included in the consolidated financial statements from:

a. The date of ‘acquisition’, i.e. the date on which the investor obtains control of the investee, to

b. The date of ‘disposal’, i.e. the date the investor loses control of the investee.

Once an investment is no longer a subsidiary, it should be treated as an associate under International Accounting Standard 28 (Investments in Associates and Joint Ventures) (if applicable) or an investment under IFRS 9 (Financial Instruments)

6. Consolidation Process

i. Basic Procedures

The financial statements of a parent and its subsidiaries are combined on line-by-line basis by adding together like items of assets, liabilities, equity, income and expenses. The following steps are then taken, in order that the consolidated financial statements should show financial information about the group as if it was a single entity.

a. The carrying amount of the parent’s investment in each subsidiary and the parent’s portion of equity of each subsidiary are eliminated or cancelled.

b. Non – controlling interests in the net income of consolidated subsidiaries are adjusted against the group income, to arrive at the net income attributable to the owners of the parent.

c. Non-controlling interests in the net assets of consolidated subsidiaries should be presented separately in the consolidated statement of financial position.

Other matters to be taken into consideration are:

a. Goodwill on consolidation should be dealt with according to IFRS 3 (Business Combination)

b. Dividends paid by a subsidiary must be accounted for

ii. Cancellation

For simple understanding, the preparation of a consolidated statements of financial position consists of two procedures:

a. Take the individual accounts of the parent company and each subsidiary and cancel out items which appear as an asset in one company and a liability in another,

b. Add together all the uncancelled assets and liabilities throughout the group.

Items requiring cancellation include:

a. The asset ‘investments in subsidiary companies’ which appears in the parent company’s accounts will be matched with the ‘share capital’ in the subsidiaries’ accounts.

b. There may be intra – group trading within the group. For example, Subsidiary co. may sell goods on credit to Parent co. Parent co. would then be a receivable in the financial statements of Subsidiary co., while Subsidiary co. would be a payable in the financial statements of Parent co.

iii. Part Cancellation

An item may appear in the statements of financial position of a parent company and its subsidiary, but not at the same amounts.

a. The parent company may have acquired shares in the subsidiary at a price greater or less than their par value. The asset will appear in the parent company’s accounts at cost, while the liability will appear in the subsidiary’s accounts at par value. This raises the issue of goodwill, which is dealt in IFRS 3 (Business Combination)

b. Even if the parent company acquired shares at par value, it may not have acquired all the shares of the subsidiary (so the subsidiary may be only partly owned). This raises the issues of non-controlling interests, which is also dealt in IFRS 3 (Business Combination).

c. The intra-group trading balances may be different because of goods or cash in transit.

d. One company may have issued loan stock of which a proportion only is taken up by the other company.

iv. Dividends Paid by Subsidiary

Dividends paid by subsidiary company to parent company should be fully cancelled while preparing consolidated financial position.

Example: Subsidiary co (S co), a 60% subsidiary company of Parent co (P co), pays dividend of $ 1,000. Its total reserves before paying dividend stood at $ 5,000.

Treatment:

a. $ 400 (40% of dividend paid by S co) of the dividend is paid to non-controlling shareholders. The cash leaves the group and will not appear anywhere in the consolidated statement of financial position.

b. The parent company receives $ 600 of the dividend, debiting the cash and crediting profit or loss account. This will be cancelled on consolidation.

c. The remaining balance of retained earnings in S co ’s statements of financial position {$4,000 ($5,000 – $ 1,000)} will be consolidated in normal way. The group’s share $ 2,400 (60% of $ 4,000) will be included in group retained earnings in the statement of financial position, the non-controlling interest share $1,600 (40% of $ 4,000) will be credited to the non-controlling interest account in the statement of financial position.

v. Unrealised Profit

Any receivable / payable balances outstanding between group companies are cancelled on consolidation. No further problem arises if all such intra-group transaction are undertaken at cost, without any mark-up for profit.

The objective of consolidated accounts is to present the financial position of several companies as that of single entity. This means that in a consolidated statement of financial position the profits recognized should be those earned by group. Therefore, the mark-up for profit made by Parent co. to Subsidiary Co or vice versa should be cancelled and the transaction should be recorded at cost at the time of consolidation.

Author Bio