The Institute of Chartered Accountants of India (ICAI) has barred Chartered Accountant Vishal Chandra Gupta from practice for six months after finding him guilty of professional misconduct under the Chartered Accountants Act, 1949. The ICAI Disciplinary Committee took action under Section 21B(3) following a complaint regarding a certificate issued by Gupta about the utilization of IPO proceeds by a company.

The Committee noted that Gupta issued a certificate on 30 May 2015 which provided contradictory information compared to the audit report issued on the same date. The audit report contained a qualified opinion, but the certificate failed to mention that it should be read in conjunction with the audit report. The certificate also failed to highlight significant discrepancies in the utilization of IPO funds, including a variance of ₹1,479.32 lakh between the amount proposed in the prospectus and actual utilization. The Committee observed that the certificate contained distorted information that could mislead investors about the company’s financial position.

In his written representation, Gupta denied gross negligence, arguing that he diligently performed his professional duties and that the certificate was not a utilization certificate but only shared limited extracts from the audited balance sheet. He also requested leniency, citing the stress caused by six years of disciplinary proceedings.

Despite his submissions, the Committee held Gupta responsible for professional misconduct, emphasizing that Chartered Accountants are expected to exercise utmost care and integrity in their professional duties. The order, dated 16 May 2024, requires the removal of Gupta’s name from ICAI’s register of members for six months as a penalty.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

[PPR/13/57/2017-DD/356/INF/2017-DC/1253/2019]

In the matter of:

CA. Vishal Chandra Gupta

MEMBERS PRESENT:

DATE OF HEARING : 19th MARCH, 2024

DATE OF ORDER : 166 May,2024

1. That vide Findings dated 05.02.2024 under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Disciplinary Committee was inter-alia of the opinion that CA. Vishal Chandra Gupta (hereinafter referred to as the Respondent”) is GUILTY of Professional Misconduct falling within the meaning of Clauses (7) and (8) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

2 That pursuant to the said Findings, an action under Section 218(3) of the Chartered Accountants (Amendment) Act, 2006 was contemplated against the Respondent and a communication was addressed to him thereby granting an opportunity of being heard in person/ through video conferencing and to make representation before the Committee on 19th March 2024

3. The Committee noted that on the date of hearing on 19th March 2024, the Respondent was not present at the appointed time, despite the fact that a notice intimating the date, time and venue of the meeting was duly served upon him through speed post and email. However, the Committee noted that the Respondent had submitted written representation dated 27th February 2024 on the Findings of the Committee, which, inter-alia, are given as under:

4. The Committee considered the reasoning as contained in the Findings holding the Respondent Guilty of Professional Misconduct vis-à-vis written representation of the Respondent. The Committee noted that the issues/ submissions made by the Respondent as aforestated have been dealt with by it at the time of hearing under Rule 18.

6. The Committee held that the Respondent issued a certificate that provided wrong and misleading information about utilization of IPO proceeds by the Company and failed to appropriately point out the discrepancies in the utilization of IPO proceeds by the Company. The Committee noted that actual utilization of IPO proceeds was significantly different from the certificate issued by the Respondent and that the utilization certificate issued by him was not true, and contained information in a distorted manner which might mislead the decision of the

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

7. Accordingly, the Committee was of the view that the ends of justice would be met if punishment is given to him in commensurate with his Professional Misconduct.

CONFIDENTIAL

DISCIPLINARY COMMITTEE “BENCH — IV (2023-2024)1

Constituted under Section 21B of the Chartered Accountants Act, 19491

File No.: 1PPR/P/57/2017-DD/356/INF/2017-DC/1253/20191 In the matter of:

CA. Vishal Chandra Gupta, New Delhi in Re:

CA Ranjeet Kumar Agarwal, Presiding Officer (in person)

Shri Jiwesh Nandan, I.A.S. (Retd.), Goevrnment Nominee (in person)

Ms. Dakshita Das, I.R.A.S. (Retd.), Government Nominee (in person)

CA Mangesh P Kinare, Member (through VC mode)

DATE OF FINAL HEARING : 26th December 2023

PARTIES PRESENT:

Respondent : CA. Vishal Chandra Gupta (through VC) :counsel for Respondent : Adv. Bhaskar Bhardwaj (through VC)

1. Background of the Case:

investigation in the matter of IPO of M/s Tarini International Limited (`Company’) was conducted by the Informant Department and pursuant to investigation, it was inter alia observed that the Company did not utilize the IPO proceeds for the purpose of objects stated in the prospectus and diverted the IPO proceeds to various entities through group companies and other entities. The Respondent was the Statutory Auditor of the Company and had audited its financial statements and issued his audit report for the Financial Year 2014-15 on 30th May 2015. The Respondent had also issued a certificate on 30th May 2015 certifying the utilization of IPO proceeds received by the Company.

2.1 During the investigation, it was observed that the Respondent, being the Statutory Auditor of the Company, had issued a certificate dated 30th May 2015, certifying that the Company had incurred Rs. 1630.98 lakhs out of IPO proceeds for the purpose of objects stated in the prospectus. It was observed that the actual utilization of IPO proceeds for the purpose of objects stated in the prospectus, ascertained pursuant to the investigation, was significantly different from the certificate issued by the Respondent. Thus, it was observed that the certificate issued by the Respondent, certifying the utilization of IPO proceeds by the Company, was not true and the same was misleading and contained information in distorted manner which might influence the decision of the investors.

3. The relevant issues discussed in the Prima facie opinion dated 28th August 2018 formulated by the Director (Discipline) in the matter in brief, are given below:

3.1 On perusal of the certificate dated 30th May 2015, it was noted that the Respondent had stated therein that ‘he had examined the audited accounts of the subject Company with reference of utilization of the proceeds of public issue and based upon his examination of books and explanation and information provided to him, he certified the expenditure incurred by the Company out of proceeds of public issue’. Thus, it was apparent from the contents of the certificate that the same was based upon audited financial statements, which itself was certified / audited by the Respondent on the same day i.e., on the day of issuing certificate.

“We draw attention to the note 30 of the financial statements whereby the holding Company has raised the money by way of Public Issue, during the year. Further; there has been variation in the utilisation of money, between the objects of public issue contained in the prospectus and actual utilisation, which was needed to be authorised from the members. In view of this, we are unable to comment upon the appropriateness of variation in utilisation of money by holding company.”

3.4 It was observed that the allegations received from SEBI percolates from the fact that they had sought an explanation from the Respondent as to the basis of his certification but the Respondent in his reply to them, had been able to produce evidence in respect of utilization to the tune of Rs. 151.60 lakhs only which was at variance with the amount mentioned in certificate. for Rs. 1630.98 lakhs. Thus, considering an overall view of the facts and circumstances of the case, it was difficult to accept the explanation of defence taken by the Respondent as there were some irregularities in the actual amount utilised which was at variance with the certification done by the Respondent. Therefore, on this aspect, it was felt that the matter required to be lbokbd into for further investigation.

3.7 The Director (Discipline) in his Prima Fade Opinion dated 28th August 2018 opined that the Respondent was Guilty of Professional Misconduct falling within the meaning of Clause (7) and (8) of Part — I of the Second Schedule to the Chartered Accountants Act, 1949. The said Clauses of the’ Schedule to the Act, states as under:

Clause (8) of Part I of the Second Schedule:

“A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct if he:

(8)fails to obtain sufficient information which is necessary for expression of an opinion, or its exceptions are sufficiently material to negate the expression of an opinion.”

4. Date(s) of Written submissions/Pleadings by parties:

5. Further written submissions filed by the Respondent:

5.1 The Committee noted that the Respondent vide letters dated 29th June 2020 and 2191 December 2023 had made additional written submissions. The Committee noted the Respondent’s submissions stating that while issuing the certificate of utilization of IPO proceeds,. he had considered the definition of ‘Working Capital’ and ‘General Corporate Purposes’ as per relevant Guidance Note issued by ICAI and Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations 2009 respectively. The Respondent submitted that while issuing the certificate of utilization of IPO proceeds, he had considered the definition of ‘Working Capital’ as per the Guidance Note on terms used in Financial Statements GN(A) 5 issued by ICAI which states that the “working capital is funds available for conducting day-to-day operations of an enterprise. Also, represented by the excess of current assets over, current liabilities including short term loans” and the definition of “General Corporate Purposes” as per the Regulation 2(na) of the SEBI (ICDR) Regulations is “General Corporate Purpose include such identified purposes for which no specific amount is allocated or any amount so specified towards General Corporate Purpose or any such purpose by whatever name called, in the draft offer document filed with the Board. According to the proviso to the said clause, any issue related expenses shall not be considered as a part of General Corporate Purpose merely because no specific amount had been allocated for such expenses in the draft offer document filed with the Board”. The Respondent further submitted that GM, SEBI vehemently failed to consider these definitions while alleging that the actual utilization was lower than the amounts mentioned in the certificate. These definitions, in fact, were the basis of working of actual utilization of IPO funds as stated in the certificate when compared with the proposed utilization as per the Prospectus as there were no specific accounting heads such as “Working Capital” and “General Corporate Purpose” in any accounting framework.

5.3 The Respondent further added that the amounts in the certificate dated 30th May 2015 were amounts actually utilized / incurred and duly recorded in the books of account based on supporting documents and vouchers. Therefore, there was no variance. As regards the inter read variance, the same was given in comparative tabular, form, which was self-explanatory. and had more clarity for any literate user / investor. The Respondent stated that the certificate dated 30th May 2015 was not included in the Annual Report. The director’s report, however, on Page 15 of the Annual Report contained the table of “Disclosure in respect of the utilization of funds in terms of the Prospectus” showing the comparative figures of proposed and actual utilization of IPO proceeds along with a note that ‘the Statutory Auditor has qualified his report on this account. Your directors have given their reply regarding this qualification elsewhere in this report’. Therefore, the reason given that there’ was no mention of qualification as marked by the Respondent in. Audit Report, – was unfounded, baseless and without any substance as such allegation’s Percolates from the imagination that the certificate was included in the Annual Report, and which might influence the decision of investor.

5.6 The Respondent in respect to the issue pertaining to details of qualification given in the Audit Report with reference to the Note 28 and 30 in standalone I consolidated accounts submitted that the CARO notified on 10th April 2015 had done away with the requirement of reporting on the end use of money raised by public issues. However, he had applied his professional skepticism and during the audit procedures, noted the variation in the heads and accordingly, qualified his audit report for variation in utilization of money so raised regarding the objects of IPO. The Company had made a disclosure in Note no. 28 of its financial statements for the FY 2014-15 in respect of listing of its fully subscribed shares which was referred to in the basis for qualified opinion paragraph in Auditors report. The Respondent stated that it was a pertinent fact that the GM, SEBI did not raise any concern about the audited accounts, or the audit report issued thereupon.

6.1 The Informant vide letter dated 09th March 2020 stated that the adjudication proceedings were approved against the Respondent firm (i.e., VCG & Co.) and the Respondent in the subject matter by the competent authority of SEBI and adjudication order dated 20th February 2020 had been passed. The Informant provided the copy of said order dated 20th February 2020 wherein the competent authority of SEBI had imposed a penalty of Rs 15,00,000/-(Rupees Fifteen Lakh only) on the Respondent firm (i.e., VCG & Co.) and the Respondent jointly and severally in terms of section 15HA of the SEBI Act, for the violation of the provisions of section 12 A (a), (b) and (c) of the SEBI Act, 1992 and Regulations 3 (a), (b), (c), (d), 4(1), 4 (2)(f), 4(2)(k) and 4(2)(r) of the PFUTP Regulations.

7.1 The details of the hearing(s) fixed and held/adjourned in said matter is given as under:

| Particulars | Date of meeting(s) | Status |

| 1st time | 02nd May, 2023 | Part heard and adjourned . |

| 2nd time | 14th December, 2023 | Part heard and adjourned. |

| 3rd time | 26th December, 2023 | Hearing concluded and decision taken |

7.2 On the day of first hearing on 02″ May 2023, the Committee noted that the Respondent along with his Counsel; were present through Video Conferencing Mode. Thereafter, the Respondent was put on oath and the Committee enquired from the Respondent as to whether he was aware of the charges; and the same as contained in Para 2 above, were also read out. The Respondent replied that he is aware about the charges but pleaded ‘Not Guilty’ on the charges levelled against him. Thereafter, in view of Rule 18(9) of the Chartered Accountants (Procedure of Investigation of Professional and Other Misconduct and Conduct of Cases). Rules, 2007, the Committee adjourned the case to a later date and accordingly, the matter was part heard and adjourned.

7.3 On the next date of hearing on 14th December 2023, the Committee noted the presence elite Respondent along with his Counsel through video-conferencing mode. The Committee asked the Counsel to present his submissions in the matter. The Counsel for the Respondent submitted that the Respondent was Statutory Auditor of the Company, and he had audited the financial statements of*the Smpany oncl,ton the same date, he had issued the certificate in respect of utilization of IPO proceeds of the Company. He further submitted that in the certificate, the Respondent had clearly stated that this was based upon the audited financial statements of the Company, and hence the certificate should be read along with the financial statements. After considering the submissions of the Counsel for the Respondent, the Committee directed him to file his reply / submissions on four points, within 10 days, viz., the qualification given in the independent audit report, the certificate issued by him where thi actual utilizatiOn certified by him was not in consonance with the report of the investigation done by the SEBI, contradictions coming in the audit report and the subsequent certificate issued by him and the order of the Adjudicating Authority imposing some penalty and the order of Securities Appellate Tribunal (SAT). Thus, the matter was part heard and adjourned to a later date.

7.4 On the day of final hearing on 26th December 2023, the Committee noted the presence of the Respondent along with his Counsel though video conferencing. Thereafter, the Committee asked the Counsel for the Respondent to present his submissions. The Counsel submitted that the certificate issued by the Respondent was not a utilization certificate. It was a replica of the contents reproduced in the audit report. It was neither a fresh certificate nor a certificate issued for any other purpose. Secondly, the prospectus issued for raising IPO was with regard to the completion of projects for which long-term capital was required.

7.5 After detailed deliberations, and on consideration of the facts of the case, various documents / material on record as well as the oral and written submissions, the Committee concluded the hearing in the instant case.

8.1 The Committee after considering the submissions made by the Respondent, thoroughly examined the charges, and noted that the Respondent had audited the financial statements of the Company for the Financial Year 2014-15 and issued the audit report dated 30th May 2015 on those financial statements. The Committee also noted that the Company came out with an IPO for public issue of 39,78,000 equity shares of face value of Rs. 10 each at a price of Rs. 41 per share aggregating to Rs. 16,30,98,000/- on 26th June 2014. The Committee noted that on investigation conducted by SEBI to ascertain whether IPO proceeds were utilized for the objects other than those mentioned in the prospectus, SEBI concluded that the actual utilization was significantly different from the certificate dated 30th May 2015 issued by the Respondent. In this regard, the Committee also took into consideration the order of learned Adjudicating. Officer of the Securities and Exchange Board of India (SEBI) bearing reference no. OrderNV/JR/2019-20/6885-6886 dated 20th February 2020 imposing a penalty of Rs. 15 lakh on the Respondent and Respondent firm, jointly and severally, for violation of provisions of Section 12A (a), (b) and (c) of the SEBI Act, 1992 and Regulations 3 (a), (b),. (c), (d), 4(1), 4(2)(f), (k) and (r) of the SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003.The Committee also noted that the Respondent and Respondent firm had filed an appeal before the Securities Appellate Tribunal, Mumbai against the afore-said order of the learned Adjudicating Officer of the Securities and Exchange Board of India. The Committee noted that the Securities Appellate Tribunal, Mumbai vide its order dated 12.10.2022 set aside the above-said order of learned Adjudicating Officer of the Securities and Exchange Board of India. In this regard, the Committee took note of Para 15 of the order of the Securities Appellate Tribunal, Mumbai, which reads as under:

8.2 The Committee observed that Securities Appellate Tribunal, Mumbai vide its order dated 12.10.2022 while holding that there was no deceit or inducement, also concluded that the appropriate authority to take action against the Respondent and Respondent firm .for professional lapse; or negligence is ICAl; and that ICAI is holding the Inquiry in, the matter based on the reference made by SEBI. The Committee ex0mined.-theifindingedpf the investigation report of the SEBI in the subject matter:; The Committee noted that Para 3 of the findings of the reports of the investigation reports the variations in the total amount proposed to be utilized as stated in the prospectus with the amount certified by the Statutory Auditor and as ascertained by the SEBI pursuant to its investigation. The said reporting done by the SEBI is reproduced below:

8.5 The Committee then examined the audit report pertaining to Financial Year 2014-15 issued by the Respondent. The Committee noted that in the audit report, the Respondent had given the qualified opinion and one of basis under basis for qualified opinion, reads as under:

“(b) We draw attention to the note 28 of the financial statements whereby the Company has raised the money by way of Public Issue, during the year. Further, there has been variation in the utilization of money, between the objects of public issue contained in the prospectus and actual utilization, which was needed to be authorized from the members. In view of this, we are unable to comment upon the appropriateness of variation in utilization of money.”

8.7 The Committee thereafter considered the allegation that the certificate issued by the Respondent certifying the IPO proceeds of the Company was not true and was misleading; and in this context, it examined and took note of the contents of the certificate dated 30th May 2015 issued by the Respondent which reads as under:

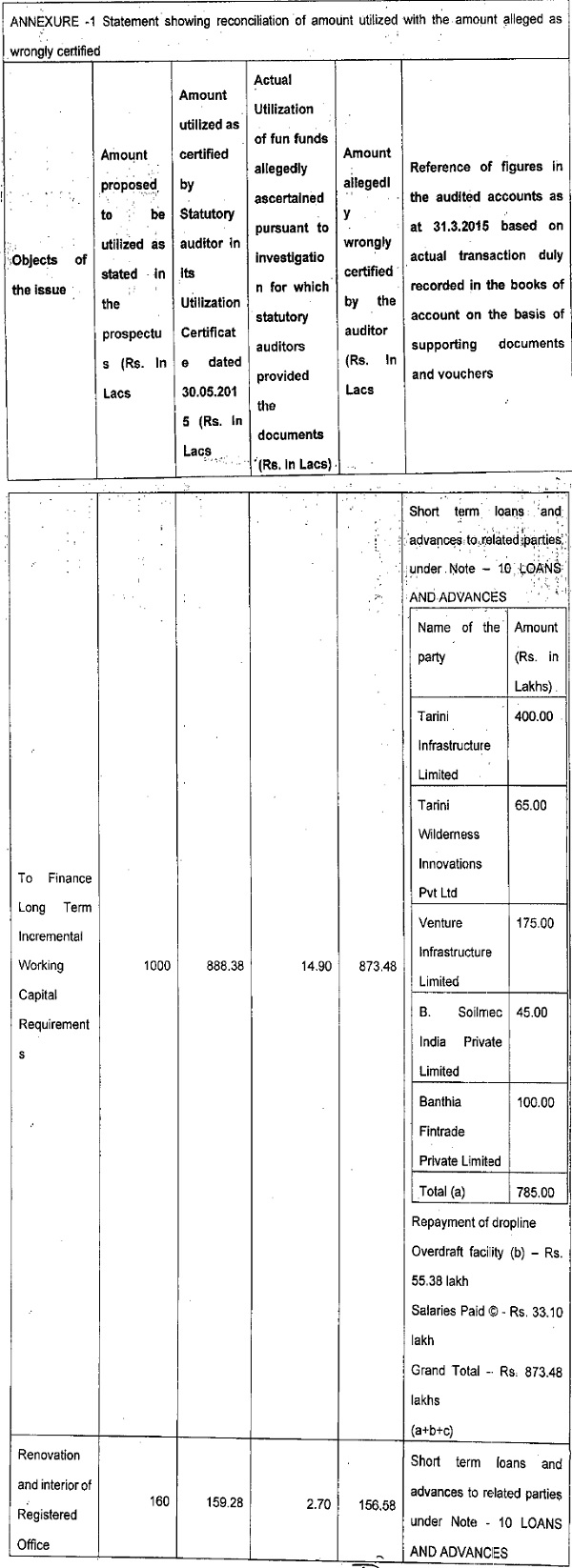

| S no | Particulars | Amount proposed to be utilized as per the prospectus .(Rs. in Lacs) | Actual utilization. of amount(Rs. in Lacs) |

| 1 |

To finance long term incremental working capital requirements |

1000.00 | 888.83 |

| 2. | Renovation and interior of registered office | 160.00 | 159.28 |

| 3. | Brand building | 150.00 | 72.95 |

| 4 | General Corporate purposes | 250.00 | 430.00 |

| 5 | Issue Expenses | 70.98 | 80.37 |

| Total | 1630.98 | 1630.98 |

8.8 In this context, the attention of the Committee was also drawn to the Director’s report dated 31.08.2015 addressed to the members of the subject Company wherein they had stated that the Company had utilized the amount of Rs. 1630.98 lakhs in terms of the prospectus. The Committee also took note of the Respondent’s submissions stating that he had carried out the verification while issuing the certificate and had also taken into consideration the various information contained in the Prospectus and explanations provided by the management of the Company and thus, the certificate had been issued stating the factual positions of ‘the transactions of the IPO proceeds and there was no false and misleading information in the certificate. The Committee noted that the audit report on the financial statements of the Company for Financial Year 2014-15 and the subject certificate, both had been issued and signed by the Respondent on 30th May 2015. In this specific context, the Committee observed that contradictory information had been given in the audit report read with financial statements of the Company audited by the Respondent for Financial Year 2014-15 and the subject certificate which had been issued on the same date. The Committee noted that the Respondent had qualified his opinion on the matter of utilization of IPO proceeds by the Company by reporting that there had been variation in the utilization of money, between the objects of public issue contained in the prospectus and actual utilization. The Committee noted that all the same point of time, the Respondent had issued certificate on the utilization of the proceeds of public issue wherein he certified that Rs. 1630.98 lakhs were actually utilized by the Company out of those proceeds of PO. Thus, the Committee observed that both documents, dated 30th May 2015, provided contradictory information regarding the utilization of IPO proceeds by the Company.

8.9 The Committee also took note of the Respondent’s submissions given in respect of producing evidence regarding actual utilization done by the Company to the tune of Rs. 151.60 Lakhs. The Respondent stated that there was a difference of opinion as to the definition of heads of objects of the issue, consideration of information and detail of projects disclosed in the prospectus under various objects. The Respondent asserted that the amount had been actually incurred and duly recorded in the books of account on the basis of supporting documents and vouchers, correctly classified, and presented in the financial statements as per the requirement of Schedule III of the Companies Act, 2013 and rules framed thereunder and in fact, the figures in the Certificate had been used and grouped from the said audited accounts as per the relevant definitions, for the purpose of classification as per the objects stated in the prospectus and therefore, there was no variance. The Committee observed that from the observations of the informant department contained in their investigation report based on the supporting documents produced by the Respondent before them, it was evident that the Company had incurred only ..Rs. 151.66 lakhs out of IPO proceeds for objects stated in prospectus as against Rs. 1630.98 lakhs as certified by. the Respondent. The Committee also observed that the subject certificate issued by the Respondent was clearly referring to the amount which was proposed to be utilized as per the prospectus. Against the same, the Respondent had reported the actual utilization of amount wherein the Respondent had certified that the Company had utilized the amount of Rs. 1630.98 lakhs as proposed to be utilized in the prospectus. Thus, the Committee observed that there was a significant variance of Rs. 1479.32 lakhs (i.e., 11,630.98 lakhs – X151.66 lakhs) in the utilization of proceeds of IPO, between the, objects of public issue contained in the prospectus and actual utilization as certified by the Respondent in the subject certificate.

8.11 The Committee also observed that the primary submission of the Respondent was that the utilization certificate should be read in conjunction with the audit report issued on the financial statements of the Company for the Financial Year 2014-15 which contained a qualification on the matter of variation in utilization of funds between the objects of public issue contained in the prospectus and actual utilization. The Committee observed that the subject certificate was only mentioning that the Respondent had examined the audited accounts of the Company for the relevant period for issuing the said certificate. In this certificate, the Respondent has certified the utilization of proceeds of the public issue brought by the Company. The Respondent in the certificate, has certified that the Company has actually utilized the amount of Rs. 1630.98 lakhs. The Committee observed that there was nowhere mentioned in the subject certificate that it had be read in conjunction with the audit report issued by him containing qualified opinion on the subject matter. Thus, the Committee observed that these assertions of the Respondent were also not tenable in this case.

8.12 Thus, on consideration of overall facts, submissions, and documentary evidence(s)/material on record and after thoroughly considering the charges against the Respondent, the Committee observed several discrepancies and contradictions in the actions of the Respondent. The Committee noted contradictory information between the audit report and the subject certificate issued by the Respondent on the same date i.e., 30th May 2015 regarding the utilization of IPO proceeds by the Company. The Committee also observed that there was a significant variance of Rs. 1479.32 lakhs between the amount proposed to be utilized as per the prospectus and the actual utilization certified by the Respondent in the subject certificate. The Committee also observed that the subject certificate does not mention anywhere that it should be read in conjunction with the audit report containing the qualified opinion.

8.13 In, light of these observations, the Committee concluded that the Respondent issued a certificate that provided wrong and misleading information utilization of IPO proceeds by the Company and failed to appropriately point out the discrepancies in the utilization of IPO proceeds by the Company. The Committee also noted that the actual utilization of IPO proceeds was significantly different from the certificate issued by the Respondent and that the utilization certificate issued by the Statutory Auditor was not true, and contained information in a distorted manner which might mislead the decision of the investors. Accordingly, the Committee held the Respondent GUILTY of Professional Misconduct falling within the meaning of Clauses (7) and (8) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

9.Conclusion:

In view of the findings stated in above paragraphs, vis-a-vis material on record, the Committee gives its charge wise findings as under:

| Charges (as per PFO) | Findings | Decision of the Committee |

| Para 2.1 as above | Para 8.1 to 8.12 as above | Guilty ~ Clause (7) and (8) of Part I of |

10. In view of the above observations, considering the oral and written submissions of the Respondent and material on record, the Committee held the Respondent GUILTY of Professional Misconduct falling within the meaning of Clause (7) and (8) of Part I of the Second Schedule to the Chartered Accountants Act, 1949.

Sd/-

(MS. DAKSHITA DAS, I.R.A.S. (RETD.})

GOVERNMENT NOMINEE