Disciplinary Committee (Bench-IV) of the Institute of Chartered Accountants of India (ICAI), in its order dated February 5, 2024, found CA Satish Kumar Jha guilty of professional and other misconduct. The case originated from a complaint filed by Anand Singh, Director of M/s Dot Truckers Ltd., alleging errors in the filing of GSTR-1 returns that led to the inclusion of unjustified GST invoices. These mistakes resulted in a tax liability of around ₹47 lakh for the company. Although the respondent argued that the issues could have stemmed from office mismanagement or unauthorized actions by others, and presented affidavits to demonstrate no undue benefit was taken, the Committee held that such defenses were extraneous to the primary concern—professional negligence. The Committee concluded that CA Jha failed to exercise due diligence expected of a chartered accountant while filing GST returns and his actions, including generation of false bills under valid GST numbers, were unacceptable under the professional standards. Consequently, he was found guilty under Clause (7) of Part I of the Second Schedule and Clause (2) of Part IV of the First Schedule to the Chartered Accountants Act, 1949. As a result, the Committee ordered that CA Satish Kumar Jha be reprimanded under Section 21B(3)(a) of the Act, considering it a fitting punishment for the misconduct established.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

[DISCIPLINARY COMMITTEE [BENCH-IV (2024-2025)]

[Constituted under Section 21B of the Chartered Accountants Act, 1949]

ORDER UNDER SECTION 2113(3) OF THE CHARTERED ACCOUNTANTS ACT, 1949 READ WITH. RULE. 19(1) OF THE CHARTERED ACCOUNTANTS (PROCEDURE OF INVESTIGATIONS OF PROFESSIONAL AND OTHER MISCONDUCT AND CONDUCT OF CASES) RULES, 2007.

[PRJ302/2018/DD/284/2018/DC/1563/2022]

In the matter of:.

Sh. Anand Singh, Director …Complainant

Versus

CA. Satish Kumar Jha …Respondent

MEMBERS PRESENT:

1. CA. Ranjeet Kumar Agarwal, Presiding Officer (In person)

2. Shri Jiwesh Nandan, I.A.S (Retd.), Government Nominee (In person)

3. Dakshita Das, I.R.A.S. (Retd.), Government Nominee (Through VC)

4. CA. Mangesh P Kinare, Member (Through VC)

5. CA. Abhay Chhajed, Member (In person)

DATE OF HEARING : 19th MARCH, 2024

DATE OF ORDER : 16th May, 2024

1. That vide Findings dated 05.02.2024 under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Disciplinary Committee was inter-alia of the opinion that CA. Satish Kumar Jha (hereinafter referred to as the Respondent”) is GUILTY of Professional and Other Misconduct falling within the meaning of Item (2) of Part-IV of First Schedule and Item (7) of Part-I of Second Schedule to the Chartered Accountants Act, 1949.

2. That pursuant to the said Findings, an action under Section 218(3) of the Chartered Accountants (Amendment) Act, 2006 was contemplated against the Respondent and a communication was addressed to him thereby granting an opportunity of being heard in person/ through video conferencing and to make representation before the Committee on 19th March 2024.

3. The Committee noted that on the date of hearing on 19th March 2024, the Respondent was present through video conferencing. During the hearing, the Respondent stated that he has already submitted his written representation vide letter dated 11th March 2024 on the Findings of the Disciplinary Committee. He further stated it was a procedural error and he had not done it intentionally, and he prayed to the Committee to take a lenient view. The Committee also noted that the Respondent had submitted written representation dated 11th March 2024 on the Findings of the Committee, which, inter-alia, are given as under:

(a) The Committee neither issued summons nor enforced attendance of the Complainant and thereby deprived the Respondent to examine the Complainant in exposing the falsehood in the allegations,

(b) The Respondent submitted affidavits of entities in whose name the alleged fraudulent GST invoices were created. He stated that there is no point of consideration of this vital evidence anywhere in the Findings of the Committee.

(c) The Committee took the admission of Respondent’s letter dated 11th September 2018 as evidence against him without analysing the contents in it, which clearly shows that it was a planned letter forced up on the Respondent by the Complainant.

(d) The Committee did not analyse the nature of the transactions that were alleged as fraud to figure out whether such acts would have yielded any benefit in the form of alleged input credits, whether a Chartered Accountant, who knows well that those entries could not have yielded any economic gain to others would have indulged in such stupid acts and whether there was any truth in the allegation of fraud and possible tax liability loss to the Complainant.

(e) The Committee failed to appreciate that the errors or omission in the GSTR 1, itself cannot cause a charge of professional misconduct, as this error could be the result of a mischief by someone in the office of the Respondent or by some others acted at the instigation of the GSM Complainant. Therefore, there was no case for invoking Clause (7) of Part 1 of Second Schedule as made out against the Respondent. An issue arising from poor office management of the Respondent in the form of errors / mischief in the filing of GSTR 1 would not amount to acts that lower the reputation of the profession. So, Invoking Clause (2) of Part IV of First Schedule also was unjustified.

(f) The Respondent prayed to the Hon’ble Committee to pardon him for the oversights.

4. The Committee considered the reasoning as contained in the Findings holding the Respondent ‘Guilty’ of Professional and Other Misconduct vis-a-vis written and verbal representation of the Respondent. The Committee noted that the issues/ submissions made by the Respondent as aforestated have been dealt with by it at the time of hearing under Rule 18.

5. Thus, keeping in view the facts and circumstances of the case, material on record including verbal and written representation of the Respondent on the Findings, the Committee noted that the conduct of the Respondent in producing affidavits from certain entities to show that unjustified GST input tax credits were not finally claimed by them, was extraneous to the main issue under consideration. The issue before the Committee was primarily related to examination of the professional conduct of the Respondent in filing the original Form GSTR-1; and on the facts, there is no dispute on the mistake committed on the part of the Respondent.

6. The Committee held that the Respondent has not exercised due diligence at the time of filing of original Form GSTR-1 wherein unjustified GST invoices. were included overlooking the impact of tax liability of Rs.47 lakhs approximately created–on the Company. The Committee was of the view that the generation of falsel, bill in the name of certain firms/companies along with their GST numbers in GST returns, as in the extants case, is not expected from a professional/ Chartered Accountant. Hence, the Professional and Other Misconduct on the part of the Respondent is clearly established as spelt out in the Committee’s Findings dated 05th February 2024, which is to be read in consonance with the instant Order being passed in the case.

7. Accordingly, the Committee was of the view that the ends of justice would be met if punishment is given to him in commensurate with his Professional and Other Misconduct.

8. Thus, the Committee ordered that the Respondent i.e., CA. Satish Kumar Jha, be REPRIMANDED, under Section 21B(3)(a) of the Chartered Accountants Act,1949.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(SHRI JIWESH NANDAN, I.A.S. {RETD.})

GOVERNMENT NOMINEE

Sd/-

(MS. DAKSHITA DAS, I.FLA.S.{RETD.})

GOVERNMENT NOMINEE

Sd/-

(CA. MANGESH P KINARE)

MEMBER

Sd/-

(CA. ABHAY CHHAJED)

MEMBER

CONFIDENTIAL

DISCIPLINARY COMMITTEE (BENCH — IV (2023-2024)1

‘Constituted under Section 218 of the Chartered Accountants Act, 19491

Findings under. Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules 2007.

File. No. : [PR/302/2018/DD/284/2018/DC/1563/20221 In the matter of:

Sh. Anand Singh, Director,

…Complainant

Versus

CA. Satish Kumar Jha

..Respondent

MEMBERS PRESENT:

CA. Ranjeet Kumar Agarwal, Presiding Officer (Through VC)

Shri Jiwesh Nandan, Government Nominee (In person).

Smt. Dakshita Das, Government Nominee (Through VC)

CA. Mangesh P Kinaren Member (Through VC)

CA. Gotha S Srinivas, Meniber (Through VC)

DATE OF FINAL HEARING : 28.11.2023

DATE OF DECISION TAKEN : 09.61.2024

PARTIES PRESENT:

Respondent: : CA. Satish Kumar Jha (Through VC)

Counsel for Respondent : CA. C.V. Sajan (Through VC) 92/

1. Background of the case:

The Complainant hired the services of the Respondent for filing of GST returns of his Company, M/s. DOT Truckers Limited (herein ‘after referred to as the “Complainant’ Company”). The Company in September, 2018 discovered that’ few service bills issued to certain parties were not related to their Company but: were included in their quarterly GST Returns in GSTR-1 for the quarters ended on December, 2017, March, 2017 and June, 2018 which resulted in creation of GST liability of Rs.47 lakhs on the Company.

2. Charges in Brief:

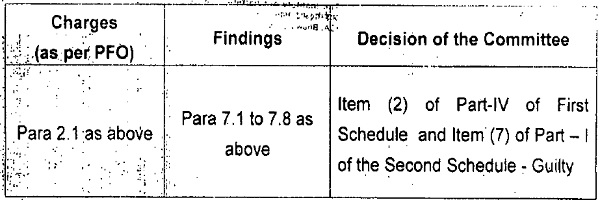

2.1 It was alleged that various false bills of services were entered fraudulently by the Respondent in quarterly GSTR-1 form of Complainant’s Company which created the GST liability of Rs. 47 Lakhs (approx.) on them. It was further stated that the said false bills were issued in the name of companies/firm with their GST numbers which were Respondent’s clients to whom he was allegedly trying to provide GST input tax credit and when the Complainant raised the issue, the Respondent admitted the fraud.

3. The relevant issues discussed in the Prima facie opinion dated 11th March 2022 formulated by the Director (Discipline) in the matter, in brief, is given below:

3.1 The main contention of the Complainant was that the Respondent had filed Form GSTR-1 on behalf of the Company wherein false details of parties were mentioned with respect to output supplies, thereby creating the GST liability of Rs. 47 Lakhs (approx.) on the Company. The Respondent raised the contention that the complaint had been settled up on his acceptance of professional responsibility and rectification of mistake, however, there was no such communication / withdrawal in the present matter from the end of Complainant.

3.2 The Respondent in his letter dated 11.09.2018 admitted that he had submitted fraudulent. GST bills to random companies in their name without the knowledge / consent of any of the directors and had thus thereby taken the responsibility for all liabilities in GST or any other department in all of his firms and its associates upto 31.12.2018. The Respondent further had firstly nowhere disputed the said letter in his Written Statement and secondly, he had adopted a contradictory stand by submitting that it was a mistake which had occurred due. to some technical error. It was thus viewed that the Respondent had adopted a contradictory stand on two different occasions for the subject matter of the Complaint .This raised doubt on the reliability and credibility of the submissions made by the Respondent in the extant matter. The plea of the Respondent for rectification of mistake does not absolve him of the liability of the Respondent with respect to filing of GST returns. The Respondent had deliberately participated in the fraudulent acts and transactions to manipulate the GST returns, thereby creating a false liability on the Company. Thus, the Respondent had been held liable for the allegations levelled by the Complainant in his complaint.

3.3 The Director (Discipline) in his Prima Facie Opinion dated 11th March 2022 has held that the Respondent was prima fade GUILTY of Professional and Other Misconduct falling within the meaning of Item (2) of Part IV of First Schedule and Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949. The said Items to the Schedule to the Act, state as under:

Item (2) of Part IV of First Schedule:

A member of the Institute, whether in practice or not, shall be deemed to be guilty of other misconduct, if he:

(2) in the opinion of the Council, brings disrepute to the profession or the Institute as a result of his action whether or not related to his professional work”

Item– (7) of Part I of Second Schedule:

“A chartered accountant in practice shall be deemed to be guilty of professional misconduct if he:

(7) does not exercise due diligence or is grossly negligent in the conduct of his professional duties.”

3.4 The Prima Facie Opinion formed by Director (Discipline) was considered by the Disciplinary Committee at its meeting held on 8th April 2022. The Committee on j5,consideration of the same, concurred with the reasons given against the charges and thus, agreed with the prima fade opinion of the Director’ (Discipline) that the Respondent is prima facie GUILTY. of Professional and Other Misconduct falling within the meaning of itent (2) of Part IV of First Schedule and Item (7) of Part I of the Second, Schedule to •the Chartered Accountants Act, 1949 and accordingly, decided td, proceed further under Chapter V of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007. The Committee also directed the Directorate that in terms of the provisions of sub-rule (2) of Rule 18, the prima facie opinion formed by the Director (Discipline) be sent to the Complainant and the Respondent including particulars or documents relied upon by the Director (Discipline), if, any, during the course of formation of prima facie opinion and the Respondent be asked to submit his Written Statement in terms of the provisions of the aforesaid Rules, 2007.

4. Date(s) of Written submissions/pleadings:

4.1 The relevant details of filing of documents in the instant case by the parties are given below:

| S. No. | Particulars | Dated |

| 1. | Complaint in Form ‘I’ filed by the Complainant | 15th September 2018 |

| 2. | Written Statement filed by the Respondent | Dated Nil (Received on 23rd October 2018) |

| 3. | Rejoinder filed by the Complainant | 17th November 2018 |

| 4. | Prima facie Opinion by Director (Discipline) | 11th March 2022 |

| 5. | Written Statement filed by the Respondent after PFO | 3rd August 2023 18th August 2023 |

5. Written Statement filed by the Respondent after PFO:

5.1 The Respondent vide his Written Statement dated 03rd August 2023 submitted the following:

(i) That GST Tax liability on a registered person was determined on the basis of GSTR 3B, to be filed every month. In the case of the subject Company i.e., M/s DOT Truckers Ltd, GSTR 3B for all months for Financial Year 201718, and for the first quarter of Financial Year 2018- 19 were filed in time with accurate data and there was no room for the Complainant to be aggrieved on the grounds that he was subjected to any loss on account of GST liability.

(ii) That according to the rules in force it was not possible to avail any GST Input tax credit, solely based on the above wrongful filling of the details of invoices and GSTIN of B2B customers in GSTR 1 of the Complainant. According to rules, movement of goods from seller to buyer and payment of sales consideration were essential for claiming GST inputs. Those mischievous, unrelated, unsubstantiated and meaningless entries recorded in the contentious GSTR 1, were not going to yield any benefit of GST Input to anyone, as these alleged entries were not backed by any documentation by suppliers for invoicing or delivery of goods / services. Moreover, no cash flow was involved in those transactions, no purchases had been accounted for by the corresponding parties, and no delivery of goods or services had taken place.

(iii)That he found the errors while examining the GST Returns for the purpose of Annual Audit of Complainant’s Company for FY 2017-18, on 10th September 2018. GSTR 1 Returns of the Company reported for the quarters of October — December 2017 and January — March 2018 had carried B2B sales amounted to Rs. 1,04,74,719 and Rs. 1,12,71,922 respectively, because of this wrongful filling of data. Later, similar error was found in the GSTR 1 first Quarter of FY 2018-19 also. All these returns had been filed together in July 2018. The Respondent was not able to figure out whether the errors had happened within the office by own staff or not.

(iv)That it was an admission of the Respondent under duress from the Complainant that had been used as evidence in the instant case, which had no evidentiary vaIue. Further, there was no truth in the allegation that an additional tax liability: of Rs 47 lakhs were created on the Complainant. The errors in the instant case did not prove any intention to evade tax, because no Input tax credit of GST was claimed by any of the parties (whose GSTIN were mentioned in the wrongly filled GSTR 1 of the Complainant Company), even though GST Returns for all those corresponding parties were also filed from the office of the Respondent. If the intention behind wrong filing of GSTR 1 of the Complainant Company was to evade any, tax payment, then there had to be corresponding claims of GST Input tax credit in the GST Returns of the counter.parties, which was not existent here.

5.2 The Respondent, in order to substantiate his claim mentioned that the entities mentioned in GSTR-1 of the Complainant’s Company along with their GSTIN never claimed any GST Input tax credit against any such recorded transactions, has vide his letter dated 18th August, 2023 brought on record 14 affidavits on behalf of such entities.

6. Brief facts of the Proceedings:

6.1 The details of the hearing(s) fixed and held/adjourned in said matter are given as under:

| Particulars | Date of Meeting(s) | Status |

| 1St time | 22nd May 2023 | Adjourned at the request of the Respondent and in the absence of Complainant |

| 2nd time | 25th July 2023 | Part heard and Adjourned |

| 3rd time | 10thAugust 2023 | Part heard and Adjourned |

| 4th time | 5th September 2023 | Part heard and adjourned in the absence of Complainant |

| 5th time | 28th November 2023 | Hearing Concluded and Judgement Reserved |

| 6th time | 9th January 2024 | Decision taken |

6.2 On the day of first hearing on 22nd May 2023, the Committee noted that the Respondent was not present and had sought adjournment vide his email dated 13th May 2023 for attending his family function. The Committee also noted that the Complainant was also not present and the notice of listing of the case had been served upon him. Thus, the Committee acceded to the request of the Respondent and adjourned the case to a later date.

6.3 Thereafter, on the day of hearing on 25th July 2023, the Committee noted that the Respondent along with Counsel were present through Video conferencing mode. The Committee noted that the Complainant was not present and notice of meeting had been served upon him. Thereafter, the Respondent was put on oath. The Committee enquired from the Respondent as to whether he was aware of the charges and the same were also read out before. him. On the same the Respondent replied that he is aware about the charges but pleaded ‘Not Guilty’ on the charges levelled against him. Thereafter, in view of Rule 18(9) of the Chartered Accountants (Procedure of Investigation of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Committee adjourned the case to later date.

6.4 On the day of hearing on 10th August 2023, the Committee noted that the Respondent along with Counsel were present through Video conferencing mode. The Committee also noted that the Complainant was not present and notice of listing of the case had been served upon him. The Committee asked the Counsel for the Respondent to make his submissions. The Counsel for the Respondent submitted the background and facts of the case. The Committee noted that the Respondent vide submissions dated 03.08.2023 had stated that the instant matter had been resolved with the Complainant. The Counsel for the Respondent made a plea before the Committee that he wished to examine the staff member of the Company as witness(es). After recording the submissions of the Counsel for the Respondent, the Committee directed the Respondent to file the following documents/information within next 10 days:

a. Contad Number/email id of the Complainant.

b. To provide the details of the witnesses along with their latest contact number.

Thereafter, the Committee adjourned the case to a later date. Thus, the matter was part-heard and adjourned.

6.5 On the day of hearing on 5th September 2023, the Committee noted that the Respondent along with Counsel were present through Video conferencing mode. The Committee noted that the Complainant was not present and notice of listing of the case had been served upon him. The. Cornmittee noted that the Complainant neither answered the telephone calls of the;, office, nor: gave any , intimation regarding his participation in the proceedings.. The Committee, asked, the Respondent to make submissions in the matter. The Counsel for;

submitted that he wished to examine Mr:. Roshan- Thakur .as witness in this case. The Committee categorically asked the role and relevance of the witness as regard to this case. The Counsel for the Respondent submitted that the witness was an employee of the Respondent and was part of this alleged case. The Committee was of the view that the statement of Mr. Roshan Thakur would not be relevant in the case, as he may not provide any new evidence or give an independent view in the matter being an employee of the Respondent. Thus, calling for examination of witness was not warranted as the documents/evidences placed on record are sufficient for the purpose of consideration of the matter. The Committee, on consideration, was of the view that the said request was made clearly for the purpose of vexation and delay therefore, be refused in view of the provisions of Rule 18(14) of the Chartered Accountants (Procedure of Investigation of Professional and Other Misconduct and Conduct of Cases) Rules, 2007. The Committee extended one final opportunity to the Complainant to substantiate the charges and adjourned the hearing in the said matter. The Committee decided that in case of failure of Complainant to participate in the next hearing, the matter be proceeded ex-parte, the Complainant.

6.6 On the day of final hearing on 28th November 2023, the Committee noted that the Respondent along with Counsel were present through Video conferencing mode. The Committee noted that the Complainant was not present and notice of listing of this case was duly served upon him and he was specifically informed that in case of his non-appearance, the matter would be decided ex-parte. The Committee was of the view that ample opportunities were granted to the Complainant to substantiate the charges, but he failed to appear before it and in the absence of the Complainant, the Committee decided to proceed ex-parte. The Committee asked the Counsel for the Respondent to make his final Submissions. The Respondent’s Counsel submitted that he had already made detailed submissions during the last hearing and had demonstrated with supporting evidences that this was a frivolous case. Based on the documents and information, available on record and after considering the submissions made by the Respondent’s Counsel, the Committee concluded the hearing in the matter and judgement was reserved.

6.7 Thereafter, in the meeting held on 09th January 2024, the Committee noted that the matter was concluded on 28th November 2023 and the judgement was reserved. After considering the documents and information available on record and considering the oral and written submissions made by the Respondent at the time of hearing(s), the Committee passed its judgement.

7. Findings of the Committee

7.1 The Committee noted that the Complainant has never attended any hearing in spite of being given advance notices duly sent. The Committee took all the efforts to reach the complainant on the basis of details available about him. Further, the Complainant has also not made any further submissions (in lieu of his presence) to substantiate his charges. Therefore, the Committee had no option but to consider the written and oral submissions of the Respondent vis-a-vis the charges mentioned in the original Complaint filed by the Complainant.

7.2 The Committee noted the charge against the Respondent that in order to provide GST input tax credit to his clients, the Respondent fraudulently entered false bills of services in GST Return of Complainant’s Company in Form GSTR-1 and thereby created GST liability of Rs. 47 lakhs approx. on the Company.

7.3 The Committee examined the contents of Respondent’s letter dated 11.9.2018 wherein he had admitted that he committed the fraud on the Complainant by issuing fraudulent bills in the name of Complainant’s company without the consent of any of its Directors to certain companies/firms. The relevant para of the said letter is given below:

“I Satish. Kumar Jha, hereby accept that I have committed a flay .with one of my clients Mr. Anand Singh as it was found that I issued Fraud GST bills to Tandom companies in the name of DOT Truckers Ltd without any of the Directors consent.” I take responsibilities for all of the liabilities in, GST or any other Departments in all of his firms or’7,’ its associates upto 31st December 2018. I have given original papers of both of my shops (eldeco station mall sec-12, Faridabad) to repay my debts towards, him.”

7.4 The Committee in this regard considered the plea of the Respondent that the above stated admission was taken from him under coercion and also that the inclusion of false bills in GSTR-1 was a mistake about which he was not aware. Further, the Committee also considered the fact that the alleged mistakes in Form GSTR-1 of Complainant’s Company were rectified by the Respondent by filing rectified GSTR-1 on 14.09.2018 whereby the tax liability of Rs.47 lakhs created on Complainant’s Company was reversed.

7.5 The Committee was of the view that the responsibility of filing the GST Returns of the Complainant’s Company, in a diligent manner, vested with the Respondent only and hence, the plea of the Respondent that he was not aware about the mistake in such returns, was not tenable.

7.6 On overall consideration of the matter, the Committee observed that it was an admitted fact that the mistake had occurred in Form GSTR-1 of the Complainant’s Company for three quarters ending December, 2017, March, 2018 and June, 2018 filed by the Respondent which contained false details of parties with respect to output supplies. The Committee also observed that the mistake was committed in GSTR -1 for consecutive three quarters ending December, 2017, March, 2018 and June, 2018 respectively.

7.7 In view of above , the Committee opined that the Respondent did not apply due diligence while filing GSTR-1 of Complainant’s Company and thus, repeatedly included false invoices aggregating to Rs.2.47 Crores issued to certain firms/companies not related to Complainant’s company involving GST tax liability of Rs.47 lakh approx. The Committee further opined that though the rectification of GST return was a valid course of action but it does not absolve the Respondent from his professional responsibility of filing of GST return diligently.

7.8 The Committee was of the view that the conduct of the Respondent in producing affidavits from certain entities to show that unjustified GST input tax credits were not finally claimed by them was extraneous to the main issue under consideration. The issue before the Committee was primarily related to examination of the professional conduct of the Respondent in filing the original Form GSTR-1; and on the facts, there is no dispute on the mistake committed on the part of the Respondent. From the foregoing discussions, the inevitable conclusion that reaches is that the Respondent has not exercised due diligence at the time of filing of original Form GSTR-1 wherein unjustified GST invoices were included overlooking the impact of tax liability of Rs.47 lakh approximately created on the company. The Committee also opined that the generation of false bills in the name of certain firms/companies along with their GST numbers in GST returns, as in the extant case, is not expected of a professional.

7.9 Therefore, the Committee held the Respondent GUILTY of Professional and Other Misconduct failing within the meaning of Item (7) of Part – I of Second Schedule and Item (2) of Part-IV of First Schedule to the . Chartered Accountants Act, 1949.

8. Conclusion

In the view of the findings States’ in the-above paras, vis-a vis material on record, the Committee gives its finding as under:

9. In view of the above observations, considering the ‘submissions of the’ Respondent and Complainant, and documents on record, the Committee field the Respondent GUILTY of Professional and Other Misconduct falling Within the meaning of Item (2) of Part-IV of First Schedule and Item (7)! of Pail I Second Schedule to the Chartered Accountants Act, 1949.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(SHRI JIWESH NANDAN, I.A.S. (RETD.)

GOVERNMENT NOMINEE

Sd/-

(MS. DAKSHITA DAS, IRAS,RETD.)

GOVERNMENT NOMINEE

Sd/-

MANGESH P KINARE)

MEMBER

Sd/-

(CA. COTHA S SRINIVAS)

MEMBER

DATE : 05.02.2024

PLACE:NEW DELHI