Death of Seamless Flow of Input Tax Credit in 2022 – Major Changes under GST

Finance Minister Hon’ble Nirmala Sitharaman in her budget speech, addressed as “Hon’ble Speaker, we are marking Azadi ka Amrit Mahotsav, and have entered into Amrit Kaal, the 25-year-long leadup to India@100”.

The wonder baby seamless flow of ITC which raised so many hopes and reduced the burdens, had been slowly placed into precarious health condition of late. On the Budget 2022 day it has been put on ventilator with no hope of recovery. The day when changes of Finance Act, 2022 are put into effect would be the date of death of seamless flow of ITC.

A new clause (ba) to sub-section (2) of section 16 of the CGST Act thru Clause 99 of the Finance Bill, 2022 is being inserted to provide that input tax credit with respect to a supply can be availed only if such credit has not been restricted in the details communicated to the taxpayer under section 38.

Clause 103 of the Finance Bill, 2022 seeks to substitute a new section for section 38 of the CGST Act. Sub-section (1) seeks to empower the Central Government to make rules to specify other supplies as well as the manner, time, conditions and restrictions for communication of details of inward supplies and input tax credit to the recipient by means of an auto-generated statement and to do away with two-way communications process in return filing.

What is auto generated statement?

GSTR-2A is auto generated tax credit statement generated by the portal. The statement filed in GSTR-1 by the supplier is auto generated and drafted to the GSTR-2A of the recipient.

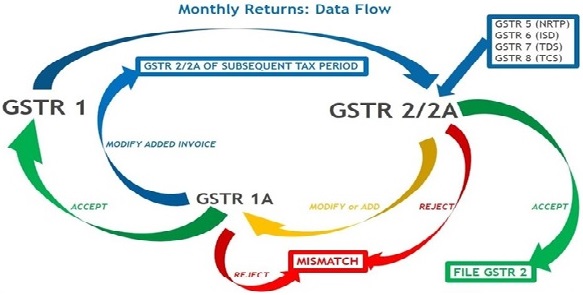

Now let us understood what is two-way communications?

Two-way communications in common parlance: Below small chart depicts the process in day to day routine.

Two-way communications in GST:

The above chart clearly shows about the two-way communications since the inception of GST. Due to system functionalities not in place, this two-way communications system is not yet implemented on the common portal although provision was there in the act. By insertion of new section 38, this communication has no relevance with special focus on auto-generated statement and to give the claim of credit with certain conditions and restrictions. This itself clarifies that now the government has done away with the requirement of filling of statement of inward supplies.

Here is the new Section 38 of the CGST Act:

Communication of details of inward supplies and input tax credit.

(1) The details of outward supplies furnished by the registered persons under sub-section (1) of section 37 and of such other supplies as may be prescribed, and an auto-generated statement containing the details of input tax credit shall be made available electronically to the recipients of such supplies in such form and manner, within such time, and subject to such conditions and restrictions as may be prescribed.

(2) The auto-generated statement under sub-section (1) shall consist of––

(a) details of inward supplies in respect of which credit of input tax may be available to the recipient; and

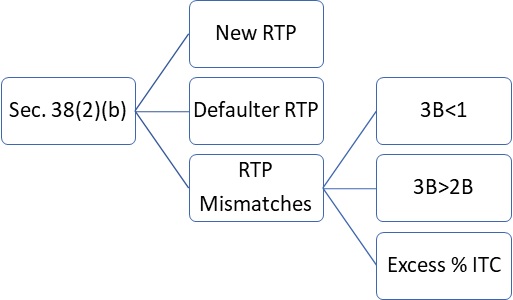

(b) details of supplies in respect of which such credit cannot be availed, whether wholly or partly, by the recipient, on account of the details of the said supplies being furnished under sub-section (1) of section 37,––

(i) by any registered person within such period of taking registration as may be prescribed; or

(ii) by any registered person, who has defaulted in payment of tax and where such default has continued for such period as may be prescribed; or

(iii) by any registered person, the output tax payable by whom in accordance with the statement of outward supplies furnished by him under the said sub-section during such period, as may be prescribed, exceeds the output tax paid by him during the said period by such limit as may be prescribed; or

(iv) by any registered person who, during such period as may be prescribed, has availed credit of input tax of an amount that exceeds the credit that can be availed by him in accordance with clause (a), by such limit as may be prescribed; or

(v) by any registered person, who has defaulted in discharging his tax liability in accordance with the provisions of sub-section (12) of section 49 subject to such conditions and restrictions as may be prescribed; or

(vi) by such other class of persons as may be prescribed.

The implementation of GST got punctures by virtue of this section. The revenue is indirectly shifting their burden on the tax payers as most of the tax payers are genuine and fall into the category of MSME. There can have large impact and affecting the working capital of the enterprise. Regular follow-ups with the supplier will be cumbersome task to be done in regular basis by the MSME recipient.

The Input Tax Credit availment is based on the conditions of Sec 16 subject to blocked credits and reversals. Timely compliance by the Supplier and payment of tax by the vendor is the major consideration now-a-days. The input tax credit is available only if the invoices are appearing in Form GSTR-2A/2B which is inserted thru clause (aa) in Sec 16.

Now the supplier is SUPREME. Timely reporting by the supplier in their GSTR-1 is the key to availment of credit by the recipient. Now the time has come to mandate e-invoice to the supplier on all B2B invoice so that timely and correct credit available to the recipient. Further, Now the time has come to effective Section 149 of the CGST Act, the GST compliance rating to check by the recipient while dealing with the supplier. Here the provisions-

Sec 149 – (1) Every registered person may be assigned a goods and services tax compliance rating score by the Government based on his record of compliance with the provisions of this Act.

(2) The goods and services tax compliance rating score may be determined on the basis of such parameters as may be prescribed.

(3) The goods and services tax compliance rating score may be updated at periodic intervals and intimated to the registered person and also placed in the public domain in such manner as may be prescribed.

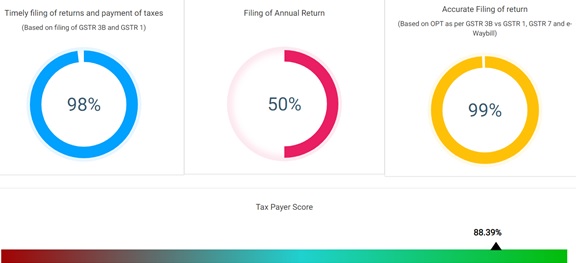

Kerala Government already starts to Create a Rating System for Tax Paying Traders. Kerala’s government is preparing to adopt a special ‘rating score’ for state traders who file accurate annual returns on time and pay their taxes on time.

The Kerala Goods and Services Tax administration is implemented the project, dubbed “Tax Payer Card,” for those traders who are registered under the GST Act. This program is now online on 3rd February, 2022. For e.g. timely filing of GSTR-3B and GSTR-1 before due date will get 100 out of 100 points. Similarly filing between 10 days to 1 month will get 50 out of 100 points and others criteria for GSTR-9, accurate filing of return and finally a tax payer score. Here is the diagram below:

******

Disclaimer: The contents of this article are for information and strictly for educative purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy &reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio

” ‘Death of Seamless Flow’ of Input Tax Credit in 2022″-

‘Death’ (or expiry) , one would have thought, can happen only to some-one (-thing) that is born live and been ever alive at least for a while !?

It has become a fashion for the practicing CAs to criticize every move by the govt to catch the tax evaders who were so far propped up by the so called professionals. i welcome this step by the govt as an assessee as long as we get the complete details of the automated 2B and 3B and option is given to assessess where they take the credit after a lag due to accounting issues. My suggestion to all the professionals is that welcome any move by the govt which is brought in to catch the white collared thieves and give u r feed back on how it can improvised further. DONT BE A NEGATIVE CHARACTER . Govt is collecting the money and putting in the right pockets where its required . we have a honest govt in place which every citizen has to support irrespective of their affiliation.