The Finance Act, 2019 introduced a new section, Section 194N which brings the concept of TDS on cash withdrawal. In order to strengthen the Digital Economy and to curb on physical cash movement, the Government of India took the initiative to tax the person(s) who withdraw heavy cash from the bank account and below is the brief about deduction of TDS on cash withdrawal.

Who is liable to deduct TDS

- Banks and banking institution

- Co-operative societies engaged in the business of banking

- A post office

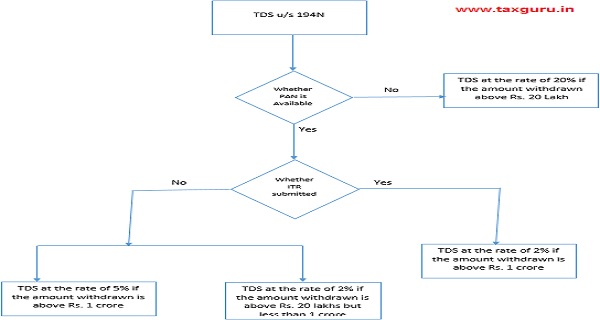

Amount limitation

- The limitation amount is Rs. 1 crore for all the accounts maintained by the assessee taken together subject to the condition that assessee has filed return for last three years. For example, if the assesse has filed ITR for FY 2019-20, FY 2018-19 and FY 2017-18, then the limitation amount will be upto Rs. 1 crore that can be withdrawn by the assessee in FY 2021-22.

- If the assessee has not filed return for last three years then the limitation amount will be Rs. 20 lakh

Rate of TDS

- TDS shall be deducted at the rate of 2% of the amount withdrawn. This is in case where assessee has filed return for last three years as mentioned above. TDS shall be deducted on whole amount and not on over and above Rs. 1 crore.

- In case, assessee has not filed ITR for last three years, then TDS rate shall be as follows,

-

- Up to Rs.20 Lakh – Nil

- 20 Lakh to Rs.1 Crore – 2%

- In excess of Rs.1 Crore – 5%

-

- In case, PAN is not provided by the assessee, 20% TDS shall be deducted on both the cases mentioned above.

- For foreign companies, foreign partnership firms, Non-residents additional surcharge and health & education cess will be applicable as per Income Tax law

- Assessee has to submit copy of ITR of last three years with bank. Banks will consider all cash withdrawals at the Primary CRN (Customer Relationship Number) level.

- It will be applicable for all accounts maintained under a PAN starting from 01.04.2021

This section will not be applicable on below mentioned person(s),

- Central or State Government of Government bodies

- Banks and co-operative societies engaged in the business of banking

- Any business correspondent of a bank or co-operative societies in accordance with the guidelines issued by RBI

- Any white label ATM operator of a bank or co-operative societies as authorized by RBI

- Commission agent or trader registered in Agriculture Produce Market Committee who has intimated to the bank or co-operative society their account number along with PAN.

About the Author

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.

Author is Amit Jindal, ACA working as Manager Taxation in Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.