GST RCM on Renting of Vehicle

Notification No. 21/2019 dated 30/09/2019 under IGST Act, 2019 applicable from 01/10/2019

Notification No. 22/2019 dated 30/09/2019 under CGST Act, 2019 applicable from 01/10/2019

Notification…….

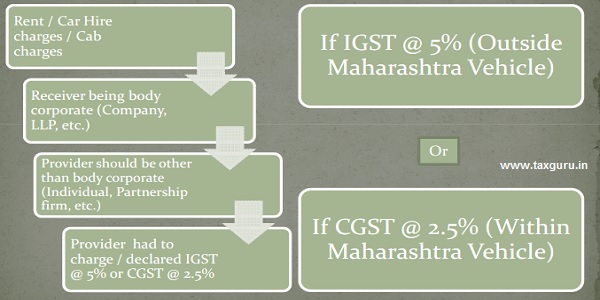

| Services provided by way of renting of a motor vehicle provided to a body corporate | Any person other than a body corporate, paying integrated tax at the rate of 5% on renting of motor vehicles with input tax credit only of input service in the same line of business |

Any body corporate located in the taxable territory. |

| Services provided by way of renting of a motor vehicle provided to a body corporate | Any person other than body corporate, paying central tax at the rate or 2.5% on renting of motor vehicles with input tax credit only of input service in the same line of business |

Any body corporate located in the taxable territory. |

Renting of Vehicle Means

Difference between Renting of vehicle/Transport of Passenger

| Key attribute | Renting of a Motor Vehicle | Contract for Transport of employees or Passenger |

| Intent | Hire of a motor vehicle with or without a Driver | To pick & drop the desired list of employees or passengers at the instruction of the employer |

| Periodicity | On need basis | On a continuity basis |

| Pricing | Basic fare + variable component on use basis | Fixed fare + variable component for kms or extra hours |

| Knowledge on place of use | Usually not a pre-condition to specify the location/ destination for such renting of a motor vehicle | Pre-defined specific route shall be confirmed. On need basis within a territorial jurisdiction the motor vehicle shall ply as per the contract |

| Risk & responsibility | Owner oT the vehicle casts responsibility on the buyer tor proper maintenance of such motor vehicle in the course of contract period to use such vehicle | Owner of the vehicle takes ultimate responsibility to upkeep and maintain the vehicle in proper working condition and little responsibility tasted on the recipient for its usage |

Renting of vehicle within Maharashtra

Renting of vehicle outside Maharashtra

GST Implication

- RCM is applicable on even on employees reimbursement.

- RCM is not applicable on OLA / Uber / Meeru, etc. being body corporate.

- Input tax credit of payment made under RCM is not available. i.e. it is cost

- to the company.

- If vendor is charges GST more than 5% then GST RCM is not applicable.

- Solution is to avail services from corporate vendors.

- Another solution is to change employee traveling policy.

Conclusion

- GST RCM is applicable on Renting of vehicle taken from non body corporate service provider charging / indicating IGST @ 5% or CGST @ 2.5%.

- RCM has to be paid in cash.

- No GST credit is available on the same.

Access Denied! Only Regstered Users Can Download The File "GST RCM on Renting of Vehicle". Register Here or Login

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.

one of my client has rented bolero car, on fixed rent, to airport authority of India, how the invoice should be raised ?? with gst ? or rcm ? who will pay rcm ??