Introduction:-

Deemed exports, as the name specifies, are those transactions which are considered as exports but not actually exports. This explanation might have confused you. So, let me put it in this way. First of all, we’ll understand what are exports? Supply of goods to a place outside India and repatriating that proceeds in foreign exchange to India, is called as export of goods. Deemed export is completely opposite to this. Here, the supply of goods will be in India and proceeds will be received in rupees itself, but the transaction is deemed to be an export i.e., Deemed Export. So, why such concept? How to claim benefits of Deemed Exports? Already exports are dumped up with huge benefits, are all these benefits applicable to this deemed exports? We’ll see the answers to all these questions in this article.

As per section 147 of Central Goods and Service Tax Act, 2017 “The Government may, on the recommendations of the Council, notify certain supplies of goods as deemed exports, where goods supplied do not leave India, and payment for such supplies is received either in Indian rupees or in convertible foreign exchange, if such goods are manufactured in India”

Meaning of Deemed Exports

- Such goods are manufactured in India.

- Goods (not services) supplied does not leave India, and

- Payment for such supplies received either in Indian Rupees or Convertible Foreign Exchange.

Categories of supply of goods notified as Deemed Exports under GST

In exercise of powers conferred under section 147 of CGST Act, the Central Government has issued Notification no. 47/2017-Central Tax dated 18.10.2017 wherein the following categories of the supply of goods has been declared as Deemed Exports.

1. Supply of goods by a registered person against advance Authorisation.

2. Supply of capital goods by a registered person against Export Promotion Capital Goods Authorisation.

3. Supply of goods by a registered person to Export Oriented Unit.

4. Supply of gold by a bank or Public Sector Undertaking specified in the notification no. 50/2017-Customs, dated the 30th June, 2017(as amended) against Advance Authorisation.

Conditions to qualify as Deemed Exports

- Applicable only for the supply of goods (not applicable to services)

- Goods are not required to be taken outside India.

- Such supply of goods must be notified by the Central Government as Deemed Exports under Section 147 of the CGST Act 2017.

- Goods must be manufactured or produced in India.

- Payment can be received in Indian Rupees or in convertible foreign exchange.

- The tax must be paid at the time of supply. Refund of tax paid on such supplies can be claimed.

Additional conditions for deemed exports to EOU/STP/HTP

1. The EOU/EHTP/STP/BTP unit must give prior intimation by filing Form A to the supplier and the Jurisdictional GST officer of supplier and recipient.

2. Form A must bear a running serial number and contain details of goods to be procured, which is pre-approved by the Development Commissioner.

3. The supplier must the supply goods under the cover of a tax invoice.

4. The tax invoice must be endorsed by the recipient. Endorsed copy of the same must be sent to the supplier and jurisdictional GST officer of the supplier and recipient.

5. Record of such goods received by EOU/EHTP/STP/BTP unit must be maintained in Form B.

Time limit for filing refund claim

To apply for refund the recipient or supplier of deemed export supplies has to file an application in FORM GST RFD-01A through common portal before expiry of 2 from the relevant date in such form and manner as may be prescribed- (rule 54(1) of CGST act 2017). Relevant date for is date when the return is furnished containing deemed export details. However, the tax payer will still have the option to physically submit the refund application to the jurisdictional proper officer in FORM GST RFD-01A, along with supporting documents, if he chooses so. It may be noted that the documents/undertaking/invoices to be submitted along with the refund application in FORM GST RFD-01A are the same as have been prescribed under the CGST rules and various circulars issued on the subject from time to time.

Documents required to claim refund: –

In case the supplier is claiming a refund of tax paid on deemed exports, the following details/documents must be produced:

1. A statement containing invoice wise details of deemed export supplies made by the supplier.

2. Acknowledgement by jurisdiction tax officer of AA and EPCG holder that the said deemed export supplies have been received OR in case of EOU/EHTP/STP/BTP/ Copy of tax invoice signed by the recipient that said deemed export supplies have been received.

3. Undertaking by the recipient that no ITC has been claimed.

4. Undertaking by the recipient that it shall not claim a refund in respect of such supplies.

5. Self-Declaration from Supplier

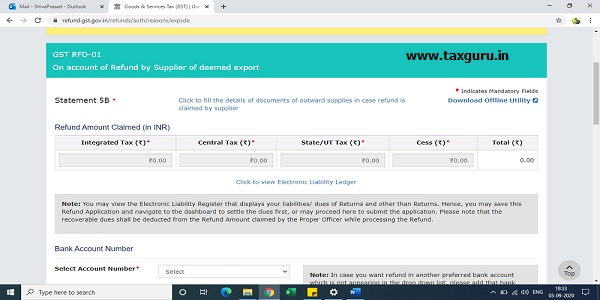

6. Statement-5B

7. CA Certificate

8. Documents required under Notification No. 49/2017-CT dated 18.10.2017 and Circular No. 14/14/2017-GST dated 06.11.2017.

Who can claim refund:-

In respect of supplies regarded as deemed exports, the application may be filed by, –

(a) the recipient of deemed export supplies; or

(b) the supplier of deemed export supplies in cases where the recipient does not avail of input tax credit on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund

Procedure to claim refund – Supplier of Deemed Exports

To claim for a refund on account of the supplier of deemed exports, follows the steps mentioned below:

Step 1: Kindly visit the official portal of department and Provide login details.

Step 2: Login to the GST portal with accurate details like user id and password and click on “login” button.

Step 3: Click services and select “Application for Refund” option from Refund menu.

Choose Refund Type

Step 4: Select the “On account of Refund by Supplier of Deemed Export”

Step 5: Choose the Financial Year and Tax Period for which application has to be filed from the drop-down list and click the create button.

Step 6: Click Yes

Step 7: Click the “Download offline Utility” link and press the “proceed” button to continue.

Step 8: Enter the details of Serial Number, Invoices of tax paid and click the “Validate & Calculate” button.

Step 9: the total number of records in the sheet is displayed. Click the “Create File to Upload” button and save your file.

Step 10: Now press the “Click to fill the details of invoices of outward supplies in case refund is claimed by supplier” after amount will be displayed.

Step 11: Now press the “Click to fill the details of documents of inward supplies in case refund is claimed by Recipient” after amount will be displayed.

Advantages and disadvantages, differences in refund claim as recipient and supplier:-

Conclusion:

The concept of deemed exports is exhaustive. Thus, an attempt has been made in this article to show the practical aspects which we have to face while filing a refund application on account of deemed exports. Claiming the refund either by the supplier or the recipient will be based upon the mutual agreement. As an industry practice filing the refund application by the supplier could make him compete in the market.

Author Bio

Good article Shivu Prasad, the article was helpful

I formative article

Nice article, with reference to the actual portal for easy understanding