About the Section 194N

This section is inserted in the Union Budget 2019 proposed on 5th July, 2019. However, in this section certain amendment is incorporated by Union Budget 2020 proposed on 27th March, 2020.

Hence let’s understand about this section including with amendment.

According to this section, Every Person (Payer) being

i. A banking Co.

ii. Co-operative society (engaged in banking business)

iii. A post office

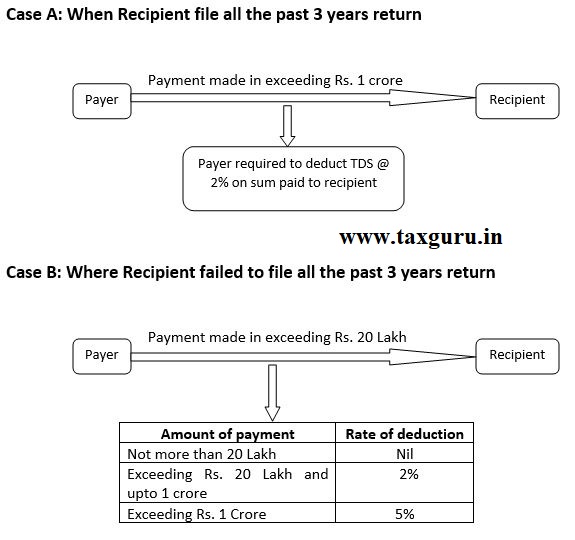

Who is responsible to paying cash, whether amount or aggregate of amounts, in exceeding rupees 1 Crore during the previous year to any person (i.e. recipient) from single account or multiple accounts?

Rate of Deduction of Tax

Then the above-mentioned person (payer) required to deduct tax @ 2% of such sum.

Exception to this section

Provided that if any person being recipient who have not filed income tax return for all of the 3 Assessment year, immediately preceding to previous year in which payment made to him, then this section is applicable with the following modification:

| Amount of payment | Rate of deduction |

| Not more than 20 Lakh (≤20 Lakh) | Nil |

| Exceeding Rs. 20 Lakh upto 1 crore (>20 Lakh ≤1 crore) | 2% |

| Exceeding Rs. 1 Crore (>1 crore) | 5% |

* this is an amendment portion and will be applicable from 1st July, 2020

Not Applicable of this section

This section is not applicable if the recipient is

1. The government

2. Any banking co.

3. Co-operative society engaged in banking business (i.e. Co-operative bank)

4. Business correspondence of a banking co. or cooperative bank

5. Any white label ATM operator of a banking co. or co-operative bank

6. Any other person notified by the government.

Note: Recipient would be Individual, HUF, Company, Partnership firm or LLP, Local Authority, AOP or BOI.

* To understand this easily please have a look graphical presentation