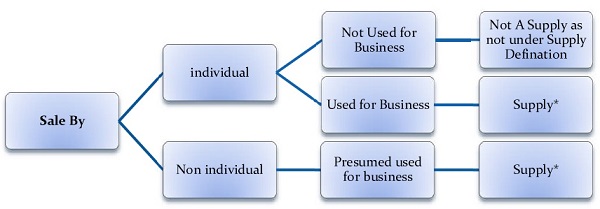

Definition of ‘Supply’ Under section 2(92) read with section 3 ‘Supply’ includes all forms of supply of goods and/or services such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business

Status (Whether Chargeable or Not):

*Further, section 7 (1) (d) of the CGST Act says that all activities listed in Schedule II shall also be termed as a “Supply.

Clause 4 (a) of schedule II says that if goods forming part of the assets of a business are transferred under the directions of the person carrying on the business so as no longer to form part of those assets, whether or not for a consideration, such transfer is also a supply of goods.

Thus. a car which is a part of the business assets of the company as the same is capitalized in the books, if transferred, then vide section 7 (1) (d) read with Schedule II clause 4 (a) of the said Act shall be termed as a “Supply” and vide section 9 shall be a taxable supply. But contrary Judgement exists under Vat regime where the same was not considered as a supply

Method of Computation of GST ( Method)

a) Sales Method

b) Margin Scheme (only for dealers)

Sales Method

Normally GST is charged on the transaction value of the goods

Margin Scheme:

Normally GST is charged on the transaction value of the goods. However, in respect of second hand goods/car , a person dealing is such goods may be allowed to pay tax on the margin.

- In case of a registered person who has claimed depreciation under section 32 of the Income-Tax Act,1961 (43 of 1961) on the said goods, the value that represents the margin of the supplier shall be the difference between the consideration received for supply of such goods and the depreciated value of such goods on the date of supply, and where the margin of such supply is negative, it shall be ignored;

- In any other case, the value that represents the margin of supplier shall be, the difference between the selling price and the purchase price and where such margin is negative, it shall be ignored.

The purpose of the scheme is to avoid double taxation as the goods, having once borne the incidence of tax, re-enter the supply and the economic supply chain.

Valuation of used Goods/Car: (Determination of value in respect of certain supplies)

As per Rule 32(5) of the CGST Rules, 2017, where a taxable supply is provided by a person dealing in buying and selling of second hand goods i.e., used goods as such or after such minor processing which does not change the nature of the goods and where no input tax credit has been availed on the purchase of such goods, the value of supply shall be the difference between the selling price and the purchase price and where the value of such supply is negative, it shall be ignored. The proviso to the above rule further provides that in case of the purchase value of goods repossessed from a unregistered defaulting borrower, for the purpose of recovery of a loan or debt shall be deemed to be the purchase price of such goods by the defaulting borrower reduced by five percentage points for every quarter or part thereof, between the date of purchase and the date of disposal by the person making such repossession.

Rate of GST

After the implementation of GST sale of used and old vehicles were taxed at the same rate as applicable on new vehicles which was 28% + Applicable cess which was up to 15%, and due to this effective tax on sale of old vehicles was upto 43%. This higher rate of tax was causing the burden on trade and industry and due to this there was slow down in the used vehicle market.

Government by issuing the Notification No. 8/2018 Central Tax Rate read with state Tax Notification, reduced the Rate of GST on old and used vehicle as follows:

| S.No. | Chapter, Heading, Sub‑ heading or Tariff item | Description of Goods | Rate |

| (1) | (2) | (3) | (4) |

| 1. | 8703 | Old and used, petrol Liquefied petroleum gases (LPG) or compressed natural gas (CNG) driven motor vehicles of engine capacity of 1200 cc or more and of length of 4000 mm or more.

Explanation. – For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. |

18% |

| 2. | 8703 | Old and used, diesel driven motor vehicles of engine capacity of 1500 cc or more and of length of 4000 mm

Explanation. – For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under. |

18% |

| 3 | 8703 | Old and used motor vehicles of engine capacity exceeding 1500 cc, popularly known as Sports Utility Vehicles (SUVs) including utility vehicles.

Explanation. – For the purposes of this entry, SUV includes a motor vehicle of length exceeding 4000 mm and having ground clearance of 170 mm. and above. |

18% |

| 4. | 87 | All Old and used Vehicles other than those mentioned from S. No. 1 to S.No.3 | 12% |

Condition of Reduction :

- This notification shall not apply, if the supplier of such goods has availed input tax credit as defined in clause (63) of section 2 of the Central Goods and Services Tax Act, 2017, CENVAT as defined in CENVAT Credit Rules, 2004 or the input tax credit of Value Added Tax or any other taxes paid, on such goods

- No Cess will be charged as per the following amendments in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), 1/2017-Compensation Cess (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 720 (E), dated the 28th June, 2017, but no credit should be taken.

(Author is associated with ASRK & ASSOCIATES and can be reached at caronakkothari@gmail.com)

very nice