Amid noise of new taxation on Long Term Capital Gain on sale of Equity Shares and Equity-oriented Mutual Funds and dissent for no relief being given to “middle-class salaried people”, we have missed significant commercially unviable amendment made in Section 80-IAC of Income Tax Act.

Background

Government of India realised that even during economic stagnation in the country, home-grown tech startups like Ola, Flipkart, Myntra, etc were able to pull foreign investments, generate employment and grow at accelerated rate.

In the market of job-seekers, India needed job-creators and startups appeared to be ray of hope. With the intention to promote these job-creators, Section 80-IAC was introduced in Finance Act, 2016 to provide 100% tax-exemption to startups, which is proposed to be amended in Finance Bill 2018.

Earlier Provisions

Section 80-IAC provides for 100% tax exemption on profits earned from “eligible business” by “eligible startup”. This exemption is for 3 consecutive financial years out of 5 financial years starting from year in which startup is incorporated either as a Company or as an LLP.

“Eligible Business” has been defined. In simplified terms, “eligible business” must fulfil two conditions:

- Innovation and commercialisation of “new” products, processes or services

- Driven by “technology or Intellectual Property”

“Eligible Startup” too have been defined to mean –

- Company or LLP incorporated between 1st April, 2016 to 31st March 2019.

- Total turnover should not be more than Rs 25 crore per annum between 1st April, 2016 to 31st March 2021.

- Having certificate of eligible business from the Inter-Ministerial Board (IMB) of Certification.

In essence, it was targeted to boost “new” products, etc which necessary involved “technology”.

Under this constraints only 78 startups were approved/recommended for tax benefits by IMB out of around 1700 applications received till 21st meeting of IMB held on 11/12/2017. (source: https://www.startupindia.gov.in)

Proposed Provisions

In view of the fact that very limited “startups” became “eligible” for Income Tax Benefits, Finance Bill propose to ‘Dilute’ both aspects of definition of “Eligible Business” as follows:

- Instead of “new” product/process/services, amended definition requires “improvement” of products or processes or services

- “Technology or Intellectual Property” has been replaced with more relevant factors, that are, “Scalable Business model” with a high potential of “employment generation” OR “wealth creation”.

It remains to be seen how would Income Tax Department and Inter-Ministerial Board (IMB) of Certification would determine “Scalability”, “Potential of Employment generation” and “Potential of Wealth creation”.

What makes all of above commercially unsound is the amended definition of “Eligible Startups”. New definition requires that the total turnover of business should not exceed “Rs 25 crore per annum” during 7 financial years starting from year in which startup is incorporated as a Company or an LLP.

Contradiction: Commercial Viability vis-a-vis Legal Provisions

On one hand Government wants home-grown businesses to carry out research and develop “improved” products, processes or services. While on other hand it has restricted its “high” potential of Employment Creation and “Wealth Creation” with cap of Rs. 25 crore on turnover.

One may argue, why company would limit its turnover just for the sake of tax benefits, it would rather not take tax benefits and mint money. Here is the illustration:

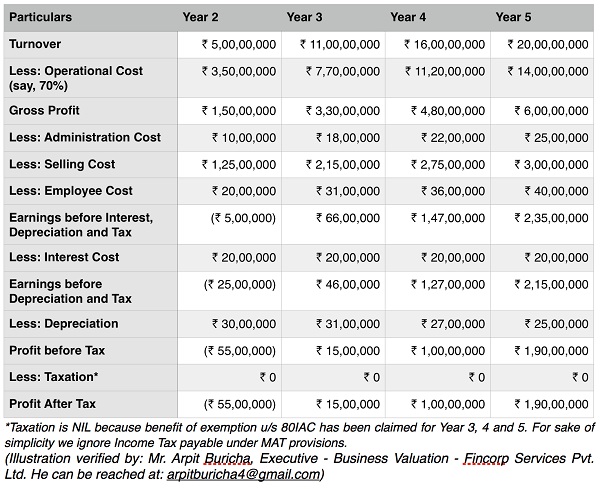

Year 1 – Say, startup incurs loss (due to R&D cost) in year 1 and promoters are able to give shape to idea of an “improved” product.

Year 2 – Startup continues to incur loss (due to high marketing cost) but turnover of Rs 5 crore is achieved.

Year 3 – Given that product is an “improved” product and business is “scalable”, turnover expands to 11 crores and meagre profit margin of around 1% is achieved. Now startup decides to avail tax exemption (for 3 consecutive F.Y.).

Year 4 – Turnover of scalable business further expands to 16 crores (this is 2nd year of exemption irrespective of profits).

Year 5 – Say, turnover increased to 20 crores (this is 3rd and last year of tax exemption irrespective of profits).

Impact of Legal Provision

Now, what if turnover of this “wealth creating” scalable startup is crossing 25 crore in 6th or 7th year? It would mean violation of conditions, and exemption available in 3 preceding years would be withdrawn. Tax exempted earlier will now have to be paid along with interest.

Commercial Viability

To understand financial aspect of business, let us continue above illustration and further assume that-

- The startup is in consumer goods industry.

- Average Total Asset-Turnover ratio of companies in this industry is between 1.5 to 2.

- Considering most optimistic total asset-turnover ratio of 2, startup would require investment of Rs. 2.5 crore to achieve turnover of Rs. 5 crore in 3rd year.

- We may define “wealth-creator”, as ‘a startup that can atleast double this investment with valuation of Rs. 5 crore at end of 5 years (although this is very conservative definition given the facts that currently all really successful startups are valued in terms of millions of USD).

Even by projecting optimistic cashflows as below and assuming cost of capital of 18%, startup’s valuation is approx. Rs. 2.2 crore by applying Discounted Cash Flow approach on “Earnings before Interest, Depreciation and Tax”.

From above analysis it can be seen that the startup could nearly break-even its initial investment after 5 years at given turnover even under optimistic circumstances and thus no wealth is being generated. We can very well conclude that it is nearly unrealistic to create wealth-generating with cap of Rs. 25 crore on total turnover.

Conclusion

Though well intentioned, the startup booster provisions of Section 80-IAC lacks commercial viability and therefore amendments made to S. 80-IAC won’t be able to yield desired results in terms of “employment generation” and “wealth creation”.

This section has potential to be a promoting factor for innovation and startups if turnover limit is rationalised and enhanced to Rs. 250 crore, that is in line with concessional tax rate of 25%.

Author Bio