GSTR 3B is a simpler return that businesses need to file in the first two months of GST (July and August, 2017) instead of the normal returns – GSTR 1, 2 and 3.

Under GST, a registered dealer is required to file three returns every month and one annual return. So, in total 37 returns have to be filed every year. Since filling up these complex forms require a great amount of time and understanding, the government has postponed the filing of GSTR 1,2 & 3 for July and August, 2017.

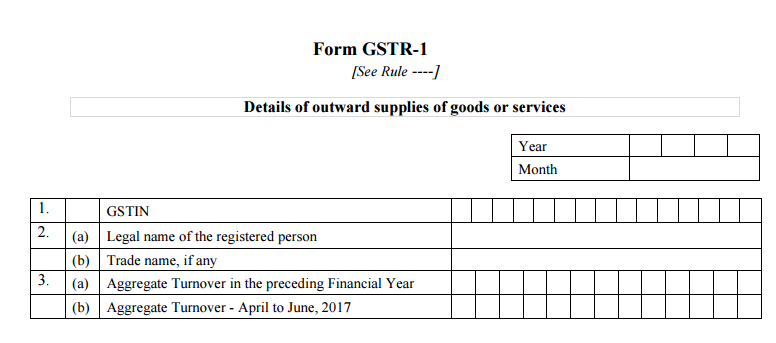

According to the GST law, every registered taxable person is required to submit the details of outward supplies in the GSTR-1. This return is required to be filed within 10 days from the end of the tax period, or the transaction month.

GSTR-1 has a total of 13 headings. However most of these will be prefilled. We need to understand certain terms. These are:

- GSTIN – Goods and Services Taxpayer Identification Number

- UID – Unique Identity Number for Embassies

- HSN – Harmonized System of Nomenclature for goods

- SAC – Services Accounting Code

- GDI – Government Department Unique ID where department does not have a GSTIN

- POS – Place of Supply of Goods or Services – State Code to be mentioned.

GST Returns

| Return Form | What to file? | By Whom? | By When? |

| GSTR-1 | Details of outward supplies of taxable goods and/or services effected | Registered Taxable Supplier | 10th of the next month |

| GSTR-2 | Details of inward supplies of taxable goods and/or services effected claiming input tax credit. | Registered Taxable Recipient | 15th of the next month |

| GSTR-3 | Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax. | Registered Taxable Person | 20th of the next month |

Various section headings under GSTR-1

1. GSTIN: Each taxpayer will be allotted a state-wise PAN-based 15-digit Goods and Services Taxpayer Identification Number (GSTIN). The format of proposed GSTIN has been shown in the image below. The GSTIN of the taxpayer will be auto-populated at the time of return filing.

2. Name of the taxpayer: Name of the taxpayer will also be auto-populated at the time of logging into the common GST Portal.

3. Gross turnover of the taxpayer in the previous FY: This information is required to be filed only in the first year of GST implementation. Next year onwards it will be auto-populated as carried forward balance of the previous year.

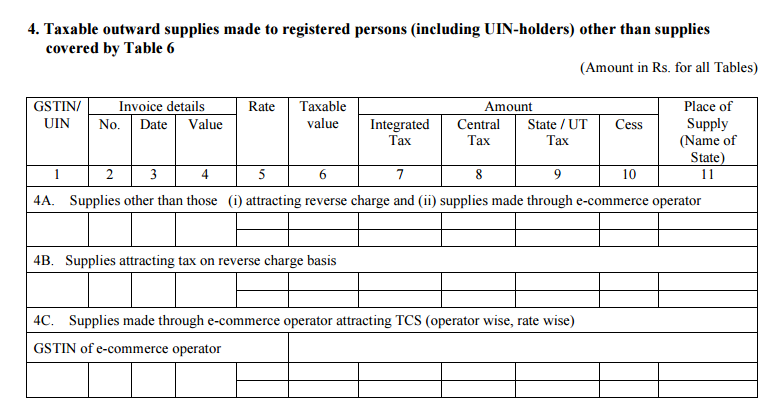

4. Taxable outward supplies made to registered persons (including UIN-holders) other than supplies covered by Table 6: This head will hold the information about the details of all taxable supplies made by the registered taxable person. This head will cover complete details of Normal Taxable Supplies, Supplies under Reverse Charge, and Supplies by way of an E-Commerce operator.