Annual Return

Annual Return

1. Company

Annual return in a layman’s term means a return which a company is required to file annually and further it is a snapshot of company information as they stood on the close of the financial year. Section 92 of the Companies Act, 2013 and the Companies (Management and Administration) Rules, 2014 deals with filling of Annual Return of a Company

The basic purpose of filing annual return with the Registrar of Companies (‘ROC’) is to provide the annual information about the Company to the ROC and its members about the Company’s general compliances.

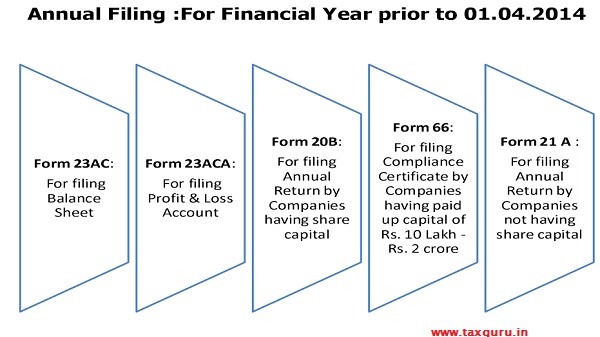

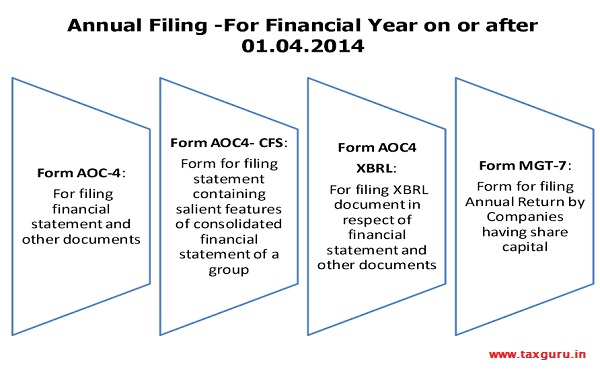

Annual Filing Eforms:

As a part of Annual Filing, Companies incorporated under the Companies Act 1956 or Companies Act 2013, are required to file the following eForms with the Registrar of Companies (ROC):

*The annual return, filed by a listed company or, by a Company having paid-up capital of Rs.10 Crores or more OR turnover of Rs.50 Crores or more shall be certified by a PCS in Form No. MGT-8

*Extract of Annual Return: An extract of the annual return in Form No MGT-9 shall form part of the Board’s report.

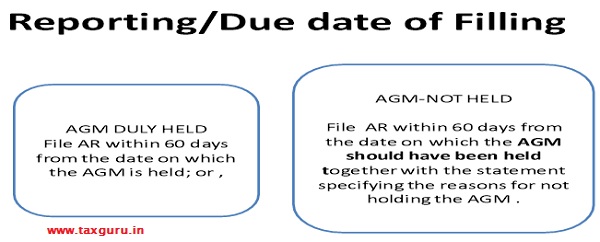

Due Date of Filing Annual Return:

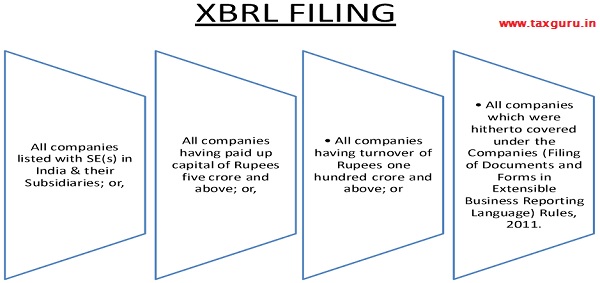

XBRL FILING:

There are certain classes of Companies which are required to file their Balance sheet and Profit and Loss or Financial Statements in XBRL:

*However, Banking, Power, NBFC and Insurance Companies are exempted from XBRL filing till further orders.

**For filing 23AC/ACA XBRL stakeholders are required to use taxonomy based upon new Schedule VI of the Companies Act, 1956.

***For filing AOC-4 XBRL stakeholders are required to use taxonomy based upon Schedule III of the Companies Act, 2013

2. Foreign Company:

Section 384(2) of Companies Act, 2013 and rule 22.5 of the Companies Act,2014 provides provisions relating to preparation and filing of Annual Return, preparation of Book of Account and manner in which they may be kept.

Companies (Registration of Foreign Companies) Rules, 2014

Every foreign company shall prepare and file, within a period of sixty days from the last day of its financial year, to the ROC an annual return in Form FC.4 along with such fee as provided in the Companies (Registration Offices and Fees) Rules, 2014 containing the particulars as they stood on the close of the financial year

Due Date of Filing: within a period of 60 days from the last day of its financial year

3. Nidhi Company

Section 406 of the Companies Act, 2013 and rule 21 of Nidhi Rules, 2014 provides rules relating to preparation and filing of Annual Return.

Every Company covered under rule 2 shall file half yearly return with the Registrar in Form NDH-3 along with such fee as provided in Companies (Registration Offices and Fees) Rules, 2014.

Due date of Filing: within 30 days from the conclusion of each half year duly certified by a CS in Practice or CA in practice or Cost Accountant in Practice.

4. Dormant Company

Section 455(5) of the Companies Act, 2013 read with rule 7 and 8 of the Companies Rules,2014 provides provisions relating to preparation and filing of Annual Return.

A dormant company shall file an annual “Return of Dormant Company” in form MSC-3 which indicates the financial position of the company and which shall be duly audited by a chartered accountant in practice.

Due date of Filing: This should be filed within 30 days from the end of each financial year. i.e. on or before 30th April every year.

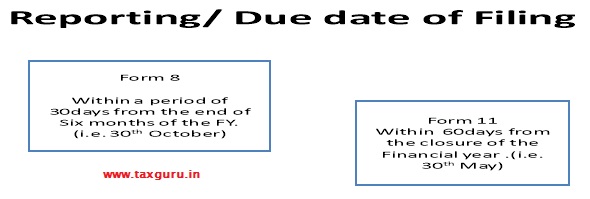

5. Limited Liability Partnerships

Pursuant to rule 25(1) of Limited Liability Partnerships Rules, 2009 provides rules relating to preparation and filing of Annual Return.

Limited Liability Partnership (LLP) under the Limited Liability Partnership Act, are required to file the following Forms with the Registrar every year:

Form 8: Statement of Account & Solvency

Form 11: Annual Return

Due Date of Filing Annual Return:

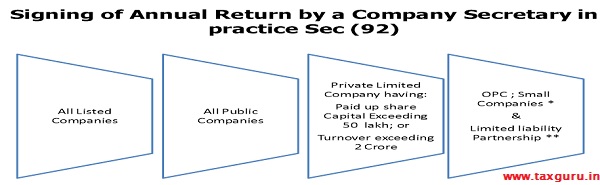

Signing & Certification of Annual Return

*where there is no company secretary, by the director of the company.

**In Case total obligation of contribution of Partners of the LLP exceeds Rs.50lakhs or turnover exceeds Rs. 5 crores.

Certification by PCS:

The annual return, filed by a listed company or, by a company having such paid-up capital of Rs.10 Crores or more OR turnover of Rs.50 Crores or more shall be certified by a PCS in Form No. MGT-8 stating that the annual return discloses the facts correctly and adequately and that the company has complied with all the provisions of this Act.

Disclaimer: The entire contents of this document have been developed on the basis of relevant information and are purely the views of the authors. Though the authors have made utmost efforts to provide authentic information however, the authors expressly disclaim all and any liability to any person who has read this document, or otherwise, in respect of anything, and of consequences of anything done, or omitted to be done by any such person in reliance upon the contents of this document.