Case Law Details

Bhalang Singh Phanbuh Vs Commissioner of CGST & Central Excise (CESTAT Kolkata)

The appeal arose from a Show Cause Notice (SCN) dated 08.11.2019 issued on the basis of details contained in Form 26AS of the appellant’s Income Tax Returns for the period 2014-15 to 2017-18. Invoking the extended period, the Department demanded Service Tax of Rs. 6,25,966/-. The adjudicating authority confirmed the demand. The Commissioner (Appeals) dismissed the appeal solely on the ground that it had been filed beyond the statutory period of 60 days and the additional condonable period of 30 days. The appellant challenged that order before the Tribunal.

On limitation relating to the filing of the appeal before the Commissioner (Appeals), the appellant submitted that the Order-in-Original dated 14.08.2020 had been passed during the COVID period and was never received. According to the appellant, knowledge of the order came only after a bank account attachment order dated 27.09.2022. The appellant thereafter sought a copy of the order from the jurisdictional authorities through letters dated 25.11.2022 and 04.01.2023, filed a writ petition before the Meghalaya High Court, and subsequently submitted an RTI application on 23.02.2024. The Department supplied the Order-in-Original in response to the RTI, and the appeal before the Commissioner (Appeals) was filed on 23.04.2024. The Tribunal observed that the appellant had consistently attempted to obtain the order and noted that there would have been no reason to approach the High Court if the order had already been received. Holding that the appeal had been filed within the prescribed period after receipt of the Order-in-Original, the Tribunal set aside the Commissioner (Appeals)’ order dismissing the appeal on limitation.

With the consent of both sides, the Tribunal proceeded to decide the appeal on merits instead of remanding the matter. The appellant argued that the Department’s case rested entirely on Form 26AS and that the entries under Sections 194C and 194IB of the Income Tax Act represented amounts paid by the appellant rather than amounts received. The Revenue contended that Form 26AS established receipt of consideration from entities including ABC India Ltd., Amrit Hatcheries Pvt. Ltd. and HPCL and that the SCN had been issued after verification of the appellant’s balance sheet and profit and loss account.

Examining the Form 26AS entries, the Tribunal held that the appellant’s contention regarding Section 194C was not acceptable. Referring to the sample Form 26AS, it found that ABC India Ltd. had paid Rs. 8,51,660 to the appellant and that the statement reflected consideration received by the appellant rather than amounts paid by the appellant. Accordingly, the Tribunal held that the appellant had no case on merits regarding the amounts reflected under Section 194C.

Regarding the entries under Section 194IB, the Tribunal observed that the provision related to TDS deducted by a lessee on rent paid to a lessor. It noted that the entries appeared to relate to consideration paid by Amrit Hatcheries Pvt. Ltd. and HPCL for premises allegedly leased by the appellant. The appellant contended that the premises let to Amrit Hatcheries were used for poultry or dairy activities exempt from Service Tax, but the Tribunal recorded that no proper evidence had been produced to support that contention and held that no proper defence had been made out on merits on that issue.

The Tribunal then considered the appellant’s contention that the SCN was barred by limitation. It found that the SCN had been issued solely on the basis of Form 26AS without any further enquiry regarding the nature of services rendered to HPCL or other entities. The record showed that the Department had sought information regarding the appellant’s turnover for 2014-15 on 22.11.2016, to which the appellant had replied on 28.11.2016 with details of Service Tax paid. No further action was taken for about three years, after which fresh enquiries were made on 16.10.2019 and the SCN was issued on 08.11.2019 based solely on Form 26AS.

The Tribunal referred to decisions relied upon by the appellant, including Homeopathic Medical Publishers v. Commissioner of CGST & Central Excise, Tabassum Enterprises v. CGST & CX, Rishu Enterprise v. Commissioner of C.G.S.T. & Excise, Dibrugarh, Quest Engineers & Consultant Pvt. Ltd. v. Commissioner of C.G.S.T. & C.Ex., Allahabad, and the Gujarat High Court decision in Nimeshbhai Gunvantbhai Patel v. Union of India. It also referred to the CBIC circular dated 26.10.2021 reiterating that show cause notices should not be issued indiscriminately on the basis of differences between ITR-TDS data and Service Tax returns without proper verification.

The Tribunal observed that the cited decisions consistently held that where a show cause notice is issued solely on the basis of Form 26AS or Income Tax Returns by invoking the extended period, without proper verification or investigation, the demand cannot legally survive. It further noted that, in the present case, the Revenue had not explained the delay of about three years before making further enquiries from a registered assessee. Holding that the ratios of the cited decisions were squarely applicable, the Tribunal set aside the confirmed demand on the ground of limitation. The appeal was allowed with consequential relief, if any, as per law.

Recent Cases Discussed:

- Homeopathic Medical Publishers Vs Commissioner of CGST & Central Excise, Final Order No. 86910/2025 dated 25.11.2025.

- Tabassum Enterprises vs. CGST & CX, Final Order No. 75452/2025 dated 19.09.2025 (Service Tax Appeal No. 75037 of 2025).

- Nimeshbhai Gunvantbhai Patel v. Union of India, (2024) 25 Centax 122 (Guj).

- M/s. Rishu Enterprise vs Commissioner of C.G.S.T. & Excise, Dibrugarh, Final Order No. 75177 of 2024 dated 08.02.2024 in Service Tax Appeal No. 75509 of 2022 (CESTAT, Kolkata).

- M/s. Quest Engineers & Consultant Pvt. Ltd. v. Commissioner of C.G.S.T. & C.Ex., Allahabad, 2022 (58) G.S.T.L. 345 (Tri. – All.).

FULL TEXT OF THE CESTAT KOLKATA ORDER

Based on the details contained in Form 26 A.S. of the Income Tax Returns, a Show Cause Notice was issued to the appellant on 8.11.2019 for the services provided during the period 2014-15 to 2017-18. The Show Cause Notice was issued by invoking the extended period provisions demanding Service Tax of Rs.6,25,966/-.

2. After due process, the adjudicating authority confirmed the demand. Upon appeal, the Commissioner (Appeals) has dismissed the appeal filed by the appellant on the ground that the same was filed beyond the appealable period of 60 days plus the condonable period of 30 days. Being aggrieved, the appellant is before the Tribunal.

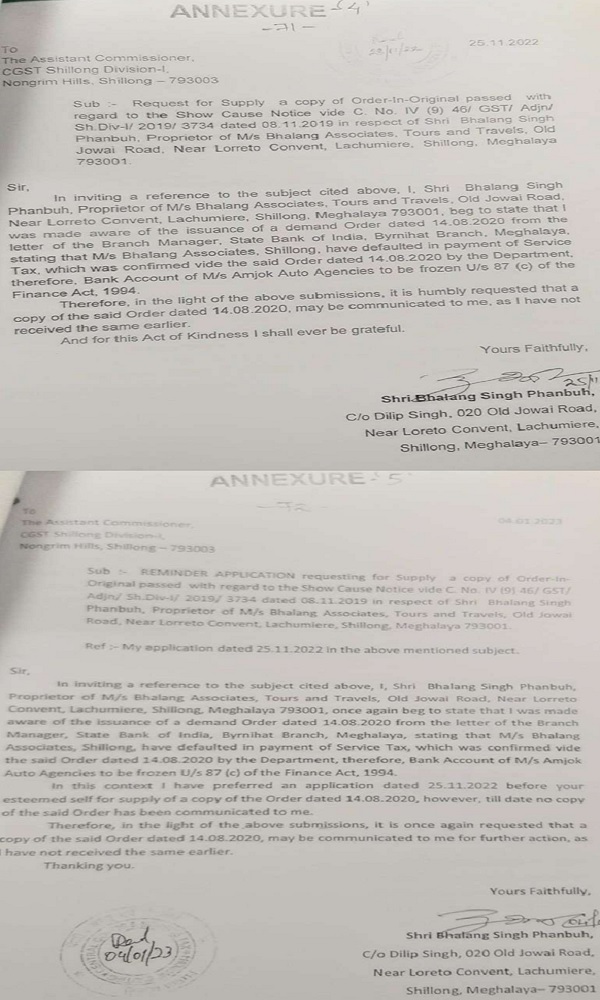

3. The Learned Consultant appearing on behalf of the appellant first takes me through the issue of delayed filing of the appeal before the Commissioner (Appeals). He submits that the OM dated 14.08.2020 was passed during the COVID pandemic and was not received by the appellant at that time. They have come to know that such an order was passed when an order towards attachment of Bank Account was passed by the CGST authorities on 27.09.2022. They have followed up with the jurisdictional authorities to supply the copy of the OIO. Since they were not given the copy of the OM for filing the appeal, the appellants have filed an appeal before the High Court of Meghalaya. The High Court has directed the appellant to take up the matter with the concerned appellant authority. After this, the appellant has filed one RTA application on 23.02.2024 (page no. 73 of the appeal book). In response to the RTA application filed by the appellant, the CPIO & Asst Commissioner on 24.02.2024 granted and copy of the OM No. 10 dated 14.08.2020. After receiving this OM on 24.02.2024, the appellant has filed the appeal before the Commissioner on 23.04.2024.

4. The Learned Consultant submits that if all these facts are taken together, then it would be seen that the appellant has filed the appeal within one month from the date of receipt of the OM by way of RTA application. In view of these submissions, he prays that it may be held that the appeal before the Commissioner (Appeals) was filed within the normal period only.

5. He further submits that since the issue is in a short compass, the appeal may be decided at the Tribunal itself. The Kolkata Bench of the Tribunal, in Shri G. Pradeep PiHai (Service Tax Appeal No. 75532 of 2024), after setting aside the order of the Commissioner (Appeals) on limitation and condoning the delay, decided the appeal on merits itself, holding that remand was unnecessary where the record was complete and the controversy could be finally adjudicated.

6. He submits that the entire case has been built based on the 26 AS statement. The Department has taken the stand that for the period 2014-15 to 2017-18, the appellant is shown to have received amounts from ABC India Ltd., Amrit Hatcheries Ltd., HPCL, etc. Based on these receipts, the demand was quantified at Rs.6,25,966/-.After due process, the adjudicating authority has confirmed the demand. As submitted above, the Commissioner (Appeals) has not gone into the merits but has dismissed the appeal on account of limitation itself.

7. Learned Consultant submits that the appellant has a strong case both on merits as well as on account of limitation. He submits that the 26 AS statement relied upon by the Revenue shows that the TDS Section of the Income Tax Act is 194C and 194IB as can be seen in the table contained in the Show Cause Notice and OIO. He submits that these are the Sections of Income Tax wherein the 26 AS depicts the amounts paid by the appellant and not the amounts received by the appellant. Therefore, he submits that the entire Show Cause Notice which is based on the quantification done as per 26 AS is erroneous. On this ground, he says that since the appellant has not received the amount but has actually paid the amount which is reflected in 26 AS, the appeal should be allowed on merits.

8. He further takes the stand that the Show Cause Notice issued on 8.11.2019 pertains to the period 2015-16 to 2017-18 and the demand is quantified only based on the Form 26AS of Income Tax Return. Hence, it is submitted that the SCN is time-barred. He relies on various case laws wherein it has been held by the Benches of Tribunal that when the Show Cause Notice is issued based on the Form 26 AS / ITR returns without proper verification and investigation, the demand cannot be sustained. Based on these submissions, he prays that the appeal may be allowed even on account of limitation.

9. The Learned AR takes the stand that the appellant has filed the appeal before the Commissioner (Appeals) in a delayed way, much beyond the condonable period of 30 days after the normal period of 60 days allowed for filing such appeals. Therefore, he justifies the dismissal of the appeal by the Commissioner (Appeals). Further, he reiterates the findings of adjudicating authority. He submits that Form 26 AS clearly proves that the appellant has received the amount from HPCL, ABC, India Ltd and others. Therefore, the Revenue has correctly taken these as the consideration received by the appellant for the services provided by the and accordingly the demand has been confirmed. He further submits that only in view of the Income Tax Returns and Form 26 AS obtained from the income tax Department, the appellant was made to give the details of the Balance Sheet and profit and loss account and only after verification of these documents, the Department could issue the Show Cause Notice. Therefore, he justifies the confirmed demand for the extended period. In view of these submissions, he prays that the appeal may be dismissed.

10. Heard both sides and perused the appeal papers and the documents placed before me.

11. I first take up the issue as to whether the appeal has been filed before the Commissioner (Appeals) in a belated way as has been held by him or within the correct period as is being canvassed by the appellant. I find that the order has been passed on 14.08.2020 which happens to be the Covid period. The appellant received a letter about the Account Freezing Notice on 27 September 2022. This has been claimed by them before the Hon’ble Meghalaya High Court. After this, the appellant has approached the jurisdictional officials for a copy of the OM, as can be seen from the following extracted copies of the letters:

12. The above letters show that the appellant has requested the jurisdictional Asst Commissioner on 25.11.2022 and when no response was received one more letter was addressed to him on 04.01.2023.

13. When the OIO was not supplied by the Asst Commissioner, the appellant has filed a Writ Petition before the High Court of Meghalaya seeking the condonation of delay as well as copy of the OIO. The Order of the High Court is extracted below:

14. The Hon. High Court has refused to fully interfere in this issue which is required to be taken up before the proper appellate forum. However, leave has been granted to the appellant to approach the proper authority for appeal.

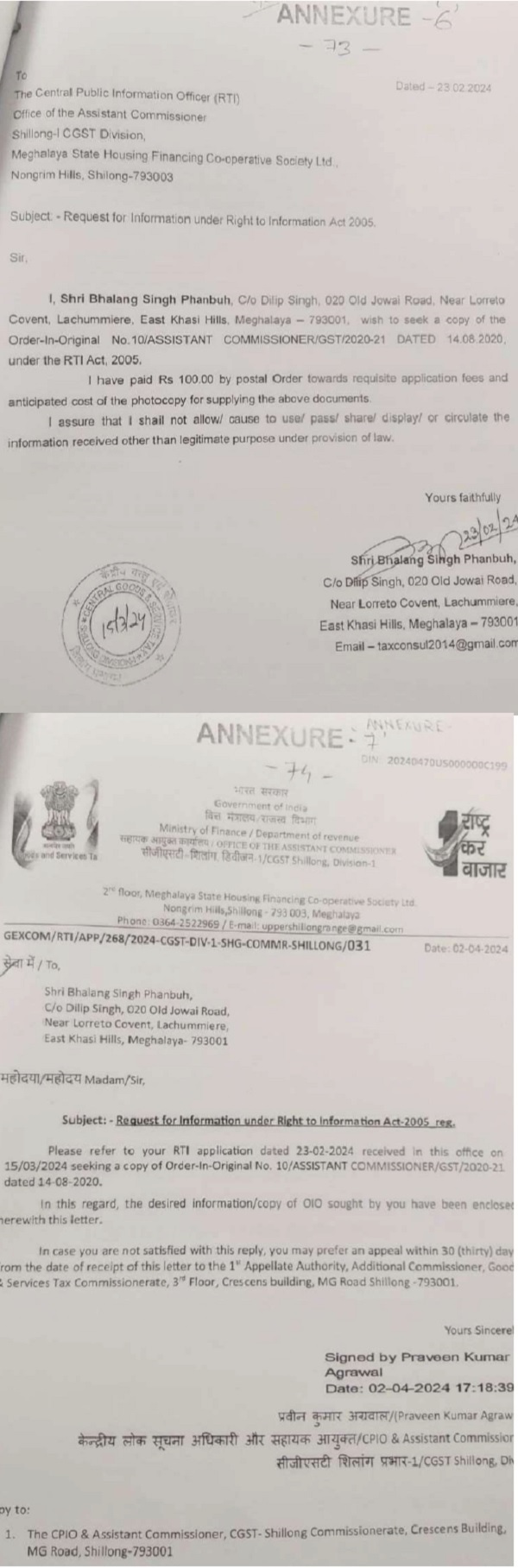

15. After this, the appellant has filed an RTI application on 23.02.2024. In response to their RTI application, the Department has responded by letter dated 02.04.2024 enclosing therewith copy of the OM No. 10 dated 14-08-2020, as can be seen from the following letters:

16. Thereafter, the appellant has filed the appeal before the Commissioner (Appeals) on 23.04.2024. If the follow up letters by the appellant seeking copy the OIO, High Court’s order, RTI application and response to RTI are viewed harmoniously, it can be seen that the appellant has made all the efforts to get hold of the copy of the OIO. If they had really received the OIO, there was no necessity to knock the doors of the High Court, which would entail time, resources and money.

17. Once the OM has been received by him on 02.04.2024, within one month from this date, they have filed their appeal before the Commissioner (Appeals). Therefore, I hold that the appellant has filed the appeal within the specified period which is available for filing the appeal before the Commissioner (Appeals). On this ground, the impugned order is set aside.

18. After going through the appeal papers and the documentary evidence placed before me, I find that the issue is in a short compass. Therefore, with the consent of both the sides, I have taken up the appeal itself for disposal.

19. It is observed that the Revenue has built up the entire case based on the Form 26-AS statement for the period 2014-15 to 2017-18. The details of the amounts and the name of the clients and the relevant TDS Section of the Income Tax is as per the following table:

| Year | Name | Amount credited | TDS Section of Income Tax Act |

| 2014-15 | ABC India Ltd. | 1895931 | 194C |

| Amtit Hatcheries Pvt Ltd. | 2218368 | 194IB | |

| HPCL | 872379.4 | 194C | |

| 2015-16 | ABC India Ltd. | 851660 | 194C |

| HPCL | 1397561 | 194C | |

| 2016-17 | HPCL | 629236 | 194C |

| 2017-18 | HPCL | 15400 | 194IB |

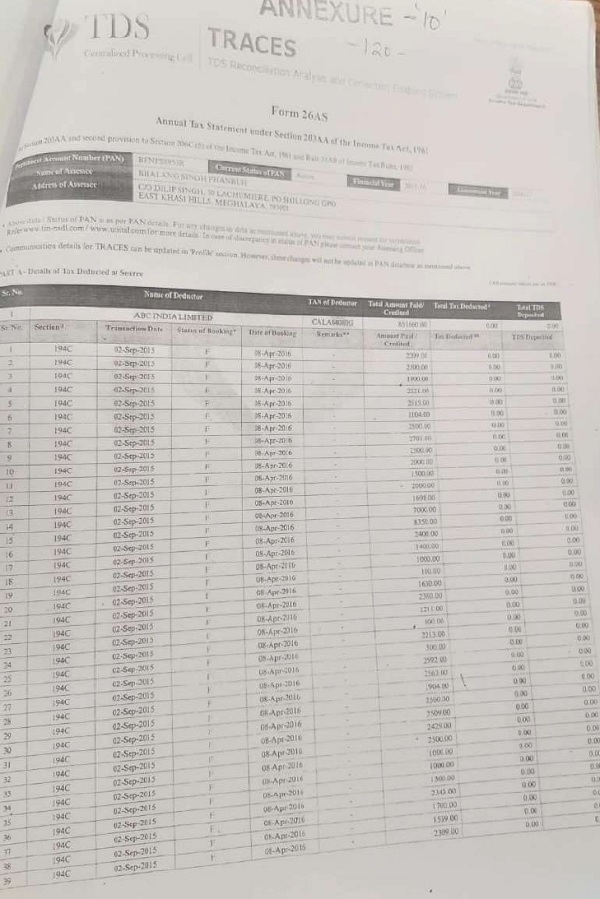

20. From the above table, it is seen that in case of ABC India Ltd and HPCL up to 2016-17, the Income Tax Section shown is 194C. On going through the Section 194C, I find that this is applicable where the amounts are paid to the contractors or subcontractors carrying out any work for the clients. In such cases, the client should deduct the tax at source and the total amount paid vis-à-vis the tax deducted should be shown. I have also gone through the actual Form 26-AS attached by the appellant in the appeal paper. One sample Form 26-AS is reproduced below:

21. From the above statement, it can be seen that ABC India has paid 8,51,660/- and has not deducted any TDS from the appellant. The statement very clearly shows that this is a case where the appellant has received the consideration from ABC India Ltd and this is not the case where the appellant has paid the amount to ABC India Ltd. Therefore, I do not subscribe to the submissions made by the appellant that this is a case where the amount shown in Form 26-AS is the amount paid by the appellant to ABC India Ltd. Therefore, in respect of the amounts shown under Section 194C, the appellant has no case on merits.

22. Coming to the two entries under TDS Section 194-IB, it is seen that this is on account of TDS to be deducted by the lessee when the premises are taken on rent. The amount shown in Form 26-AS is in respect of the following amounts:

| 2014-15 | Amtit Hatcheries Pvt Ltd. | 2218368 | 194IB |

| 2017-18 | HPCL | 15400 | 194IB |

23. Under this Section 1941B, TDS is deducted by the person, who is paying the rent to the lessor. In this case, it looks like the appellant has given premises on lease to Amrit Hatcheries and HPCL, for which they have paid the consideration. In respect of Amrit Hatcheries, the appellant has taken the stand that the same has been given for poultry / dairy activities, which is exempted from payment of Service Tax. No proper evidence has been enclosed in the appeal to support his contention. Therefore, I take the view that no proper defence has been made out by the appellant on merits on this issue.

24. Now, I take up the issue of the time bar as has been canvassed by the appellant.

25. From the records, it is very clear that the Show Cause Notice has been issued purely based on the Form 26-AS details. No further enquiries have been made as to what kind of service was rendered by the appellant to HPCL and others. From the SCN, it is observed that the appellant is registered with S T Regn No.BFNPS8953RSD001. A query towards 2014-15 turnover was raised about the Service Tax payment on 22.11.2016 [RUD-1], for which the appellant has filed his reply on 28.11.2016 [RUD-2] and has given the details of Rs.8,02,798 towards the Service Tax paid by him. Thereafter no action was taken by the Department. After about 3 years on 16.10.2019, subsequent enquires have been made from the appellant. Finally, the SCN has been issued on 08.11.2019 solely based on the consideration shown in the Form 26 AS of Income Tax as has been observed from the Table discussed above.

26. The Tribunals have been consistently holding that when the Show Cause Notice is issued purely based on the Form 26-AS Income Tax returns without any proper corroborative evidence towards the service provided, the same is not legally sustainable. I have for reference the following case laws:

Homeopathic Medical Publishers

Vs Commissioner of CGST & Central Excise

FINAL ORDER NO: _86910/2025 dated 25/11/2025

3. Learned Chartered Accountant also placed reliance on the decision of Hon’ble High Court of Gujarat in Nimeshbhai Gunvant bhai Patel v. Union of India [(2024) 25 Centax 122 (Guj)] and several decisions of the Tribunal invalidating proceedings commenced with no allegation other than discrepancy between returns filed under the Finance Act, 1994 and under Income Tax Act, 1961 respectively. Relying upon the decision of the Hon’ble High Court of Madras, in Commissioner of Customs (Imports), Chennai v. Flemingo (DFS) Pvt Ltd [2010 (251) ELT 348 (Mad)], and of the Tribunal, in Shubham Electricals v. Commissioner of Central Excise & Service Tax, Rohtak [2015 (40) STR 1034 (Tri.-Del.)], it was submitted that proceedings initiated by show cause notice which did not lay out specific identification of chargeability to levy on identified taxable activity was invalid in law.

6. It would appear that the initiation of recovery proceedings under section 73 of Finance Act, 1994 solely on the basis of information received from third parties was so rampant and undesirable that the Central Board of Indirect Taxes & Customs (CBIC), vide circular dated 26th October 2021, instructed that :

‘2. In this regard, the undersigned is directed to inform that CBIC vide instructions dated 01.04.2021 and 23.04.2021 issued vide F.No.137/472020-ST, has directed the field formations that while analysing ITR-TDS data received from Income Tax, a reconciliation statement has to be sought from the taxpayer for the difference and whether the service income earned by them for the corresponding period is attributable to any of the negative list services specified in Section 66D of the Finance Act, 1994 or exempt from payment of Service Tax, due to any reason. It was further reiterated that demand notices may not be issued indiscriminately based on the difference between the ITR-TDS taxable value and the taxable value in Service Tax Returns.

3. It is once again reiterated that instructions of the Board to issue show cause notices based on the difference in ITR-TDS data and service tax returns only after proper verification of facts, may be followed diligently. Pr. Chief Commissioner /Chief Commissioner (s) may devise a suitable mechanism to monitor and prevent issue of indiscriminate show cause notices. Needless to mention that in all such cases where the notices have already been issued, adjudicating authorities are expected to pass a judicious order after proper appreciation of facts and submission of the noticee.’

7. The Hon’ble High Court of Gujarat, in re Nimeshbhai Gunvant bhai Patel, has held, in like circumstances and after narration of reconciliation offered by assessee, that

’16. …Therefore, considering the facts on record it is evident that the petitioner was not at all liable for service tax and the respondent authorities could not have assume the jurisdiction to issue the show cause notice on the basis of the data provided by the Income Tax Department in Form-26AS and thereafter failed to consider the details provided by the petitioner in reply to the show cause notice.

17. It is also pertinent to note that no justification is given in the impugned show cause notice as well as the order-in original for assumption of jurisdiction by invoking extended period of 5 years under the proviso to subsection-1 of section 73 of the Finance Act,

18. In view of the foregoing reasons, the impugned show cause notice is not tenable as the same is issued without jurisdiction and consequently the order-in-original also wouldn not survive….’

8. In view of our findings supra and the decisions aforesaid, the lack of allegation in the show cause notice, that any, or even part, of the impugned income was not attributable to any of the claimed activities, places the invoking of section 73 of Finance Act, 1994 in jeopardy at the threshold itself. It would appear that the adjudicating authority was influenced almost entirely by the additional income reported in returns prescribed in another jurisdiction.

9. In view of the above, we set aside the impugned order and allow the appeal.

Tabassum Enterprises vs.

CGST & CX

Final Order No.75452/2025 dated 19.09.2025 (Service Tax

Appeal No.75037 of 2025)

“5. I find that the present demand has been raised and confirmed on the basis of data provided by the Central Board of Direct Taxes (CBDT). It is observed that the said demand has been confirmed without the support of any independent or corroborative evidence from the Service Tax records. Such mechanical reliance on Income Tax data, without verification of the nature of receipts or proof of taxable services rendered, is impermissible in law. It is a settled legal position that mere entries in income tax returns or Form 26AS cannot, by themselves, establish liability under the Finance Act, 1994, unless corroborated by evidence demonstrating rendition of taxable service.

5.1. In support of this view, I rely upon the decision in the case of M/s. Rishu Enterprise vs Commissioner of C.G.S.T. & Excise, Dibrugarh, in Final Order No. 75177 of 2024 dated 08.02.2024 in Service Tax Appeal No. 75509 of 2022 [CESTAT, Kolkata], wherein this Tribunalhas observed as under: –

“8. In view of the judicial pronouncement of this Tribunal, we hold that merely on the basis of Form 26-AS issued by the Income Tax Department, the demand of Service Tax is not sustainable against the appellant.

………..

11. In view of this, we hold that the impugned demand is not sustainable against the appellant on the basis of the details provided by the Income Tax Department in Form 26AS and the extended period of limitation is not invokable.”

5.2. The same view has been held by the Tribunal at Allahabad in the case of M/s.Quest Engineers & Consultant Pvt. Ltd. v. Commissioner of C.G.S.T. &C.Ex., Allahabad [2022 (58) G.S.T.L. 345 (Tri. – All.)]observing as follows: –

“12. …. ….We further find that Form No. 26AS is not a statutory document for determining the taxable turnover under the Service Tax provisions. We find that Form No. 26AS is maintained on cash/ receipt basis by the Income Tax Department for the purpose of tax deducted at source, etc. being the relevant data for Income Tax. Whereas under the Service Tax provisions, the service tax is chargeable on mercantile basis (accrual basis) on the service provided whether the value of such service is received or not. Thus, we find that the whole basis of show cause notice is incorrect and/or misconceived.”

5.6. Following the ratio of the decisions cited supra, I hold that the demand of service tax confirmed in the impugned order, solely relying the data received from CBDT, without adducing corroborative evidence in support, cannot be sustained. Thus, I observe that the demand confirmed in the impugned order is liable to be set aside on this ground itself.”

27. The above cases show that the High Court and co-ordinate Benches of the Tribunals have been consistently holding that when the SCN is issued solely on the basis of 26AS / Income Tax Returns by invoking the extended period provisions, without any proper verification and investigation, the demand cannot legally survive. In the present case, not only the SCN was issued by relying on 26AS, but also Revenue has not been able to explain as to why there is a delay of about 3 years to even make a query from a registered assessee.

28. I take the view that the ratios laid down in the cited case laws are squarely applicable. Accordingly, I set aside the confirmed demand on account of limitation.

29. The appeal stands allowed. The appellant would be eligible for consequential relief, if any, as per law.

(Pronounced in the open court on…07.07.2026..)

Author Bio