The Finance Bill, 2026 introduces several amendments to Income Tax Act, with the objective of simplifying compliance, rationalising penalties, promoting investment, and furthering the process of decriminalisation of tax offences.

The Finance Act, 2026 has been notified on 30th March 2026. The Chapter- II, Sections 2 to 3 (Page 2 to 29) relates to Rates of Income Tax, Chapter- III, Sections 4 to 34 (Page 30 to 40) amends Income Tax Act 1961, Sections 35 to 129 (Page 41 to 71) amends Income Tax Act 2025, Chapter- IV Sections 130 to 144 (Pages 72 to 76) provide for The Foreign Assets of Small Taxpayers Disclosure Scheme 2026, Chapter- VI Part III Section 160 (Page 79) amends Black Money Act. The main amendments/ provisions of The Finance Act 2026, are summarised as follows:

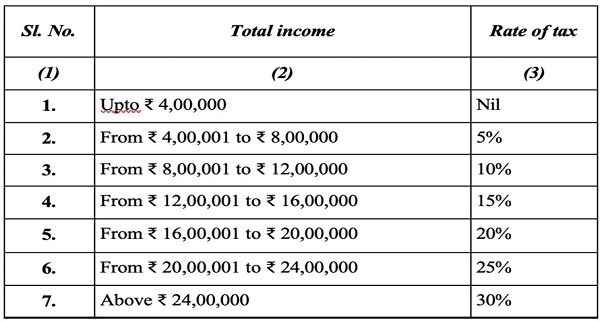

1. Income Tax Slab Rates for Tax Year 2026-27:The Income Tax rates applicable for Tax Year 2026-27 are the same as that for the Previous Year 2025-26. The Income Tax rates as applicable in respect of the total income of a person, being an individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person for the Tax Year 2026-27 are given in Annexure- A enclosed.

2. Increase in Tax Rates of Securities Transaction Tax: The Securities Transaction Tax (STT) was introduced by the Finance Act 2004 as a mechanism for efficient collection of tax on transactions in specified securities carried out through recognised market infrastructure. The rates of STT have been revised periodically to reflect changes in market structure and trading behaviour. It has been amended to increase the rate of STT on sale of an option in securities from 0.1 per cent to 0.15 per cent of the option premium, on sale of an option where the option is exercised from 0.125 per cent to 0.15 per cent of the intrinsic price, and on sale of a future in securities from 0.02 per cent to 0.05 per cent of the traded price.

(Effective from 1st day of April 2026)

3. Taxation of Buyback of Shares: As per the existing provisions, consideration received by a shareholder on buy-back of shares by a company is treated as dividend income under section 2(40)(f) of the Income Tax Act 2025 and taxed accordingly, while the cost of acquisition of the shares extinguished on buy-back is recognised separately as a capital loss under section 69 of the Act. It has been amended to provide that consideration received on buy-back shall be chargeable to tax under the head “Capital gains” instead of being treated as dividend income. It has also been provided that, in the case of promoters, the effective tax liability on gains arising from buy-back shall be 30%, comprising tax payable at the applicable rates together with an additional tax. In case of promoter companies, the effective tax liability will be 22%.

(Effective from 1st day of April 2026)

4. Exemption for Sovereign Gold Bond: The section 70(1)(x) of the Income Tax Act 2025 provides an exemption from capital gains tax in respect of income arising from redemption of Sovereign Gold Bonds issued by the Reserve Bank of India under the Sovereign Gold Bond Scheme, 2015. It has been amended to provide that the exemption shall be available only where the Sovereign Gold Bond is subscribed to by a subscriber at the time of original issue and is held continuously until redemption on maturity, for all Sovereign Gold Bonds issued by the Reserve Bank of India from time to time.

(Effective from 1st day of April 2026)

5. Relaxation obtaining TAN by a Resident Individual or HUF, where the Seller of the Immovable Property is a Non Resident:As per existing section 397(1)(c) of Income Tax Act 2025, if a person buys an immovable property from a resident seller, the person is not required to obtain TAN, to deduct tax at source. However, where seller of the immovable property is a non-resident, the buyer is required to obtain TAN to deduct tax at source. It has been amended to provide that resident individual or Hindu undivided family, is not required to obtain TAN to deduct tax at source in respect of any consideration on transfer of any immovable property.

(Effective from 1st day of October 2026)

6. Enabling Filing of Declaration for No Deduction of Tax at Source to a Depository: As per existing provisions of section 393(6) of Income Tax Act 2025, a written declaration is to be filed by the assessee for no deduction of tax at source to the person responsible for paying any income or sum of the nature as specified. Investors earning income from multiple securities often face a cumbersome process, needing to submit separate forms to all entities. It has been amended to allow filing of the declaration to the depository which in turn shall provide such declaration to the person responsible for paying such income. Also, the time limit for furnishing the declaration received by person responsible for paying income, to the prescribed Income tax authority have been changed from monthly basis to quarterly basis.

(Effective from 1st day of April 2027)

7. Application of TDS on Supply of Manpower: As per existing provisions under section 393(1) of Income Tax Act 2025, TDS is to be deducted, in the case of payments made to contractors for carrying out any work, in the case of fees paid for professional or technical services, in the case of payments by way of commission or brokerage, and others as provided. It has been amended to include supply of manpower under the ambit of ‘work’, so that provisions relating to payments made to contractors for carrying out any work, becomes applicable.

(Effective from 1st day of April 2026)

8. Exemption for Disability Pension to Armed Force Personnel: Disability pension is granted to members of the Armed Forces who are invalided out of service on account of a bodily disability that is attributable to, or aggravated by, military, naval or air force service, and comprises a service element and a disability element. The exemption first provided under the Indian Income Tax Act 1922 was continuing, through the repeal and savings clause, and notifications, administrative instructions and clarificatory circulars. The provisions of Income Tax Act 2025 have been rationalized to provide for exemption of disability pension, in cases where the individual has been invalided out of Armed Forces service on account of a bodily disability attributable to, or aggravated by, such service. The exemption will also be available to paramilitary personnel.

(Effective from 1st day of April 2026)

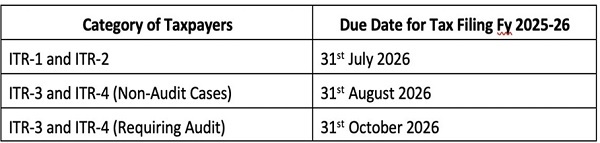

9. Rationalizing Due Dates for Filing of Return of Income: The section 263 of the Income Tax Act 2025 makes the provisions for filing of Income Tax Return by taxpayers. The section 263 deals with the comprehensive framework that lays down class of persons who are required to file a return, the due dates, and the different types of returns that may be furnished. It covers the original return, belated return, revised return and the updated return. The due date for filing of return has been extended from 31st July to 31st August, for assessee having income from profits and gains of business or profession whose accounts are not required to be audited. The summarized position of due dates as per amended provisions is as under:

(Effective from 1st day of March 2026, for AY 2026-27, PY 2025-26)

10. Extending the Period of Filing Revised Return: The section 263(5) of the Income Tax Act 2025 allows a person who has already furnished a return, to file a revised return, if any omission or wrong statement is discovered in the original or belated return, within nine months from the end of the relevant tax year or before completion of assessment, whichever is earlier. It has been amended to increase the prescribed time limit for filing the revised return to twelve months from the end of the relevant tax year. Also, a fee has been levied, for revised returns which are filed beyond nine months from the end of relevant tax year. The similar amendments have also been made in section 139(5) of Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

11. Scope of Filing of Updated Return in the case of Reduction of Losses: The section 263(6) of the Income Tax Act 2025 allows a taxpayer, whether or not a return was furnished earlier, to file an updated return within 48 months from the end of the financial year succeeding the relevant tax year. The said section further imposes certain restrictions on updating the return of Income. e.g., updated return cannot be a return of loss, cannot reduce tax liability, and cannot increase a refund. Filing an updated return requires payment of additional income-tax as prescribed. It has been amended to allow filing of updated return in such cases where taxpayer reduces the amount of loss in comparison to the amount of loss claimed in the return of loss furnished within the due date. The similar amendments have also been made in Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

12. Allowing the Filing of Updated Return after Issuance of Notice of Reassessment: The section 263(6) of the Income Tax Act 2025 allows a taxpayer, regardless of whether the original return is filed, to file an updated return within 48 months from the end of the financial year succeeding the relevant tax year. Filing an updated return requires payment of additional income-tax amounting to 25%, 50%, 60% and 70% of the aggregate of tax and interest payable, for filing the updated return in first, second, third and fourth year, respectively from the end of the financial year succeeding the relevant tax year. It has been amended to provide that an updated return may be furnished by a person for the relevant tax year in pursuance of a notice under section 280 within such period as specified in the said notice. In such cases, the additional income-tax payable shall be increased by a further sum of 10 % of aggregate of tax and interest payable. The similar amendments have also been made in Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

13. Foreign Assets of Small Taxpayers – Disclosure Scheme, 2026 (FAST-DS 2026): The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015, was enacted to address the issue of undisclosed foreign income and assets held by resident taxpayers. It has been observed that non-compliance is particularly prevalent in cases involving legacy or inadvertent non-disclosures for small taxpayers. It has been amended to introduce a time-bound scheme for declaration of foreign assets and foreign-sourced income, with payment of tax or fee based on the nature and source of acquisition and grant of limited immunity from penalty and prosecution under the Black Money Act in respect of matters covered by the declaration.

(Effective from the date to be notified)

14. Relaxation of Conditions for Prosecution under the Black Money Act: The Black Money Act, provides for penal and prosecution measures in cases of wilful non-disclosure of foreign income and assets by residents. In order to provide relief in cases of minor and inadvertent non-disclosures, sections 49 and 50 of the Act, have been amended to provide that these provisions shall not apply in respect of foreign assets, other than immovable property, where the aggregate value does not exceed twenty lakh rupees.

(Effective from 1st day of October 2024)

15. Rationalization of Penalties into Fee: The penalties for delays under section 446, 447 and 454 of the Income Tax Act 2025 have been converted into mandatory fee as fee reduces litigation for technical faults.

– Penalty under section 446 for failure to get accounts audited has been converted to a Graded fee of Rs. 75,000 and1,50,000 depending upon the period of delay.

– Penalty under section 447for failure to furnish report under section 172 has been converted to a Graded fee of Rs. 50,000 and 1,00,000 depending upon period of delay.

– Penalty under section 454(1)for failure to furnish statement of financial transaction or reportable account has been converted to a fee.

– For penalty under section 454(2), an upper limit of 1,00,000/- has been provided.

(Effective from 1st day of April 2026)

16. Exemption to a Foreign Company on any income arising in India by way of Procuring Data Centre Services from a Specified Data Centre: The existing section 11 of the Income Tax Act 2025 read with Schedule IV specifies the eligible income, which shall not be included in the total income of the eligible non-residents, foreign companies and other such persons. The Schedule IV has been amended to provide exemption to a foreign company, on any income accruing or arising in India or deemed to accrue or arise in India by way of procuring data centre services from a specified data centre, for a period up to tax year ending on 31st March, 2047. One of the conditions for exemption is that where services are provided to India users by the foreign company, it shall be routed through an Indian reseller entity. The “specified data centre” means a data centre which is set up under an approved scheme and is notified in this behalf by the Central Government in the Ministry of Electronics and Information Technology, and is owned and operated by an Indian company.

(Effective from 1st day of April 2026)

17. Allowing Deduction for expenditure on Prospecting of Critical Minerals: The section 51 of the Income Tax Act 2025 provides for tax deductibility of expenses incurred by an Indian company or resident taxpayers (other than companies) engaged in any operations relating to prospecting or extraction or production of the minerals. It allows deduction, on deferred basis (over a span of 10 years), in respect of expenses incurred wholly and exclusively on operations relating to prospecting or on the development of mine or other natural deposit. It has been amended to expand the list of minerals in Schedule XII of the Act, thereby making expenditure on prospecting and exploring of such critical minerals also eligible for deduction.

(Effective from 1st day of April 2026)

18. Exemption to a Foreign Company on Income arising on account of Providing Capital Equipment etc. to an Electronic Goods Manufacturer Located in a Custom Bonded Area: The existing section 11 of the Income Tax Act 2025 read with Schedule IV specifies the eligible income, which shall not be included in the total income of the eligible non-residents, foreign companies and other such persons. The Schedule IV has been amended to provide exemption to a foreign company for a period up to the tax year 2030-2031, on any income arising on account of providing capital goods, equipment or tooling to a contract manufacturer, being a company resident in India, who is located in a custom bonded area, and produces electronic goods on behalf of such foreign company for a consideration.

(Effective from 1st day of April 2026)

19. Exclusion of Specified Business of Non-Residents which are under Presumptive Taxation from the Applicability of Minimum Alternate Tax: Certain foreign companies are excluded from the application of Minimum Alternate Tax (MAT) under the present provisions. The income of non-residents derived from certain business who opt for presumptive rate of taxation under section 61 of the Income Tax Act 2025, are also excluded. It has been amended to provide that income of non-residents who opt for presumptive rate of taxation, for two other specified businesses (business of operation of cruise ships and the business of providing services or technology for the setting up an electronics manufacturing facility in India to a resident company) shall also be excluded from the applicability of MAT.

(Effective from 1st day of April 2026)

20. Exemption to Non-Residents for Rendering Services under a Notified Scheme in India: The existing section 11 of the Income Tax Act 2025 read with Schedule IV specifies the eligible income, which shall not be included in the total income of the eligible non-residents, foreign companies and other such persons. The Schedule IV has been amended to provide exemption to a non-resident individual visiting India for rendering certain services in connection with any notified Scheme of the Central Government, on any income which accrues or arises outside India, and is not deemed to accrue or arise in India, for five consecutive tax years.

(Effective from 1st day of April 2026)

21. Extension of Period of Deduction for units in IFSC and Rationalization of Tax Rate: The section 147 of the Income Tax Act 2025 provides for deduction of 100% on certain incomes to the units of IFSC and OBUs. This is available for 10 consecutive years out of 15 years for units in IFSC and 10 consecutive years for OBUs. It has been amended to increase the period of deduction to 20 consecutive years out of 25 years for units in IFSC and 20 consecutive years for OBUs. It has also been provided that the business income of these units from IFSC after the expiry of period of deduction will be taxed at rate of 15%.

(Effective from 1st day of April 2026)

22. Rationalization of Minimum Alternate Tax Provisions: The existing section 206 of the Income Tax Act 2025 provide for Minimum Alternate Tax (MAT) which is applicable for companies for the old tax regime. This tax is charged on the Book profit of the assessee at the rate of 15% for corporates. In case the MAT is higher than the income-tax payable on the company total income computed under normal tax provisions, the assessee pays MAT. When a company pays MAT when it is higher than regular tax, the excess amount paid is allowed as a tax credit. This credit can be carried forward up to 15 years and set off in future years where the company’s regular tax liability exceeds the MAT liability.

It has been amended to provide that the tax paid under provisions of MAT be made as final tax in the old regime and no new MAT credit may be allowed. However, the tax rate of MAT has been reduced to 14% of book profit from the existing 15%. Further, set-off of MAT credit shall be allowed only in the new tax regime for domestic companies to the extent of 25% of the tax liability. In the case of foreign companies, set off shall be allowed to the extent of the difference between the tax on the total income and the minimum alternate tax, for the tax year in which normal tax is more than MAT.

(Effective from 1st day of April 2026)

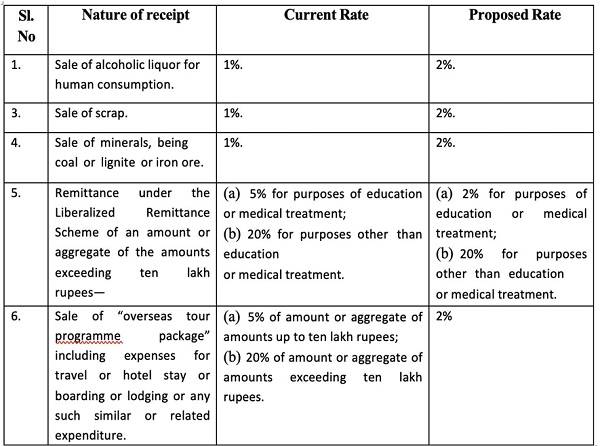

23. Rationalization of Tax Collected at Source (TCS) Rates: The section 394(1) of the Income Tax Act 2025 provides multiple rates for collection of tax at source, which have been rationalized by providing uniform rates to the extent possible, detailed as under: –

(Effective from 1st day of April 2026)

24. Provisions relating to Income from House Property and Permanent Account Number: The section 21(5) of the Income-tax Act 2025 has been amended to align it with the corresponding provision of Income-tax Act, 1961 so as to provide that annual value of property held as stock-in-trade to be taken as nil up to two years from the end of the financial year in which certificate of completion of construction is obtained from the competent authority. The section 22(2) has been amended to provide that aggregate amount of deduction for interest on borrowed capital shall be inclusive of prior- period interest payable. The section 262(10)(c) of the Act has been amended to enable Central Board of Direct Taxes (CBDT) to make rules for quoting of Permanent Account Number in documents related to such transactions which do not relate to business or profession.

(Effective from 1st day of April 2026)

25. Guidelines to be Binding on Income Tax Authorities and Person Liable to Deduct or Collect Income Tax: The section 400(2) the Income Tax Act 2025 provides that the Board with the previous approval of Central Government, may issue guidelines to remove any difficulties arising in giving effect to provisions of TDS/TCS chapter and such guidelines shall be laid before each House of Parliament. It has been amended to provide that any guidelines issued to remove difficulties in giving effect to provisions of TDS/TCS chapter shall be binding on income-tax authorities and on the person liable to deduct or collect Income-tax.

(Effective from 1st day of April 2026)

26. Non-allowability of Interest as a Deduction against Dividend Income: Dividend income and income from units of mutual funds constitute passive investment receipts taxable under the head “Income from other sources”. The section 93 of the Income Tax Act 2025 provides for allowing certain deductions against such income, i.e., interest expenditure incurred for earning such income, subject to a ceiling of twenty per cent of the gross dividend or income from units of mutual funds. It has been amended to provide that no deduction shall be allowed in respect of any interest expenditure incurred for earning dividend income or income from units of mutual funds.

(Effective from 1st day of April 2026)

27. Rationalisation of Schedule XI of the Income Tax Act 2025 relating to Provident Funds: In view of the evolution of the provident fund regulatory regime and the introduction of an absolute monetary cap on employer contributions under section 17(1)(h) of the Income Tax Act 2025, it has been amended to rationalise and align the income tax provisions of Schedule XI of the Act, governing recognised provident funds.

– The provisions of paragraph 4(c) of Part A of Schedule XI of the Act restrict employer contributions by reference to parity with employee contributions and mandates annual crediting of such contributions. It has been omitted, as a unified monetary ceiling of Rs 7.5 lakh on aggregate employer contributions.

– The provisions of paragraph 4(f) of Part A of Schedule XI govern eligibility for recognition of provident funds with reference to exemption from the EPF Scheme. It has been amended to provide that only provident funds which have obtained exemption under section 17 of the EPF Act may apply for recognition under the Income-tax

– The provisions of paragraph 5(4) of Part A of Schedule XI permit discretionary relaxation of employer–employee contribution parity based on a salary threshold of Rs 500 or contingent bonus structures. It has been omitted, as a unified monetary ceiling of Rs 7.5 lakh on aggregate employer contributions.

– The provisions of paragraph 6(a) of Part A of Schedule XI deem employer contributions in excess of twelve per cent of salary as income of the employee. It has been omitted as this percentage-based restriction overlaps with the unified monetary ceiling of Rs 7.5 lakh on aggregate employer contribution.

– The provisions of paragraph 1(d) of Part C of Schedule XI prescribe differentiated limits for employees who are also shareholders of the employer company. It has been omitted, since such a distinction is not recognised under the EPF Act or the EPF Scheme and overlaps with the unified monetary ceiling of Rs 7.5 lakh on aggregate employer contribution.

– The provisions of paragraph 1(e) of Part C of Schedule XI restrict investment of provident fund monies in Government securities to fifty per cent. This ceiling is inconsistent with the current investment norms prescribed by the Ministry of Labour and Employment and the Employees’ Provident Fund Organisation, which permit higher exposure. It has been amended to remove the rigid statutory cap, while retaining regulatory oversight through subordinate legislation under the EPF framework.

(Effective from 1st day of April 2026)

28. Rationalizingthe Due Date to credit Employee Contribution by the Employer to claim such Contribution as Deduction: The existing section 29(1)(e) of Income Tax Act 2025 allows for deduction of any amount of contribution received by the assessee being an employer, from an employee, if such amount is credited by the assessee to the account of the employee in the relevant fund or funds by the due date. The ‘due date’ means the date by which the assessee is required as an employer to credit employee contribution to the account of an employee in the relevant fund. It has been amended to provide that the due date for crediting the employee contribution shall be due date of filing of return of income under section 263(1) of the

(Effective from 1st day of April 2026)

Exemption on Interest Income under the Motor Vehicles Act: The exiting section 11 of Income Tax Act 2025 provides for the exemption of income of persons included in Schedule III subject to the fulfilment of conditions specified therein. The said Schedule has been amended to provide exemption to an individual or his legal heir, on any income in the nature of interest under the Motor Vehicles Act 1988.

(Effective from 1st day of April 2026)

29. No TDS in respect of Interest on Compensation Amount awarded by MotorAccidents Claims Tribunal to an Individual: As per section 393(4) of Income Tax Act 2025, tax is not required to be deducted in respect of interest on the compensation amount awarded by the Motor Accidents Claims Tribunal, if the amount or the aggregate of the amounts of such income does not exceed ₹ 50,000 during the tax year. It has been amended to provide that no tax shall be deducted at source in respect of interest on the compensation amount awarded by the Motor Accidents Claims Tribunal to an individual.

(Effective from 1st day of April 2026)

30. Enabling Electronic Verification and Issuance of Certificate for Deduction of TDS/ TCS at Nil or Lower Rate: Section 395 of Income Tax Act 2025 provides for issuance of certificate, for deduction of tax at source (TDS) and tax collection at source (TCS) at nil or lower rate. The amended provisions allow an option to the payee, to file the application, electronically before the prescribed income-tax authority, which may issue the certificate subject to fulfilment of conditions as may be prescribed, or reject the application if prescribed conditions are not fulfilled or the application is incomplete.

(Effective from 1st day of April 2026)

31. Allowing Deduction to Non-life Insurance Business when TDS, not deducted earlier is Paid Later: The existing section 35(b)(i) and (ii) of Income Tax Act 2025 provides that any sum, interest, etc. payable on which tax is deductible at source but has not been deducted or deducted but not paid within the due date specified in section 263(1), then the amount as mentioned in the respective sections shall not be allowed as deduction. The provisions have been rationalized to provide that the amount disallowed, shall be allowed as deduction in the tax year in which tax has been deducted and paid as per the provisions of the said section.

(Effective from 1st day of April 2026)

32. Exemption of Income on Compulsory Acquisition of any Land under the RFCTLARR Act: The section 96 of the Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement Act, 2013 (RFCTLARR Act), provides that income tax shall not be levied on any award or agreement made (except those under section 46) under the said Act. CBDT vide Circular No.36/2016 had clarified that compensation received in respect of such award or agreement, shall not be taxable even if there are no specific provisions of exemption for such compensation in the Income Tax Act. The provisions of Income Tax Act 2025 have been rationalized to exempt any income in respect of any such award or agreement made on account of compulsory acquisition of any land, carried out on or after the 1st April, 2026.

(Effective from 1st day of April 2026)

33. Rationalization of Prosecution Proceedings: The provisions of chapter XXII of the Income Tax Act 2025, imposes criminal liability on assessee and prescribes imprisonment including rigorous imprisonment which span from three months to seven years for various offences including falsification of books of accounts, failure to credit TDS/TCS deducted, tendering false statement, wilful attempt to evade tax, failure to furnish return within due time, abatement of false return, removal/ concealment/ transfer of property to evade recovery of tax, failure to follow certain directions of AO, etc. The section 473 to 485 & 494 have been amended in light of continued exercise of decriminalization and to make punishment for the offences, proportionate to the crimes.

-

- The nature of punishment has been changed from rigorous imprisonment to simple imprisonment wherever prescribed in these sections.

- Maximum punishment has been limited to 2 years from its current 7 year and for the subsequent offences, it is reduced to 3 years from its current 7 years.

- Wherever punishment of offences is prescribed based on certain grading of amount of tax evaded, new grading of offences/ corresponding punishment has been prescribed.

- For amount of tax evaded does not exceeds ten lakh rupees, punishment of only fine has been prescribed.

- Imposition of fine has been introduced in lieu of or in addition of imprisonment.

- Certain offences have been fully decriminalized.

The similar amendments have also been made in the Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

34. Rationalizing the Period of Block in case of Other Persons: The section 295 of the Income Tax Act 2025 provides, that where Assessing officer is satisfied that any undisclosed income belongs to or pertains to or relates to any ‘other person’, other than the person ‘specified person’ with respect to whom search was initiated, then, any material or information relating to the aforesaid undisclosed income will be handed over to the Assessing Officer having jurisdiction over such other person, who shall proceed against such other person. The existing provisions of Block assessment provides that, the block period is same for the specified person or other person. It has been amended to limit the period of block in case of third party to relevant years of his undisclosed income.

(Effective from 1st day of April 2026)

35. Referencing the Time Limit to complete Block Assessment to the Initiation of Search or Requisition: The section 296 of the Income Tax Act 2025 provides that an assessment or reassessment for block assessment must be completed within 12 months from the end of the quarter in which the last search authorization was executed or requisition was made. It has been amended to provide the date initiation of search as the reference point to decide the date of limitation, and the period of eighteen months to complete block assessment.

(Effective from 1st day of April 2026)

36. Imposition of Penalty for Under-reporting or Misreporting of Income within Assessment Order: Under the existing provisions, first an assessment order is passed and based on the findings or additions made in it and subject to the status of appellate proceedings, penalty is initiated. The separate penalty proceedings are initiated by giving a show cause notice and a separate penalty order is passed after giving due opportunity to the assessee. It leads to multiplicity of proceedings, and uncertainty for taxpayer regarding the status of imposition of penalty.

It has been amended to provide that, penalty for under- reporting of income shall be imposed within the Assessment Order. It has also been provided for charging of interest, only after passing of the order by CIT(A) or ITAT (for appeal against DRP orders), as case may be. The similar amendments have also been made in Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

37. Increase in Maximum Amount of Penalty in section 466 of the Act: The section 254 of the Income Tax Act 2025 provides the power to the income tax authorities to collect information from the premises where business or profession is carried out. Further, section 466 provides for imposition of maximum penalty amounting to Rs. 1000/- for failure to comply with this provision. It has been amended to enhance the maximum amount of penalty to Rs. 25,000/-.

(Effective from 1st day of April 2026)

38. Rationalization of Tax Rate under section 195 and Penalty under section 443 in respect of Certain Income: The section 195 of the Income Tax Act 2025 provides for tax on income referred to in section 102 to 106, i.e., income on account of, unexplained credits, unexplained investment, unexplained asset, unexplained expenditure and amount borrowed or repaid through negotiable instrument, hundi, etc. It provides that where total income of an assessee includes any such income, the income tax calculated on such income will be charged at the rate of 60%. Further, section 443 of the Act provides penalty amounting to 10% of the tax payable. It has been amended to reduce the tax rate from 60% to 30% and also omit the penalty under section 443 and subsume this penalty under section 439(11) of the Act.

(Effective from 1st day of April 2026)

39. Expanding the scope of Immunity from Imposition of Penalty or Prosecution under section 440 of the Act: The section 440 of the Income Tax Act 2025 provides for granting of immunity (in cases of under reporting of income) by the Assessing Officer from imposition of penalty or prosecution, if (a) the tax and interest payable as per Assessment order, has been paid within the period specified in notice of demand, and (b) no appeal against the such assessment order has been filed. It has been amended to extend the scope of immunity to such cases where penalty is initiated for under-reporting of income in consequence of misreporting. The similar amendments have also been made in Income Tax Act 1961.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of March 2026 for Act 1961)

40. Deductions in respect of Dividends Received and Distributed by Certain Cooperative Societies: The section 149(2)(d) of the Income Tax Act 2025 provides for deduction on the income of a cooperative society that is received as interest or dividend from any other co-operative society, in the old tax regime. The dividends received by a cooperative society from a company are taxed in the hands of the cooperative society. It has been amended to allow deduction on dividends received by cooperative societies from other cooperative societies, to the extent such dividends are distributed to its members, in the new tax regime. It has also been amended to allow deduction for dividends received by notified federal cooperatives from companies for 3 years, i.e., till tax year 2028-29 under both the old and new tax regimes, for dividends arising out of investments made by the federal cooperative till 31.01.2026 and which are further distributed by it to its members.

(Effective from 1st day of April 2026)

41. Widening scope of Deduction under section 149 by including Ancillary Activities of Cattle Feed and Cotton Seeds: The section 149(2)(b) of the Income Tax Act 2025 provides for deduction of whole of the amount of profits and gains of business in the case of a co-operative society, being a primary society engaged in supplying milk, oilseeds, fruits, or vegetables raised or grown by its members to a federal co-operative society, engaged in the same business or to the Government or a local authority; or to a Government company or a corporation engaged in the same business. It has been amended to include activities such as supplying of cattle feed and cotton seeds, within the ambit of this section.

(Effective from 1st day of April 2026)

42. Inclusion of Cooperatives registered under Multi-State Cooperative Societies Act, 2002 in the Definition of Cooperative Society’: As per provisions of section 2(32) of the Income Tax Act 2025, a ‘co-operative society’ is defined as a co-operative society registered under the Cooperative Societies Act, 1912, or under any other law in force in any State or Union territory for the registration of co-operative societies. It has been amended to include the Co-operative societies which are registered under the “Multi-State Cooperative Societies Act, 2002,” within the definition of co-operative society under the Act.

(Effective from 1st day of April 2026)

43. Amendment of section 169 of the Income-tax Act, 2025 relating to Providing Effect to Advance Pricing Agreements: The section 168(1) of the Income Tax Act 2025 allows filing of a modified return of income only by the person who has entered into advance pricing agreement (APA) with the Board. The provisions do not allow for modifying the return of income or filing of return of income by the associated enterprise whose income and tax liability is correspondingly modified consequent to the APA. It has been amended to provide that where an income is modified as a result of advance pricing agreement entered into with any person then, such person shall, or any other person being an associated enterprise, may, furnish a return or a modified return, within a period of three months from the end of the month in which the said agreement was entered into, in respect of tax years covered by such agreement, where such agreement is entered on or after 1st April, 2026, in respect of tax year beginning from 1st April, 2026.

(Effective from 1st day of April 2026)

44. Rationalization of Certain Terms for Treasury Centers in IFSC: The section 2(40) of the Income Tax Act 2025 provides the definition of dividend. The sub clause (v) provides that dividend does not include any advance or loan between two group entities, where, one of the group entities is a “Finance company” or a “Finance unit”, and the parent entity or principal entity of such group is listed on stock exchange in a country or territory outside India other than the country or territory outside India as may be specified by the Board. It has been amended to provide that the other group entity to the transaction shall also be located in a country or territory outside India which shall be a notified jurisdiction. The terms ‘group entity’ and ‘parent entity or principal entity’ have also been defined.

(Effective from 1st day of April 2026)

45. Clarification regarding Jurisdiction to Issue Notice under 148 Where Income has Escaped Assessment and for Carrying out Pre-assessment Procedure under 148A: The Income Tax Act 1961 provides a two-step procedure for carrying out reassessment under section 147. This first step starts with a notice under section 148A which enables the Assessing Officer to carry out enquiries so as to determine whether the case is fit for issuance of notice under section 148. A reasoned order is passed under section 148A by the Assessing Officer. The second step i.e., with the issue of notice under section 148, the case gets transferred to the National Faceless Assessment Centre (NaFAC) for carrying out the assessment in a faceless manner as per section 144B.

It has been amended to clarify that notwithstanding anything contained in any judgment, order or decree of court, the Assessing Officer for the purposes of section 148 and section 148A shall mean and shall always be deemed to have meant Assessing Officer other than the National Faceless Assessment Centre or any of its assessment units. Suitable amendment is also carried out in the Income-tax Act 2025.

(Effective from 1st day of April 2026 for Act 2025, and 1st day of April 2021 for Act 1961)

46. Assessments not to be Invalid on Ground of any Mistake, Defect or Omission on account of Computer Generated DIN, if such assessment is Referenced by the DIN in Any Manner: Section 292B of the Income-tax Act 1961 states that no return of income, assessment, notice, summons or other proceeding in pursuance of any of the provisions of this Act shall be invalid or shall be deemed to be invalid merely by reason of any mistake, defect or omission in such return of income, assessment, notice, summons or other proceeding if such return of income, assessment, notice, summons or other proceeding is in substance and effect in conformity with or according to the intent and purpose of this Act.

CBDT Circular 19 of 2019 dated 14th August 2019 provided for quoting of a computer-generated document identification number (DIN), on inter-alia, assessment orders. The section 292B has been amended to provide that notwithstanding anything contained in any judgment, order or decree of court, no assessment in pursuance of any of the provisions of Income Tax Act 1961 shall be invalid or shall be deemed to have been invalid on the ground of any mistake, defect or omission in respect of quoting of a computer generated Document Identification Number, if such assessment order are referenced by such number in any manner. Suitable amendments have also been carried out in the Income-tax Act 2025.

(Effective from 1st day of April 2026 for Act 2025, 1st day of October 2019 for Act 1961)

47. Clarifying Time Limit for Completion of Assessment under section 144C: Section 144C provides for a special procedure where assessment is made in cases where the eligible assessee is a person in whose case variations arise on account of order of a transfer pricing officer or where the person is a non-resident. Under this section, the Assessing Officer is required to forward a draft of the proposed order of assessment (draft order) to the eligible assessee.

The eligible assessee can accept the variation proposed in the draft order or file objections before the Dispute Resolution Panel (DRP). Where variations in the draft order are accepted, the Assessing Officer is required to complete the assessment on basis of the draft order. The period for completing the assessment in this case provided in section 144C, is one month from the end of the month in which the acceptance is received or the period of 30 days of filing objections before DRP expire. Where the eligible assessee files objection to the DRP, the DRP is required to pass directions and time limit for passing these directions is nine months from the end of the month in which draft order is forwarded to the eligible assessee. The period for completing the assessment in this case is one month from the end of month in which such directions are received.

Section 153 provides for time limit for completion of assessment, reassessment and re-computation. Section 153B provide time limit for completion of assessment in search cases. The section 153 and section 153B have been amended to provide that time lines in these sections govern the draft order stage and the timelines provided in section 144C operate for finalization of assessments. Suitable amendments have also been carried out in the Income-tax Act 2025.

(Effective from 1st day of April 2026 for Act 2025, 1st day of April 2009 for Act 1961)

48. Manner of Computation of 60 days for Passing the Order by the Transfer Pricing Officer (TPO): The section 92CA of the Income-tax Act, 1961 deals with the case where assessee, has entered into an international transaction or specified domestic transaction in any previous year, and the Assessing Officer (AO) may refer the computation of the arm’s length price in relation to the said international transaction or specified domestic transaction under section 92C to the TPO. The TPO is required to pass an order before 60 days prior to the date on which period of limitation under section 153/ 153B for making the order of assessment expires. The section 92CA has been amended to provide, as to how the period of sixty days is required to be computed. Suitable amendments have also been carried out in the Income-tax Act 2025.

(Effective from 1st day of April 2026 for Act 2025, 1st day of June 2007 for Act 1961)

49. Amendments in Chapter XIII-G for giving effect to Extension of Tonnage Tax Scheme to Inland Vessels: Chapter XIII-G of the Income-tax Act, 1961 provides for special provisions relating to income of shipping companies. Vide Finance Act, 2025, benefit of tonnage tax scheme under the said Chapter was extended to Inland vessels registered under Inland Vessels Act, 2021 to promote the inland water transportation. The relevant provisions of sections 227, 228, 232 and 235 Income Tax Act 2025 have been amended to provide references for Inland Vessels and for applicability of tonnage tax scheme.

(Effective from 1st day of April 2026)

50. Penalty provision for Non-furnishing of Statement or Furnishing Inaccurate Information in a Statement on Transaction of Crypto-asset: As per Section 509 of the Income Tax Act 2025, prescribed reporting entities, such as crypto exchanges and brokers, has the obligation to furnish information in respect of transactions in a crypto asset. The section 446 has been amended to provide for penalty of Rs. 200 per day for non- furnishing of statement and Rs. 50,000 for furnishing inaccurate particulars and failure to correct such inaccuracy.

(Effective from 1st day of April 2026)

51. Clarifying Repeal and Savings clause where Amount Allowed as Deduction Earlier is to be Treated as Income in a Later Year: The section 536(2)(h) of the Income Tax Act 2025 provides that where any deduction has been allowed or any amount has not been included in the total income under the repealed Income Tax Act 1961, subject to fulfilment of certain conditions, then on violations of such conditions, such amount will be deemed to be income in the tax year in which violation takes place. It has been amended to provide that where any sum has been allowed as deduction or has not been included in the total income under the repealed Income Tax Act, 1961, such sum will be deemed to be income under Income Tax Act 2025, even without violations of any conditions, if it was to be included in the total income under the provisions of Income Tax Act 1961 had it not been repealed.

(Effective from 1st day of April 2026)

52. Amendment in the provision relating to Merger of Non Profit Organisations (NPOs): The section 352(4) of the Income Tax Act 2025 provides that the specified person shall be liable to pay the tax on accreted income where it has merged with any other entity other than a registered non-profit organisation having the same or similar objects. It has been amended to insert a new Section 354A in the Income Tax Act to provide that where any registered non-profit organisation has merged with any other registered nonprofit organisation, the provisions of section 352 shall not apply if, (a) the other registered non-profit organisation has same or similar objects, and (b) the said merger fulfils such conditions as may be prescribed.

(Effective from 1st day of April 2026)

53. Amendment in the provisions relating to the Violations by a Registered NPO: The section 351 of the Income Tax Act 2025 specifies activities which constitute ‘specified violation’ by a registered non-profit organisation, and it includes violation on account of commercial activities by registered non-profit organisation carrying out advancement of any other object of general public utility. Such violation is also included in the ‘other violation’ under section 353, which may lead to cancellation of registration. It has been amended to remove the reference of such violation from section 351 of the Act.

(Effective from 1st day of April 2026)

54. Amendment of section 332(1)(f) to Remove Certain Funds from the Requirement of Registration: The section 332 of the Income Tax Act 2025 specifies the persons who may apply for registration as a registered non-profit organisation. It has been amended to provide that the persons referred to in Schedule VII (Table: Sl. No. 10) to (Table: Sl. No. 16), are not required to register themselves, to claim benefit of exemption.

(Effective from 1st day of April 2026)

55. Amendment in section 349 of the Income Tax Act, 2025 to provide for Filing of Belated Return by NPO: The section 349 of the Income Tax Act 2025 provides furnishing of return by a registered non-profit organisation within the time limit allowed under section 263(1)(c). It has been amended to enable furnishing of belated return by registered non-profit organization.

(Effective from 1st day of April 2026)

56. No TDS in respect of Interest Income Credited or Paid to any Cooperative Society engaged in Carrying on the Business of Banking (including a Cooperative Land Mortgage Bank): The section 393(4) of the Income Tax Act 2025 provides for the conditions where tax is not required to be deducted at source under corresponding provision of the Act. It has been amended to provide that deduction of tax at source shall not be made on interest income (other than interest on securities) credited or paid to any co-operative society engaged in carrying on the business of banking (including a co-operative land mortgage bank).

(Effective from 1st day of April 2026)

Annexure- A

Income Tax Rates for Tax Year 2026-27

Individual, HUF, Association of Persons, Body of Individuals or Artificial Juridical person

A. New Regime

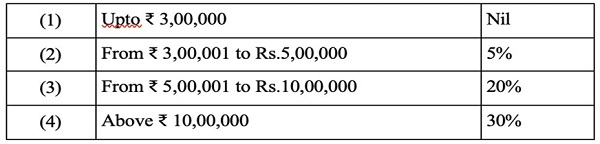

Under section 202, the rates applicable for determining the income-tax payable in respect of the total income of a person, being an individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person, are as under: –

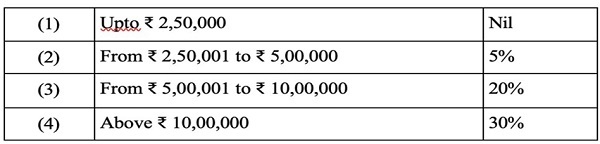

B. Old Regime

1. However, if such person exercises the option under 202(4) for old regime, the applicable rates are as under: –

2. For Senior Citizens (every individual, being a resident in India, who is of the age of sixty years or more but less than eighty years)

3. For Super Senior Citizens (every individual, being a resident in India, who is of the age of eighty years or more)

C. Surcharge and Health & Education Cess

The Surcharge and Health & Education Cess shall be additional as applicable.

******

Compiled by:- CMA Yash Paul Bhola, MBA, FCMA, Former Director (Finance), National Fertilizers Limited.

Disclaimer: The contents of this article are for informational purposes only. The user may refer to the relevant notification/ circular/ decisions by the respective authorities for specific interpretation and compliances related to a particular subject matter)

Author Bio