The consultation paper issued by the Securities and Exchange Board of India (SEBI) proposes the introduction of Gift Card/ Gift Prepaid Payment Instruments (Gift PPI) for investing in mutual funds, aiming to improve financial inclusion by onboarding new investors. Under the proposal, a purchaser can buy a Gift PPI through banking channels and transfer it to a recipient, who can redeem it for mutual fund subscriptions via an Asset Management Company (AMC). Existing SEBI and RBI regulations governing e-wallets and PPIs will apply, including limits, KYC requirements, and restrictions on incentives. Additional safeguards include funding only through bank transfer or UPI, mandatory ownership validation, adherence to ₹50,000 annual investment limits, and use of the full PPI value for subscription. The proposal also outlines refund mechanisms for unclaimed PPIs, distributor involvement options, and strict compliance with no third-party payment norms, while seeking public comments on key operational aspects.

Securities and Exchange Board of India

Consultation Paper on introduction of Gift Card/ Gift PPI (Prepaid Payment Instrument) for Mutual Funds

Mar 24, 2026 | Reports : Reports for Public Comments

1. Objective

1.1. The objective of this consultation paper is to solicit comments on the proposal to introduce Gift Card/ Gift PPI for subscription of mutual fund units. The proposal involves allowing purchaser of Gift Card/ Gift PPI to gift such instrument which can be utilized for subscription of mutual fund units by the recipient of Gift Card/ Gift PPI.

1.2. Gift Card/ Gift PPI is expected to improve financial inclusion through onboarding of new investors in the mutual fund space.

2. Background

2.1. SEBI has received a proposal from the Association of Mutual Funds in India (AMFI) to consider allowing Gift PPI as an instrument to invest in units of mutual fund.

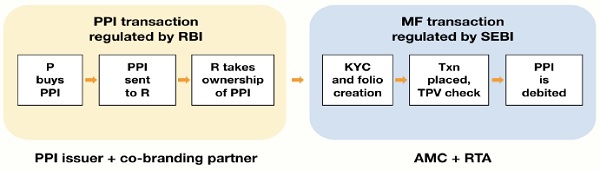

About the product: The purchaser of Gift PPI can gift the prepaid payment instrument, to a recipient of the Gift PPI, who can utilize the instrument for subscription of units of mutual fund. The flow of money in the Gift PPI from PPI issuer to purchaser of PPI to redeemer of Gift PPI shall be governed under the guidelines issued by the Reserve Bank of India (RBI). The subscription of units of mutual fund from Gift PPI shall be governed under the SEBI guidelines. As per the proposal by AMFI, following shall be the flow:

- The purchaser of Gift PPI receives the Gift Card either in physical form or online from PPI issuer on payment through banking channel.

- The Gift PPI is then shared with the intended beneficiary by the PPI purchaser.

- The person receiving the Gift PPI claims the ownership of the Gift PPI and use the same for subscription of units of mutual fund from the Asset Management Company’s (AMC) website.

2.2. SEBI guidelines: As per para 14.10 of SEBI Master Circular for Mutual Funds dated June 27, 2024, the following is inter alia stated on the use of e-wallets for investment in mutual funds:

2.2.1. Mutual funds (MFs)/Asset management Companies (AMCs) are allowed to enter into arrangement with issuers of PPIs for facilitating payment from e-wallets to mutual fund schemes.

2.2.2. MFs/AMCs shall ensure that extant regulations such as cut-off timings, time stamping, etc. are complied with for investment in MFs using e-wallets.

2.2.3. Redemption proceeds shall only be made in the bank account of the investor/ unit holder.

2.2.4. Total subscription through e-wallet and cash for an investor is restricted to INR 50,000 per MF per FY (financial year).

2.2.5. E-wallets shall not offer any incentives such as cashback, vouchers etc., directly or indirectly, for investing in MFs.

2.2.6. MFs/ AMCs shall ensure that only amounts loaded into e-wallet through cash or debit card or net banking can be used for subscription to MF schemes. Credit cards, cash back and promotional schemes cannot be used.

2.2.7. MFs/ AMCs shall also comply with the requirement of no third party payment norm for investment made using e-wallets.

2.3. RBI guidelines: PPI instruments are governed under RBI Master Directions on Prepaid Payment Instruments (PPIs). The relevant provisions are summarized as follows:

2.3.1. PPIs can be issued by banks and non-bank entities after necessary approval/ authorization from RBI under Payment and Settlement Systems Act, 2007.

2.3.2. PPI is defined as “Instruments that facilitate purchase of goods and services, financial services, remittance facilities, etc., against the value stored therein.”

2.3.3. Guidelines provides for safeguards against money laundering.

2.3.4. PPI can be loaded by cash, bank account, debit card, credit card etc. No interest is payable on PPI balances.

2.3.5. All PPIs issued in the country shall have a minimum validity period of one year from the date of last loading / reloading in the PPI. PPIs can also be issued with a longer validity.

2.3.6. PPI issuer shall caution the PPI holder at reasonable intervals, during the 45 days’ period prior to expiry of the validity period of the PPI;

2.3.7. Non-bank PPI issuer cannot transfer the outstanding balance to its Profit & Loss account for at least three years from the expiry date of PPI. In case the PPI holder approaches the PPI issuer for refund of such amount, at any time after the expiry date of PPI, then the same shall be paid to the PPI holder in a bank account.

Specific guidelines for Gift PPI under RBI Master Directions

2.3.8. Maximum value of each such prepaid payment gift instrument (Gift PPI) shall not exceed INR 10,000/-. Such instrument shall not be reloadable.

2.3.9. Cash-out or funds transfer shall not be permitted for such instrument. However, the funds may be transferred ‘back to source account’ (account from where Gift PPI was loaded) after receiving consent of the PPI holder.

2.3.10. KYC details of the purchaser of Gift PPI shall be maintained by the PPI issuer. Separate KYC shall not be required for customers who are issued such instrument against debit to their bank accounts and / or credit cards in India.

2.3.11. PPI issuer shall adopt a risk-based approach, duly approved by its Board, in deciding number of such instruments which can be issued to a customer, transaction limits, etc.

3. Additional safeguards proposed in consultation with AMFI

In addition to the abovementioned guidelines issued by RBI and SEBI, it is proposed to put in place following additional safeguards for implementation of Gift PPI as a mode for onboarding investors of mutual funds:

3.2. The PPI shall be funded only through electronic bank transfer or UPI from an Indian bank account.

3.3. PPIs offered by AMCs shall be redeemed for any of the mutual fund schemes managed by such AMC at the discretion of redeemer. In addition, considering that PPI redeemers could be first time investors who may be less familiar with mutual funds, the following options shall be provided to assist PPI redeemers in selecting a scheme:

3.3.1. The PPI purchaser may select a scheme for the PPI, however the same shall not be binding on the redeemer. Also, in this scenario, the PPI purchaser’s selection of a scheme will not constitute any investment advice or a recommendation. The mutual fund transaction executed by the PPI redeemer shall be processed under the direct plan.

3.3.2. The PPI redeemer may also avail the services of a distributor for selecting a scheme. In this scenario, the subscription will be processed under the regular plan.

Consultation No. 1:

Whether the proposal to allow PPI purchaser suggesting a scheme for PPI redeemer appropriate?

Consultation No. 2:

Whether the proposal to allow use of distributor services by PPI redeemer and processing the mutual fund subscription under regular plan appropriate?

3.4. Upon demand, the PPI issuer will provide to SEBI or to AMC, the PPI purchaser’s details, including source account details that was used to purchase the PPI.

3.5. Funds transfer: For each subscription of mutual fund units through Gift PPI, the PPI issuer shall send an electronic funds transfer from the PPI issuer’s escrow account to the relevant bank account for the use of funds by the mutual fund scheme.

3.6. Validity period: Each PPI shall have a validity period of one year from date of issuance. If the PPI is not claimed within one year, the PPI issuer shall refund the face value to the purchaser’s verified bank account. AMCs shall track unclaimed PPIs on a monthly basis and regularly notify PPI holder for any claim of Gift PPI.

Consultation No. 3:

Whether the proposal to refund the money after the end of validity period appropriate?

3.7. Third Party Validation (TPV) check: For each PPI redemption, the RTA will receive from the PPI issuer information identifying the registered owner of the PPI and check to see whether he or she is the same as the folio owner. If there is a match, the transaction will be allowed. Otherwise, the transaction will be rejected, and the PPI face value will be refunded to the issuer’s escrow account.

3.8. Compliance with no third-party payment norms: To comply with no third-party payment norms under para. 14.10.1(i) of Master Circular on Mutual Funds dated June 27, 2024, a Gift PPI must be legally owned by the redeemer before it can be used for mutual fund subscription. A PPI owned by any other person cannot be used to purchase a mutual fund. To ensure compliance, the Gift PPI redeemer must accept legal ownership of the Gift PPI, which is recorded by the PPI issuer, before it can be used for mutual fund subscription. When a subscription order is placed, the RTA receives from the PPI issuer information identifying the registered owner of the PPI and verifies that the registered owner is the same as the folio owner. If there is a match, the transaction is allowed, otherwise, the transaction is rejected.

3.9. INR 50,000 limit check: The RTAs, on behalf of AMCs will track how much each investor has invested per AMC per financial year through Gift PPI, e-wallets and cash. If the transaction resulting from a Gift PPI redemption crosses INR 50,000, the RTA will reject the transaction, and the PPI face value will be refunded to the issuer’s escrow account.

3.10. Full value of Gift PPI to be used: The full value of PPI shall be utilized by the PPI

redeemer for subscription to units of a mutual fund scheme. This will ensure that no funds remain unclaimed in the Gift PPI. The subscription value in the MF scheme of the PPI redeemer shall be equal to the value loaded in the PPI, subject to statutory levies on subscription to MF scheme, if any.

Consultation No. 4:

Whether the safeguards proposed for third party validation, compliance with third party payment norms and allowing only full value of Gift PPI to be utilized for subscription of mutual fund units appropriate?

3.11. Gift PPI Issuance/redemption fee: The issuer or co-branding partner charges with respect to PPI issuance shall be borne by the AMC.

3.12. Any distribution and marketing of proposed Gift PPIs shall have to be compliant with the SEBI guidelines for Mutual Funds including the advertisement code. Further, the AMCs shall refrain from using dark patterns on their website for subscription/ redemption of Gift PPI.

3.13. The important aspects of Gift PPI shall be clearly and suitably disclosed by MFs, inter-alia, including, validity of Gift PPI, grievance redressal, refund conditions, etc. The AMCs shall also be responsible for protection of interest of respective PPI buyers and shall facilitate grievance redressal along with PPI issuer.

Consultation No. 5:

Are the proposed safeguards adequate? If no, please specify what other measures can be made applicable.

Consultation No. 6:

Any other suggestions on the proposal may be provided with rationale

Public Comments on this Consultation Paper

1. Public comments are invited for the proposals as mentioned above. The comments/ suggestions should be submitted through the following link by April 14, 2026:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPublic Comments=yes

2. In case of any technical issue in submitting your comments through web based public comments form, you may contact the following through email with a subject

“Consultation Paper on introduction of Gift Card/ Gift PPI (Prepaid Payment Instrument) for Mutual Funds “:

a) Priyanka Mahapatra, General Manager (priyankam@sebi.gov.in)

b) Pranay Agrawal, Manager (pranaya@sebi.gov.in) Issued on: March 24, 2026

Issued on: March 24, 2026