Month: April 2026

1,943 articlesCorporate Law

Corporate Law

IBBI Study Highlights Need for Stronger MSME Insolvency Framework Due to Pre-Admission Settlements

Company Law

Company Law

Penalty Imposed for Failure to Conduct Board Meetings Under Companies Act

Corporate Law

Corporate Law

IRDAI Information and Cyber Security Guidelines, 2026

Income Tax

Income Tax

Section 69A Addition Deleted Due to Double Taxation of Recorded Sales

Income Tax

Income Tax

Statement of Financial Transactions (SFT) under Income-tax framework

Income Tax

Income Tax

Annual Information Statement (AIS): Section 285BB, Forms, Rule 114-I & Tutorials

Income Tax

Income Tax

Income Tax Audit under Section 44AB: Rules, Forms Penalties & Due Dates

Income Tax

Income Tax

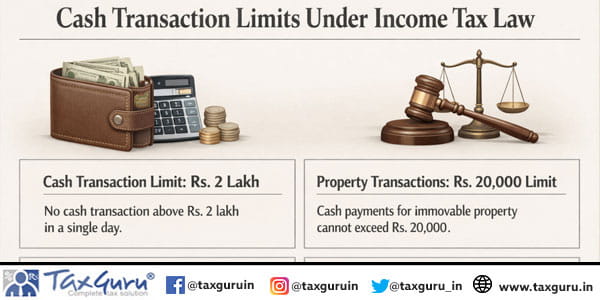

Cash Transaction Limits Under Income Tax Law

Income Tax

Income Tax

Income Tax Exemption to foreign funds investing in Indian infrastructure entities

Income Tax

Income Tax