Month: April 2026

1,943 articlesIncome Tax

Income Tax

Section 12AB & 80G Registration Cannot Be Denied for No Irrevocability Clause: ITAT Mumbai

CA, CS, CMA

CA, CS, CMA

9 Important Decisions taken in Meeting of ICSI Council dated 17-18 March 2026

Corporate Law

Corporate Law

CCI Orders Probe into Poultry Sector Over Restrictive Breeder Agreements Limiting Market Access

Income Tax

Income Tax

No Shares, No Dividend-ITAT Holds Mandatory Transfer to Govt Not Liable for DDT

Income Tax

Income Tax

Wrong Approval Authority = Entire Reassessment Void; ITAT Quashes 148 Proceedings

Income Tax

Income Tax

Technical Dismissal Upheld but ITAT Orders Fresh Review After 26AS Correction

Corporate Law

Corporate Law

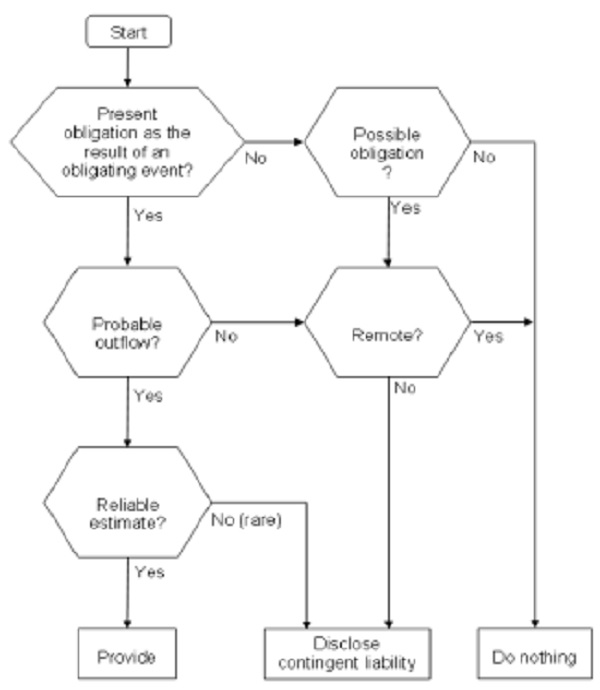

NFRA Issues Guidance to Strengthen Audit of Provisions and Contingent Liabilities

Income Tax

Income Tax

No Building Approval, No 12AB-Yet ITAT Grants Fresh Chance Due to Short Compliance Window

Income Tax

Income Tax

CBDT Notifies PAN CR-01 & CR-02 Forms to Simplify PAN Data Corrections

Income Tax

Income Tax