Month: January 2026

2,391 articlesIncome Tax

Income Tax

ITAT Delhi Quashed Reassessment For Wrong Assumption of Facts

Finance

Finance

IFSCA Classified Oilfield Equipment Leasing as Financial Product

Company Law

Company Law

Mandatory Valuation by Registered Valuer for Preferential Issue of Shares

Income Tax

Income Tax

Unexplained Cash Credits (Section 68): How to defend?

Goods and Services Tax

Goods and Services Tax

GST Advisory on Filing Opt-In Declaration for Specified Premises, 2025

Company Law

Company Law

MCA to set up 3 new Regional Directorates & 6 Registrar of Companies

Company Law

Company Law

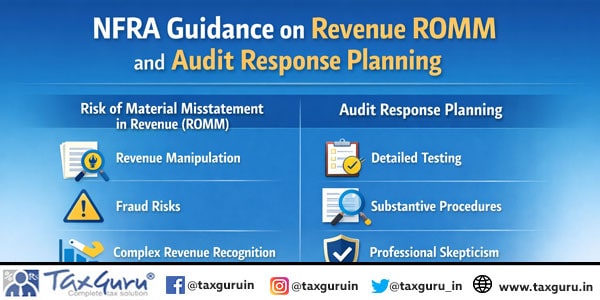

NFRA Guidance on Revenue ROMM and Audit Response Planning

Excise Duty

Excise Duty

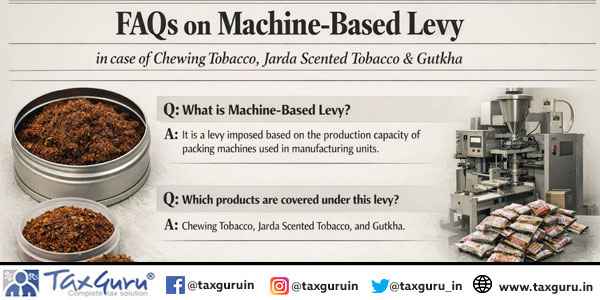

FAQs on Machine-Based levy in case of Chewing Tobacco, Jarda Scented Tobacco & Gutkha

Custom Duty

Custom Duty

Custom Advance Ruling Declined as Classification Issue Already Settled by Court

Custom Duty

Custom Duty