Month: January 2026

2,391 articlesIncome Tax

Income Tax

Section 50C Adjustment Barred at Return Processing Stage: ITAT Delhi

Income Tax

Income Tax

Inter-Charity Donations is Valid Application of Income: ITAT Delhi

Income Tax

Income Tax

No Double Taxation of Same Bank Credits, Matter Sent for Verification

Income Tax

Income Tax

Failure to Furnish Details Not Final: ITAT Grants Fresh Opportunity

Income Tax

Income Tax

Section 153C Bar After April 2021: Bulk Assessments Quashed by ITAT

Corporate Law

Corporate Law

Appeal Does Not Abate If Estate Is Sufficiently Represented: SC

Corporate Law

Corporate Law

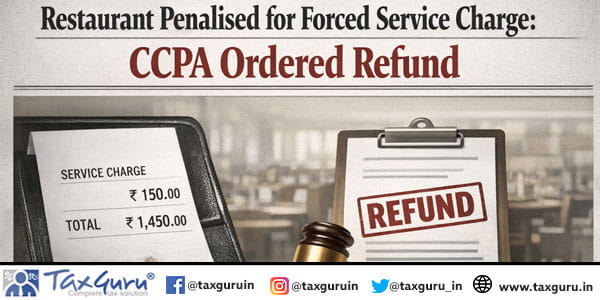

Forced Service Charge by Restaurant & GST Thereon is Unfair Trade Practice: CCPA Delhi

Corporate Law

Corporate Law

Restaurant Penalised for Forced Service Charge: CCPA Ordered Refund

Corporate Law

Corporate Law

Hiding Pending Criminal Cases Bars Government Jobs: SC

Custom Duty

Custom Duty