Month: June 2025

1,781 articlesGoods and Services Tax

Goods and Services Tax

Silver Trade Under GST: Barter, RCM & E-Way Bill – AAR Ruling

Goods and Services Tax

Goods and Services Tax

Tamil Nadu AAR Rejects GST ITC Ruling Request Due to Ongoing DGGI Investigation

Income Tax

Income Tax

CPC Must Grant Full TDS Credit as Reflected in Form 26AS; Cannot Reduce Claim: ITAT Jodhpur

Goods and Services Tax

Goods and Services Tax

GST on Corpus Funds for Apartment Maintenance

Custom Duty

Custom Duty

Customs Broker not required to physically inspect premise of client to ensure their functioning

Custom Duty

Custom Duty

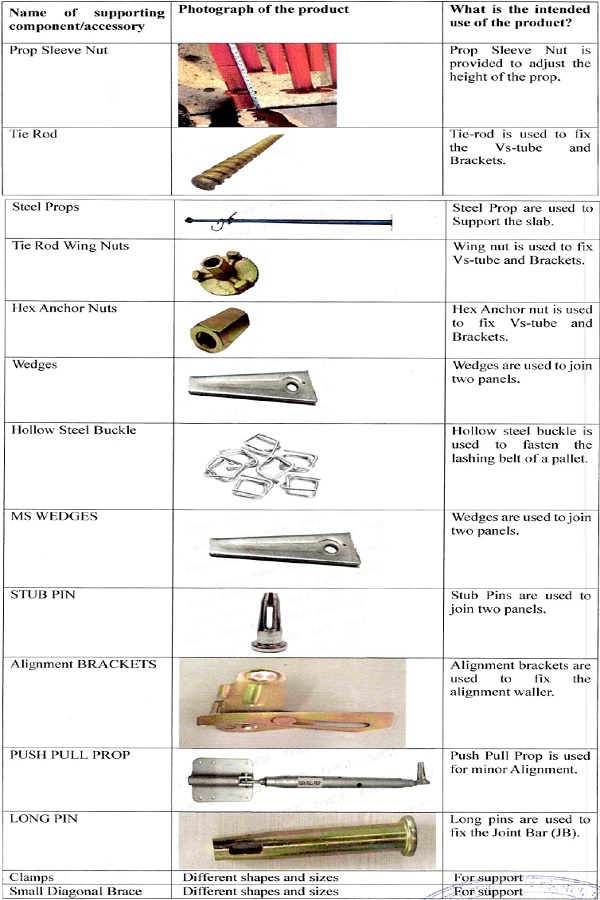

Imported Aluminium Formworks Classified as Temporary Structures Under CTI 7610: CAAR Delhi

Custom Duty

Custom Duty

CAAR Mumbai Classifies Mustek Mobile Computers as Data Processing Machines

Custom Duty

Custom Duty

Fuel Dispenser Display Boards Classifiable as Parts of Fuel Pumps Under CTI 84139190

Custom Duty

Custom Duty

Barcode/RFID Computers Classified Under 84713090: CAAR

Custom Duty

Custom Duty