Shalki Bansal

Charitable/religious trusts are the trusts which are formed with an objective of providing relief to poor, education, medical relief, preservation of environment/ monuments , advancement of objects of general public utility, religious purpose, etc. There taxation has always been a point of concern. The entire income of such trust (be it house property, capital gain or any other income) is taxed as per the provisions of section 11-13 of the Income Tax Act, 1961 rather than as per there relevant provisions . Here I have discussed the major areas related to taxation of income of such charitable/religious trusts.

Income of charitable/religious trust can be classified as follows:-

Page Contents

- I. Voluntary Contributions (donations) Section 11(1)

- II. Income From Property held under trust for charitable and religious purposes

- III. Capital Gains (Sec 11(1A)

- IV. Anonymous Donations (Sec 115BBC)

- Cases where anonymous donations shall not be taxable u/s 115BBC

- Section 13: Section 11 not to apply in certain cases:

I. Voluntary Contributions (donations) Section 11(1)

Voluntary contributions are basically the donations received by the charitable/religious trust which form part of income of the trust.

They are of two types:

1) Donations received with specific direction that they shall form part of corpus fund

Such donations are exempt

2) Donations received without such specific instruction

Such donations shall form part of income from trust property

II. Income From Property held under trust for charitable and religious purposes

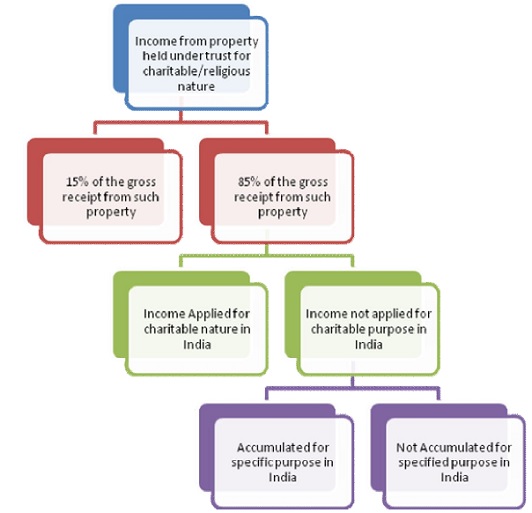

| Particulars | Taxability | ||||||||||

| 15% of gross receipts from such trust property | Exempt | ||||||||||

| 85% of gross receipt from such trust property | |||||||||||

| i. Income Applied for Charitable Purposes in India | Exempt (Sec11(1))to the extent to which applied for the following purposes:

1. Purchase of capital asset 2. Repayment of loan for purchase of capital asset 3. Revenue Expenditure 4. Donation to trust registered u/s 12AA or u/s 10(23C) |

||||||||||

| Income deemed to be applied for charitable purpose in India:

In case whole or part of income is not received during that year in which it is derived |

-Exempt in case :

a. Income is applied for charitable purpose in India in the year of receipt or in the immediate succeeding year. b. Assessee submits a declaration to the Assessing Officer on or before the due date of filling of return as per section 139(1) that such income shall be applied for such purpose in the year of receipt or succeeding year. |

||||||||||

| In any other case

|

-Exempt in case :

a. Such income is applied in above mentioned charitable purposes in the immediately succeeding year. b. Assessee submits a declaration to the Assessing Officer on or before the due date of filling of return as per section 139(1) that such income shall be applied for such purpose in the immediate succeeding year. |

||||||||||

| II. Income not applied for charitable/religious purpose in India

Accumulated for specific purpose in India Q) What are the modes in which income shall be accumulated for specific purpose (sec 11(5))?? A) 1. Investment in government saving certificate/UTI 2. Deposit in post office savings bank/scheduled bank. 3. Investment in immovable property. 4. Deposit with or investment in bonds of a public co. having main object of providing long term finance for urban infrastructure/industrial development/ residential house, in India

|

♠ Exempt (sec 11(2)) in case accumulated for specific purpose in India subjected to the following conditions:

A) Assessee gives notice to Assessing officer specifying purpose and period (cannot exceed 5 years) of accumulation before assessment is complete. B) Accumulated amount is deposited /invested in specified form. ♠ Withdrawal of Exemption in the following cases (sec11(3)):

|

||||||||||

| Not accumulated for specific purpose in India | Taxable in case income is not applied for charitable/religious purpose in India and is also not accumulated for specific purpose in India. |

III. Capital Gains (Sec 11(1A)

The capital gain arising from the transfer of a property held by religious/charitable trust shall be taxable as under:

1) Cost of new asset ≥ net consideration from asset sold → Entire capital gain is exempt

2) Cost of new asset < net consideration from asset sold → Capital Gains Exempt = Cost of new asset less Cost of old asset

IV. Anonymous Donations (Sec 115BBC)

Q) What are anonymous donations??

A) Anonymous donations are basically the donations where the person receiving the donations doesn’t maintain any record of the person giving the donation. E.g. – Offerings given in temple in donation box.

Taxability

Step 1: Compute the total amount of anonymous donation received by the charitable/religious institution

Step 2 : Compute 5% of the total donations(corpus donations + anonymous donations + other donations not forming part of corpus)

Step 3 : Select the higher of the following two:

a) Amount computed in step 2 or

b) 1,00,000

The amount computed in step 3 shall be exempt and the remaining amounts of anonymous donations are taxable in the hands of such charitable/religious institution @ flat 30% (115BBC)

Cases where anonymous donations shall not be taxable u/s 115BBC

1) Where donations are received by trust established WHOLLY for RELIGIOUS purpose (no charitable purpose). E.g.-donations given by devotees to trust owning a temple.

2) However in case such religious/charitable trust also runs a school/medical institution/educational institution ,etc and the donations are received with specific direction that they are for such school/institution then such donations shall be taxable

Anonymous donations not taxable u/s 115BBC → taxable as per section 11 & 12

Anonymous donations taxable u/s 115BBC → not exempted u/s 11 & 12

Section 13: Section 11 not to apply in certain cases:

1. Entire income from the property held under a trust for private religious purposes which does not enure for the benefit of the public.

2. Entire income of a charitable trust or institution created or established for the benefit of any particular religious community or caste.

3. Entire income of the following charitable/religious trust:-

a) where any part of the income of such trust is used for the benefit of any person specified under sec 13(3) or

b) Where any property of the trust id used for the benefit of any person specified under sec 13(3)

4. Entire income of a charitable /religious trust whose funds are not invested in modes specified under section 11(5).

Hope this article helped you in understanding the taxation of charitable/religious trust. For any further query please at [email protected]

Republished with Amendments

need an expert on religious property’s tax issue. He/she must be aware of latest BMC property tax rules, about HC & SC orders in favour of property tax waiver on religious trusts.

kindly treat this as urgent & email ur reply.

thank you.

Dear

Please tells me in trust Income applied is 15% of Net income or gross receipt.?? as per law only mention 15% of the Income earned??

Interest income from FD By a trust created as corpus fund ?

Can trust claim exemption on int income received from fd kept as corpus fund ?

IS anonymus donation taxable for non registered religious trust??

kindly suggest as soon as possible

Can a Religious Institution give loan( application of funds) to other religious Institution registered under 12AA

A Private trust having 20 founder trustees running school. Now some of them wants to leave and demand money out of the total assets. How they should be paid. What are all other formality to be followed.

if a trust has income from share from profit in aop and aop is assessed at MMR and member share is exempt in such case whether section 11(7) shall be applicable for such exempt income?

On which amount there is need to take PAN Number of Doner by a charitable Trust ( Cash Or in kind )

I could not understand the concept of business income of charitable trust where business is incidental or not

Please somebody explain me

I could not understand the concept of business income of charitable trust where business is incidental or not !?

Please somebody explain !

Trust does not have 12A/ 12AA. Total Donation Received during the year Rs.13 Lakh, Rs. 11 Lakh spent to buy a property. Balance Rs. 2 Lakh spend for other Objects of Trust. What is the taxable income ?

Kindly suggest

Is there any real benefit in accumulating 15% of trust income when the total income is below taxable limit? For example trust income is Rs.15,00,000/- it has spent 14,37,000/- towards charitable/ religious/ admin expenses. Balance income Rs.63000/- which is much below taxable limit.

i am running school, our gross receipt Rs. 3450150/ and expences Rs. 3405150 Surplus amt of income expendure A/c Rs. 55000/- for the f.y. 2013-14, no any doneation received during the year. whether filing of ITR is required. if yes, inwhich form. with necessary guideline.

Dear sir, Our trust is not registered under 12A, and it is religious trust. under which section assessment will be done and which ITR should I file. ITR 7 or ITR 5 as AOP ?

our is a public charitable trusthaving registration u/s 12AA & 80G.

We areplanning to do fund raising programme by issuing souvinear. income is by way of advertisement & sale of passes for the programme. Is there any restriction on collection by way of sale of tickets & advertisement.Any amendment in finance act 2015.

taxability of Corpus Fund donations (Temple Building Fund) received by a religious trust yet to be registered u/s. 12A?

Whether Corpus Fund donations (Temple Building Fund) received by a religious trust yet to be registered u/s. 12A?

our samaj trust register under BPT ACT 1950(XXIX) not apply for 12AA wheather income and donation received taxable ?

our source of income interest on FD.

Specific fund received for specific purpose of religious.and can donar be a permenent trustee ?

pls.reply

sirs, A temple in adambakkam which has no trust, perform the function by lot of individuals on their own. When the money received by the gurukkal is more than the expense, and it is of sufficient lump sum, they make deposit in nationalised bank in different amount and different periods in the name of the deity or in the name of the temple.

Now the income tax department issued notice under section 133(6) of the Income tax act, 1961 . One more letter was received the temple that pan number of the devasthanam.

also now the banker's claims that TAX DEDUCTED AT SOURCE will be made on the interest credited by the bank.

Temple requests not to deduct tax.

what will be the consequences.

sirs, A temple in adambakkam which has no trust, perform the function by lot of individuals on their own. When the money received by the gurukkal is more than the expense, and it is of sufficient lump sum, they make deposit in nationalised bank in different amount and different periods in the name of the deity or in the name of the temple.

Now the income tax department issued notice under section 133(6) of the Income tax act, 1961 . One more letter was received the temple that pan number of the devasthanam.

also now the banker’s claims that TAX DEDUCTED AT SOURCE will be made on the interest credited by the bank.

Temple requests not to deduct tax.

what will be the consequences.

Dear Sir/Mam

WHETHER PROPERTY MADE THROUGH GIFT TO A CHARITABLE TRUST IS EXEMPT UNDER INCOME TAX OR NOT ?

thanks

Whether d corpus fund donation received, which is totally spent for the purpose by a trust would be taxable which is yet to be registered Under 12A.

Thanks

If the Public Charitable Trust with Corpus fully invested in FD,wants to close don the charitable activity,what is the legal procedure involved?

Wonderful. Very easy to understand .

Request you to provide me the Proforma of declarations u/s -11(5) and 13(1)(c) of Income Tax Act.

thanks & regards

CA. Vara Prasad P.V.S

thanks for tabular format and ‘T’diagram.it become very easy to understand.

if trust not registered u/s.12aa Donation income is taxble income?

donation consider others income but ITR 7 is not considar others income

An excellent summary- add information on s-11 disallowances and plugging of the double deduction through budget 2014.

How would be the taxation of corpus fund donations received by a trust, which was denied for 12A registration by CIT

what :s the status of top 10 such trusts in india…eg tirupati/ shirdi etc,??

Nice work…thnx fr making it too simple..