This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

Immunity from penalty as provided under Explanation 5 to Section 271(1)(c) despite non disclosure of manner in which income is derived

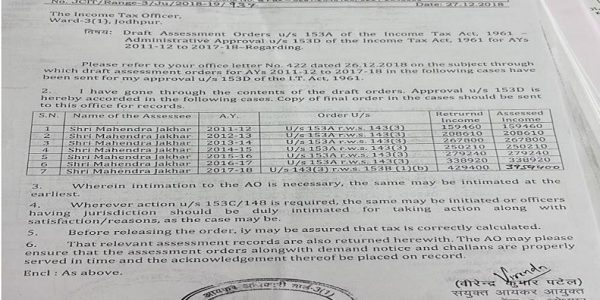

Case Law Details

- Case Name

- Commissioner Of Income Tax Vs Mahendra C. Shah (Gujarat High Court)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Courts

- All High Courts, Gujarat High Court

In the present case, admittedly the Assessment Year being 1988-89 and the search having taken place on 03.07.1987 the return of income was not due before 31.07.1988. Therefore, whether the income represented by the value of the asset was shown in the return of income or not became irrelevant once a declaration had been made about such income having not been disclosed till the date of search in the return of income to be furnished before the time specified in Section 139(1) of the Act as required by the earlier part of Exception No. 2. In fact, at the cost of repetition, it is required to be st...