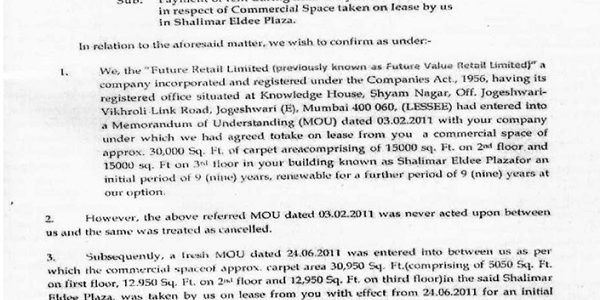

This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

Beneficial ownership is relevant than legal ownership to claim depreciation – SC

Case Law Details

- Case Name

- Mysore Minerals Ltd. Vs Commissioner of Income-tax (Supreme Court of India)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Courts

- Supreme Court of India

SUPREME COURT OF INDIA

Mysore Minerals Ltd.

vs

Commissioner of Income-tax

Civil Appeal No. 5374 OF 1994,

[1999] 239 ITR 775 (SC)

Date of Pronouncement – 01.09.1999

JUDGMENT

R.C. Lahoti J.—The appellant-assessee is a private limited company. During the assessment year 1981-82 (accounting year ending on March 31, 1981), the assessee had purchased for the use of its staff seven low income group houses from the Housing Board. The assessee had made part payments and was in turn made allotment of the houses followed by delivery of possession by the Housing Board. The actual deed of conveya...