Objective & Background

-To mitigate the concerns of public in digital lending ecosystem which primarily relate to unbridled engagement of third parties, mis-selling, breach of data privacy, unfair business conduct, charging of exorbitant interest rates, and unethical recovery practices.

-Against this, RBI had constituted a Working Group on ‘digital lending including lending through online platforms and mobile apps’ (WGDL) and after taking into account the inputs received form stakeholders by way of public comments, a regulatory framework to support orderly growth of credit delivery through digital lending methods while mitigating the regulatory concerns, has been firmed up.

Read: Recommendations of Working group on Digital Lending – Implementation

Important Phrases/definitions

Digital Lending- A remote and automated lending process, majorly by use of seamless digital technologies in customer acquisition, credit assessment, loan approval, disbursement, recovery, and associated customer service

Lending Service Providers (LSPs)- An agent of a Regulated Entity who carries out for a fee from the Regulated Entity (“RE”), one or more of lender’s functions in customer acquisition, underwriting support, pricing support, disbursement, servicing, monitoring, collection, recovery of specific loan or loan portfolio

Digital Lending Apps (DLAs) Mobile and web-based applications with user interface that facilitate borrowing by a borrower from a digital lender. DLAs will include apps of the REs as well as operated by LSPs which are engaged by REs for extension of any credit facilitation services

Annual Percentage Rate (APR)- APR shall be based on an all-inclusive cost and margin including cost of funds, credit cost and operating cost, processing fee, verification charges, maintenance charges, etc., except contingent charges like penal charges, late payment charges, etc. APR must be disclosed to the borrower upfront as part of the Key Fact Statement (KFS).

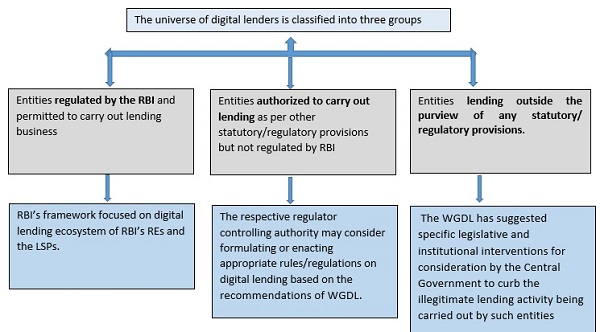

RBI’s framework

RBI has examined the recommendations and divided the same in three parts:-

Annexure-1[1]–Recommendations accepted for immediate implementation and the consequent regulatory stance

Annexure-2- [2]Recommendations, though accepted in-principle, which require further examination

Annexure-3-[3]Recommendations which require wider engagement with the Government of India and other stakeholders in view of the technical complexities, setting up of institutional mechanism and legislative interventions

Highlights of Mandatory requirements

A. Customer Protection and Conduct Issues

1) Loan disbursals and repayments to be executed only between bank a/c of borrower and RE without any pool a/c of LSP or any third party

2) Any fees to be charged by LSP to be paid by RE and not borrower.

3) Key Fact Statement (KFS) to be provided to borrower before execution of loan

4) APR to be disclosed to borrowers also form part of KFS.

5) No Automatic limit increase without borrower’s consent

6) Cooling off/lookup period for exit of borrowers shall form part of loan contract.

7) REs and LSPs shall have a nodal grievance redressal officer to deal with FinTech/ digital lending related complaints and to be disseminated on their website

8) If any complaint by borrower not resolved within 30 days, borrower can lodge a complaint under Reserve Bank – Integrated Ombudsman Scheme (RB-IOS)

B. Technology and Data Requirements

1) Clear Audit trails of data collected by DLAs and with prior explicit consent of the borrower.

2) Option for borrowers for use of specific data, including option to revoke previously granted consent, besides option to delete the data collected from borrowers by the DLAs/ LSPs.

C) Regulatory Framework

1) Any lending by DLAs (either of the RE or of the LSP engaged by RE) is required to be reported to Credit Information Companies (CICs) by REs irrespective of its nature or tenor

2) New digital lending products extended over merchant platforms involving short term credit or deferred payments are required to be reported to CICs by the REs

Note:-

The onus of ensuring implementation of the requirements will rest with the REs. Detailed instructions will be issued separately.

Source:-

[1] https://rbidocs.rbi.org.in/rdocs/content/pdfs/PR689DL10082022_AN1.pdf

[2] https://rbidocs.rbi.org.in/rdocs/content/pdfs/PR689DL10082022_AN2.pdf

[3] https://rbidocs.rbi.org.in/rdocs/content/pdfs/PR689DL10082022_AN3.pdf

Author Bio