Regulatory Implications of Transition From ‘NRI’ To ‘OCI’ Status in Relation to Transactions in Immovable Property; Why Transition From NRI to OCI Has No Impact on Indian Property Transactions; Immovable Property Rules Remain Unchanged Despite NRI–OCI Status Shift; Uniform FEMA Treatment for NRIs and OCIs in Real Estate Matters Explained; Tax and Repatriation Rules Stay the Same After Conversion From NRI to OCI.

Overview

Transactions undertaken in India by Non-Resident Indians (“NRIs”) and Overseas Citizens of India (“OCIs”) are regulated under the provisions of the Foreign Exchange Management Act, 1999, as amended (“FEMA Act”) and rules framed thereunder, read in consonance with the Reserve Bank of India (“RBI”) guidelines and directions issued from time to time along with the Income-tax Act, 1961 (“IT Act”) and rules framed thereunder, each as amended.

Relevant Definitions

- A person resident outside India is defined under FEMA Act as a person who is not resident in India. Therefore, if a person:

-

- Not residing in India for more 182 days during the course of the preceding F.Y.

- Indicate his intention to stay outside India for an uncertain period would fall under the definition of ‘resident outside India’.[1]

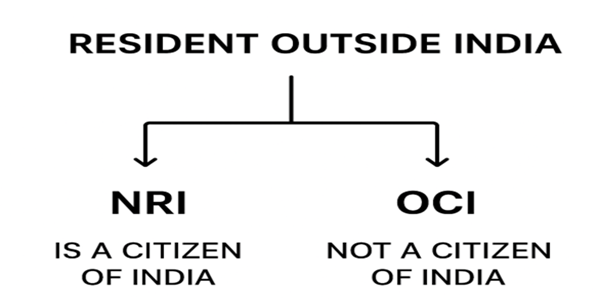

- Non-Resident Indian (“NRI”) means a person resident outside India who is a citizen of India, as defined under Foreign Exchange Management (Deposit) Regulations, 2016.[2]

- Overseas Citizen of India (“OCI”) means a person registered as an Overseas Citizen of India Cardholder by the Central Government of India under The Citizenship Act, 1955.[3]

- Remittance of asset means remittance outside India of funds representing sale proceeds of immovable property or any other asset held in India in accordance with the provisions of the Foreign Exchange Management (Remittance of Assets) Regulations, 2016.[4]

- Relative: A person shall be deemed to be the relative of another, if he or she is related to another in the following manner, as defined under The Companies Act, 2013[5] read with The Companies (Specification of Definitions Details) Rules, 2014[6] :

-

- Father (including ‘step-father’)

- Mother (including ‘step-mother’)

- Son (including ‘step-son’)

- Son’s wife

- Daughter

- Daughter’s husband

- Brother (including ‘step-brother’)

- Sister (including ‘step-sister’)

Analysis

After a thorough analysis of the aforementioned statutory provisions, legislations and other relevant authoritative sources including, inter alia, RBI and Government circulars, notifications, rules and notices, it can be conclusively stated that the legal framework governing the acquisition and transfer of immovable property in India applies identically to NRIs and OCIs. The relevant legislation employs these classifications interchangeably for the purposes of immovable property transactions without the prior approval of RBI, thereby placing both categories on an equivalent legal footing, subject to the limitations outlined below as enshrined in Foreign Exchange Management (Non-debt Instruments) Rules, 2019[7]:

- NRI/OCI may acquire immovable property in India other than an agricultural land or farm house or plantation property.

- The consideration for such transfer shall be made out of : (i) funds received in India through banking channels by way of inward remittance from any place outside India ; or (ii) funds held in any non-resident account maintained in accordance with the provisions of the Act, rules or regulations framed thereunder.

Provided further that no payment for any transfer of immovable property shall be made either by traveller’s cheque or by foreign currency notes or by any other mode.

- NRI/OCI may acquire any immovable property in India other than agricultural land or farm house or plantation property by way of gift from a person resident in India or from an NRI or from an OCI, who in any case is a ‘relative’.

- Under a deed of settlement made by either of his parents or a relative and the settlement taking effect on the death of the settler, on production of the original deed of settlement.

- NRI/OCI acquire any immovable property in India by way of inheritance from a person resident outside India or from a person resident in India.

- NRI/OCI may transfer any immovable property in India to a person resident in India.

- NRI/OCI may transfer any immovable property other than agricultural land or farm house or plantation property to an NRI or an OCI.

- In the case of residential property, the repatriation of sale proceeds is restricted to not more than two such properties.

- NRI/OCI may remit, through an authorised dealer[8], an amount not exceeding USD 1 million per F.Y.

Provided the aforesaid remittance is made in more than one instalment, the remittance of all instalments shall be made through the same Authorised Dealer.

Furthermore, IT Act does not differentiate between NRI and OCI, it only mentions ‘non-resident’/’ not ordinarily resident’ under the Section 2(30) read with Section 6(6) of the aforesaid act.[9] Therefore, it can be deduced that tax implications also remains the same to that of NRI and OCI w.r.t. transactions in immovable property.

Note: The only material difference between the rights of NRIs and OCIs pertains to differential rights of a ‘citizen’ and a ‘non-citizen’ under The Citizenship Act, 1955.

[1] Foreign Exchange Management Act, No. 42 of 1999, § 2(w).

[2] Foreign Exchange Management (Deposit) Regulations, 2016, Reg. 2(vi).

[3] The Citizenship Act, No. 57 of 1955, § 7A.

[4] Foreign Exchange Management (Remittance of Assets) Regulations, 2016, Reg. 2(v).

[5] The Companies Act, No. 18 of 2013, § 2(77).

[6] Companies (Specification of Definitions Details) Rules, 2014, Rule 4.

[7] Foreign Exchange Management (Non-debt Instruments) Rules, 2019, Rule 24, 29.

[8] Foreign Exchange Management Act, No. 42 of 1999, § 10(1).

[9] Income-tax Act, No. 43 of 1961, § 2(30) and 6(6).