The retail sector in India is one of the biggest contributors to the economy in terms of revenue and contributes about 10% towards its GDP. It provides the second highest rate of employment after agriculture. The retail sales in India are growing at a compounded annual rate of 15% since the year 2014.

The total market size of Indian retail industry reached US$ 672 billion in 2017. It is forecasted to increase to US$ 1,200 billion by 2021 and 1,750 billion by 2026.

Now, let’s take a look at what % FDI is allowed in retail trading sector:

| Sector/ Activity | % of Equity / FDI cap | Entry Route |

| Single Brand Product Retail Trading- E-commerce activities | 100%

100% |

Automatic route

Automatic route |

| Multi Brand Retail Trading | 51% | Government route |

| Duty Free Shops | 100% | Automatic route |

As per the latest policy issued by Department of Industrial Policy and Promotion (DIPP), 100% foreign direct investment (FDI) is allowed in case of single brand retail through automatic route with few strings attached as below:

- Only those products that are branded during manufacturing and also sold under the same brand in other countries will be covered under this.

- Although, where the FDI is more than 51%, at least 30% of the value of goods should be sourced from India. This was in view to promote domestic sectors in India i.e. micro, small and medium enterprises, village and cottage industries, artisans and craftsmen. As a relief to the companies, in the initial five years, this requirement has to be made as an average of total value of goods purchased in the five years. After that, every year 30% requirement has to be completed.

However, FM Nirmala Sitharaman announced in Union Budget 2019 that local sourcing norms will be eased for FDI in single brand retail sector in case of ‘state-of-art’ and ‘cutting-edge technology, subject to government approval. The relaxation of mandatory 30% local sourcing norm will spur the growth of the Indian economy, and will potentially help in attracting large players in the single-brand retail sector.

The policy also allows a single brand retail entity which is operating through brick and mortar stores, to trade through e-commerce. Indian entity has to make sure that all the compliances has been fulfilled whereas the investing entity will be responsible to file the evidence with RBI to prove the effective compliance.

The FDI policy in India allows e-commerce activities under automatic route with 100% equity, subject to below conditions:

- E-commerce entities would engage only in Business to Business (B2B)e-commerce and not in Business to Consumer (B2C) e-commerce.

- Moreover, India allows 100 percent foreign direct investment (FDI) in the marketplace model of e-commerce, which it defines as a tech platform (or a facilitator) that connects buyers and sellers.

- It has not allowed FDI in inventory-driven models of e-commerce.

However, the Department of Industrial Policy and Promotion (DIPP) updated Press Note 2 (2018 series) to provide clarity on the functioning of an e-commerce marketplace as below:

i) Digital and electronic network will include network of computers, television channels and any other internet application used in automated manner such as web pages, extranets, mobiles, etc.

ii) E-commerce marketplace may provide support services to sellers in respect of warehousing, logistics, order fulfillment, call center , payment collection and other services.

iii) E-commerce entity providing a marketplace cannot exercise ownership over the inventory i.e. goods purported to be sold. Such an ownership over the inventory will render the business into inventory based model.

iv) An e-commerce entity shall not permit more than 25% of the sales value on financial year basis affected through its marketplace from one vendor or their group companies.

v) In marketplace model goods/services made available for sale electronically on website should clearly provide name, address and other contact details of the seller. Post sales, delivery of goods to the customers and customer satisfaction will be responsibility of the seller.

vi) An entity having equity participation by e-commerce marketplace entity or its group companies, or having control on its inventory by e-commerce marketplace entity or its group companies will not be permitted to sell its products on the platform run by such marketplace entity.

vii) In marketplace model, payments for sale may be facilitated by the e-commerce entity in conformity with the guidelines of the Reserve Bank of India.

viii) In marketplace model, any warrantee/ guarantee of goods and services sold will be responsibility of the seller.

ix) E-commerce entities will not mandate any seller to sell any product exclusively on its platform only.

x) E-commerce entities providing marketplace will not directly/ indirectly influence the sale price of goods/ services and shall maintain level playing field. Services should be provided by e-commerce entity or other entities in which e-commerce marketplace entity has direct/ indirect equity participation or common control, to vendors on platform at arm’s length and in a fair and non-discriminatory manner.

xi) E-commerce entity will be required to furnish a certificate along with a report of statutory auditor to RBI, conforming compliance of above guidelines, by 30th September of every year for preceding FY.

Subject to the conditions of FDI policy on services sector and applicable laws/regulations, security and other conditionalities, sale of services through e-commerce will be under automatic route.

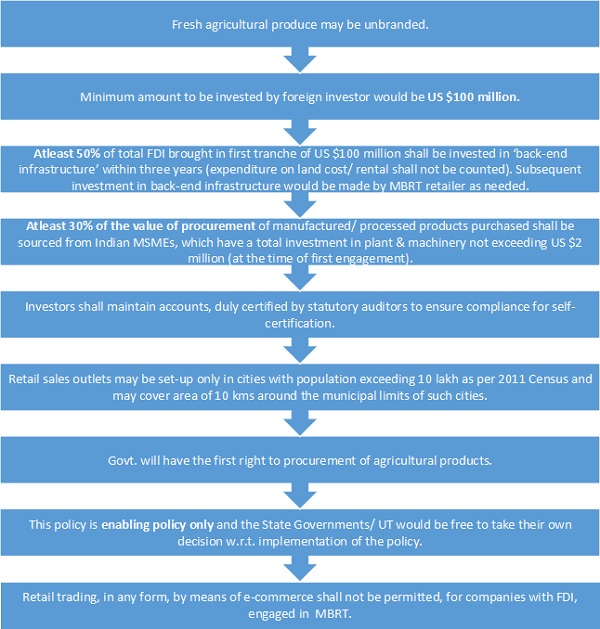

Moreover, FDI in multi-brand retail in India is limited to 51% equity, and that too with government approval. Further, it shall be permitted, subject to below conditions:

Moreover, FDI in Duty Free Shops is also allowed under automatic route with 100% equity, subject to regulations of Customs Act. However, Duty Free Shop entity shall not engage into any retail trading activity in the Domestic Tariff Area of the country.

About the Author

Author is Neeraj Bhagat, FCA helping foreign companies in setting up of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. He is also founder of Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi. He can be reached at info@neerajbhagat.com.

Author is Neeraj Bhagat, FCA helping foreign companies in setting up of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. He is also founder of Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi. He can be reached at info@neerajbhagat.com.