The Finance Act, 2021, has inserted Section 194Q, in Income Tax Act, 1961 with effect from 01.07.2021, to provide for the deduction of tax (TDS) on certain purchases. The TDS has to be deducted if the value or aggregate purchase value exceeds Rs. 50 lakhs during the previous year.

As per Finance Act, 2021, Section 194Q as inserted in Income Tax Act states that any person, being a buyer who is responsible for paying any sum to any resident (seller) for purchase of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall, at the time of credit of such sum to the account of the seller or at the time of payment thereof by any mode, whichever is earlier, deduct an amount equal to 0.1 per cent of such sum exceeding fifty lakh rupees as income-tax.

Further, where any sum referred to in sub-section (1) is credited to any account, whether called “suspense account” or by any other name, in the books of account of the person liable to pay such income, such credit of income shall be deemed to be the credit of such income to the account of the payee and the provisions of this section shall apply accordingly.

This article provides conceptual understanding of new provision and how it will affect the assessees.

- Person liable to deduct tax under section 194Q of Income Tax Act, 1961

The tax shall be deducted under Section 194Q by a buyer carrying on a business whose total sales, gross receipts or turnover from the business exceeds Rs. 10 crores during the financial year immediately preceding the financial year in which such goods are purchased. This provision shall be applicable from 01-07-2021.

Thus, the liability to deduct tax under this provision in the financial year 2021-22 shall arise if the turnover of the purchaser was more than Rs. 10 crores in the financial year 2020-21.

- When to be deduct TDS

The tax shall be deducted from the purchases made by a buyer if the following conditions are satisfied:

a) There is a purchase of goods from a resident person;

b) Goods are purchased for a value or aggregate of value exceeding Rs. 50 lakhs in any previous year; and

c) The buyer should not be in the list of persons excluded from the provision for deduction of tax. The tax shall not be deducted under this provision if the tax is deductible or collectible under any other provision except Section 206C(1H). Thus, if a transaction is subject to TCS under Section 206C(1H), the buyer shall have the first obligation to deduct the tax. If he does so, the seller will not have any obligation to collect the tax under Section 206C(1H).

- Timing of deduction of tax

Tax is required to be deducted at the time of credit of such sum to the account of the seller or at the time of payment thereof by any mode, whichever is earlier. The tax shall also be deducted if the sum is credited to any ‘Suspense Account’.

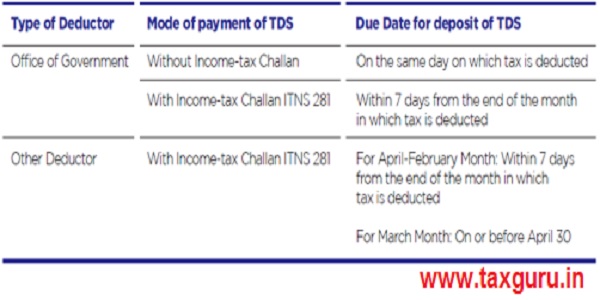

- Deposit of TDS – how to be made

A corporate assessee and other assessees (who are subject to tax audit under Section 44AB) will have to make payment of tax (including TDS) electronically through internet banking facility or by way of debit cards. To deposit the tax, the deductor has to fill the Challan No. ITNS 281.

Other deductors can deposit the tax so deducted into any branch of the RBI or the State Bank of India or any authorized bank.

- Due date to deposit TDS

Tax deducted during the month shall be deposited on or before the following due date:

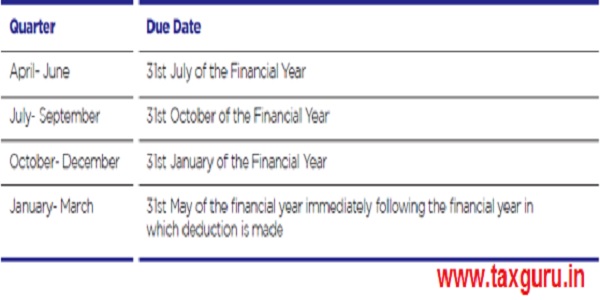

Due date for filing of TDS return?

The statement of tax deducted at source under this provision shall be filed with the Income-tax Department on or before the following due date:

TDS to be deducted at what rate

The tax shall be deducted by the buyer of goods at the rate of 0.1% of the purchase value exceeding Rs. 50 lakhs if the seller has furnished his PAN or Aadhaar, otherwise, the tax shall be deducted at any rate of 5%.

Tax collection at source [Section 206C(1H)]

The Finance Act, 2020 inserted a new sub section (1H) to section 206C of the Income Tax Act, 1961 (IT Act) widening the scope of tax collection at source which provides that every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year shall, at the time of receipt of such amount, collect from the buyer, a sum equal to 0.1 per cent of the sale consideration exceeding fifty lakh rupees as income-tax.

What if both TDS and TCS are applicable?

Second Proviso to Section 206C(1H) provides that if the buyer is liable to deduct tax under any other provision on the goods purchased by him from the seller and has deducted such amount, no tax shall be collected on the same transaction. Section 194Q(5) provides that no tax is required to be deducted by a person under this provision if tax is deductible under any other provision or tax is collectable under section 206C [other than a transaction on which tax is collectable under Section 206C(1H)].

Though Section 206C(1H) excludes a transaction on which tax is actually deducted under any other provision (which will cover Section 194Q as well), but Section 194Q(5) does not create a similar exception for a transaction on which tax is collectible under Section 206C(1H). Thus, the buyer shall have the primary and foremost obligation to deduct the tax and no tax shall be collected on such transaction under Section 206C(1H). However, if the buyer makes a default, the liability to collect the tax gets shifted to the seller.

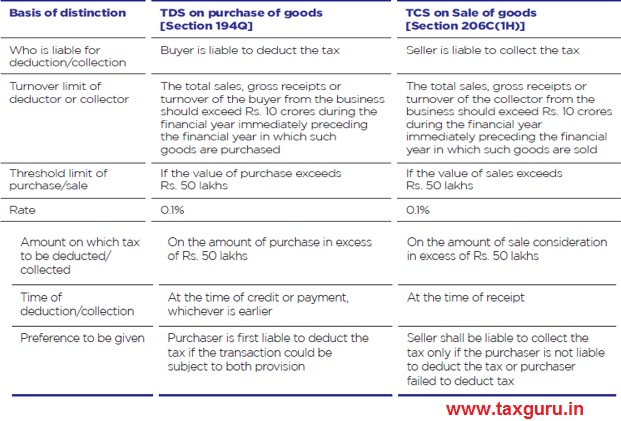

TCS and TDS can be compared as follows:

- Liability of buyer importing goods (say motor vehicles) from outside India

Section 194Q provides that any person, being a buyer who is responsible for paying any sum to any resident, being a seller, is required to deduct tax at source under this provision. Thus, the obligation to deduct tax under this provision arises only when the payment is made to a resident seller. As in the case of import, the seller is a non-resident, the buyer will not have any obligation to deduct tax under this provision. However, the TDS under Section 195 or payment of Equalisation Levy may be required in respect of such transaction.

- Scope of ‘goods’

The term ‘goods’ is not defined in the Income-tax Act. However, the term ‘goods’ is of wide import. Anything which comes to the market can be treated as goods. However, this term ‘Goods’ has been defined under the Sale of Goods Act, 1930.

As per section 2 (7) of Sale of Goods Act, 1930 ‘goods’ means every kind of movable property other than actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale

The Sale of Goods Act, 1930 is a specific statute which deals with the ‘sale of goods’ whereas the CGST Act, 2017 deals with tax on ‘supply of goods’. Thus, the definition of term ‘goods’ can be referred to from the Sale of Goods Act, 1930 for the purpose of Section 194Q.

Therefore, the tax is to be deducted under this provision from the purchase value of the goods such as (illustrative):

- Movable property;

- Any commodity;

- Fuel;

- Motor vehicle;

- Scraps

It may be noted that all type of motor vehicles, viz, two wheelers, four wheelers, commercial vehicles etc shall be covered.

- TDS on the purchase of immovable property (say a showroom)

As referred to above, ‘goods’ means every kind of movable property subject to certain exceptions and inclusions. Thus, the immovable property shall not be treated as ‘goods’. Consequently, the TDS shall not be deducted under section 194Q from the purchase of immovable property by a developer.

- Purchase value

It is imperative to accurately determine the purchase value as it is relevant both for the applicability of the provision and amount from which tax should be deducted. Additional, allied or out-of-pocket charges recovered from the customers may or may not form part of purchase value. Where these expenses have been reflected in the purchase invoice itself, it should form part of purchase value. If they are charged through a separate invoice, it should not form part of purchase value.

- Threshold limit of Rs. 50 lakhs

The Finance Act, 2021, has inserted Section 194Q, with effect from 01-07-2021, to provide for the deduction of tax on certain purchases. The TDS has to be deducted if the value or aggregate purchase value exceeds Rs. 50 lakhs during the previous year. How this limit of Rs. 50 Lakh for deducting TDS shall be reckoned for the financial year 2021-22? Should it be from 01-04-2021 or 01-07-2021?

It may be noted that similar confusion arose when Section 206C(1H) was introduced by the Finance Act, 2020, with effect from 01-10-2020. In respect of which the CBDT vide Circular No. 17, dated 29-09-2020, has clarified that since the threshold of Rs. 50 lakhs is with respect to the previous year, calculation of sale consideration for triggering TCS under this provision shall be computed from 01-04-2020. Hence, if a seller has already received Rs. 50 lakhs or more up to 30-09-2020 from a buyer, TCS under this provision shall apply on all receipts of sale consideration on or after 01-10-2020.

Applying the same principle it should be concluded that threshold of Rs. 50 lakhs shall be computed from 01-04-2021. Thus, if a buyer has already purchased goods of value Rs. 50 lakhs or more up to 30-06-2021 from a seller, TDS under this provision shall apply on all purchases on or after 01-07-2021.

- Value for TDS – GST included?

When tax is deducted at the time of credit of amount in the account of the seller and the component of GST comprised in the amount payable to the seller is indicated separately in the invoice, then TDS shall be deducted on the amount credited without including such GST.

In other cases, where GST is not shown separately, Income tax TDS is required to be deducted on the gross Invoice value. (e.g. composition dealers).

- TDS on advance payment made to dealer

Section 194Q provides that tax is required to be deducted in the transaction relating to the purchase of goods. It does not mention whether such purchase needs to be effected immediately or at a future date. As the tax is required to be deducted at the time of payment or at the time of credit, whichever is earlier, it should be reasonable to conclude that the provision may get attracted even if such purchase happens in future.

As long as the intention is to adjust the advance payment against the future purchase of goods, the tax should be deducted at the time of payment or credit, whichever is earlier. If the advance payment is not made with an intention to adjust it against future purchase (deposit or loan) but eventually it is adjusted against the future purchase, no tax is required to be deducted at the time of payment of such advance. In such case liability to deduct tax will arise the moment such advance is adjusted against the purchase value of goods.

- TDS on payment of advance received before 01-07-2021 for purchase of goods

The Finance Act, 2021, has proposed to insert Section 194Q with effect from 01-07-2021. Thus, provisions of this Section shall not apply on any payment made or credit made in the books of accounts before 01-07-2021. Consequently, it would apply to all purchases made on or after 01-07-2021.

Simply put, the tax should be deducted where the payment is made or amount is credited on or after 01-07-2021. Thus, where any of the trigger event (i.e., payment or credit) has occurred before the date of applicability of provision, no liability to deduct tax will arise.

- Impact on inter branch transfers

The TDS under section 194Q is required to be deducted by any person, being a buyer, responsible for making payment to the seller for the purchase of goods. Thus, the existence of two distinct parties as ‘seller’ and ‘buyer’ is a pre-requisite to construe a transaction as a purchase. The condition of purchase is not fulfilled in the context of branch transfer. Therefore, the provisions of this section shall not apply in the case of branch transfers.

- Consequences of non-filing of TDS return

If there is a delay in filing of TDS return, the late filing fee shall be payable under Section 234E. The fee for default in furnishing the TDS/TCS Statement shall be levied at the rate of Rs. 200 per day during which such failure continues. However, the amount of fee shall not exceed the total amount deductible or collectable, as the case may be. The fee shall be payable before submission of the belated TDS/TCS Statement.

If a person fails to file the TDS return or does not file it by the due dates, he shall be liable to pay penalty under Section 271H. The penalty under Section 271H is also levied in case of furnishing of inaccurate information under TDS return. The minimum amount of penalty for failure to furnish TDS return or providing inaccurate information therein is Rs. 10,000 which can go up to Rs. 1,00,000.

- Consequences for failure to deduct or pay TDS

If any person, responsible for deduction of tax at source, fails to deduct the whole or any part of the tax or after deduction fails to deposit the same to the credit of the Central Government, then he shall be deemed to be an assessee-in-default.

If deductor fails to deduct tax at source, he shall be liable to pay interest at the rate of 1% for every month or part thereof on the amount of tax he failed to deduct. However, if he fails to deposit the tax deducted at source, he shall be liable to pay interest at the rate of 1.5% for every month or part thereof on the amount of tax he failed to deposit to the credit of the Central Govt.

FADA members are advised to carefully examine the liability of TDS or TCS and ensure compliances along with proper rate for tax collection or deduction as the cost of non compliance would result in interest / penalties and disallowances under Income Tax Act, 1961.

***********

Author Bio