Introduction: Section 43B of the Income Tax Act, 1961, delineates the criteria for allowable deductions based on actual payments. Among its provisions, Section 43B(h) specifically addresses payments to micro and small enterprises, outlining conditions for deduction eligibility. This article provides an insightful analysis of Section 43B(h), its implications, and the necessary steps for compliance.

1. Section43B of the Act is the section that governs the allowability of certain deductions on an actual payment basis. This section provides an explanation wherein certain expenses are allowed as deduction while calculating the income from business or profession based on the previous year in which such sum is actually paid by the assessee. However, expenses will be allowed as deduction even if it is actually paid by the assessee on or before the due date for furnishing the return of income under section 139(1) and provided that evidence of such payment is furnished by the assessee at the time of filing its return.

2. As we prepare books of accounts on accrual basis which means even if certain expenses not paid during the financial year are allowed to debit in the books of accounts even if it is not yet paid. With the insertion of section 43(B) of the income tax act, 1961, expenses actually paid during the financial year are allowed and if failed to pay within the financial year then even if it is paid before furnishing the return of income under section 139(1) it is allowed to debit in that financial year.

3. Section 43B(h): Any sum payable by the assessee to a micro or small enterprise, beyond the time limit specified in section 15 of the Micro, Small and Medium Enterprises Development Act 2006 shall be allowed as deduction only on actual payment which means that if it is paid on or before furnishing the return of income under section 139(1), it is not allowed to debit in that financial year.

4. Analysis of this provision in simple way:

Sec.43(B) provides relaxation to the assessee with relates to the payment that even if the assessee failed to make the payment before the end of the Financial year and paid on or before the due date of furnishing the Return of Income then it will be allowed as deduction while computing income under the head Profit or Gain from Business/Profession but if the payment which is due to be Paid to the micro or small enterprises is not paid within the time limit prescribed u/s 15 of MSMED Act,2006 then it will not be allowed as deduction while computing income under the head Profit or Gain from Business/Profession for that Financial year and shall be allowed as deduction in the financial year in which it is actually paid.

5. Definition of Micro, Small, Medium Enterprises is as follows:-

|

Classification |

MICRO | SMALL | MEDIUM |

| Manufacturing Enterprises and Enterprises rendering Services | Investment in Plant and Machinery or Equipment:

Not more than Rs.1 crore and Annual Turnover; not more than Rs. 5 crore |

Investment in Plant and Machinery or Equipment:

Not more than Rs.10 crore and Annual Turnover; not more than Rs. 50 crore |

Investment in Plant and Machinery or Equipment:

Not more than Rs.50 crore and Annual Turnover; not more than Rs.250 crore |

6. Definition of Enterprises is as follows:

Section 2(e) “enterprise” means an industrial undertaking or a business concern or any other establishment, by whatever name called, engaged in the manufacture or production of goods, in any manner, pertaining to any industry specified in the First Schedule to the Industries (Development and Regulation) Act, 1951 (55 of 1951) or engaged in providing or rendering of any service or services;

Retail and wholesale trades as MSMEs and they are allowed to be registered on Udyam Registration Portal. However, benefits of Retails and wholesale trade MSMEs are to be restricted to Priority sector lending only.

For the application of section 43(B)(h), the supplier should be registered under MSMED Act,2006 as a Micro and small enterprises as a manufacturer and/or service provider.

It means the definition of enterprises includes only Manufacturers & Servicemen but does not include Traders, Distributors whether wholesalers or retailers.

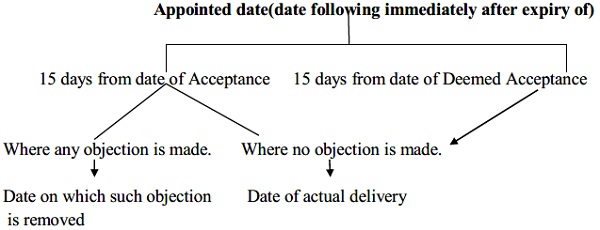

7. Section 2(b) “appointed day” means the day following immediately after the expiry of the period of fifteen days from the day of acceptance or the day of deemed acceptance of any goods or any services by a buyer from a supplier.

Explanation- For the purposes of this clause,-

(i) “the day of acceptance” means,-

(a) the day of the actual delivery of goods or the rendering of services; or (b) where any objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day on which such objection is removed by the supplier;

(ii) “the day of deemed acceptance” means, where no objection is made in writing by the buyer regarding acceptance of goods or services within fifteen days from the day of the delivery of goods or the rendering of services, the day of the actual delivery of goods or the rendering of services;

Generally, the appointed date is 15 days from the date of supply/service in cases where there is no agreement between the parties. However, if there is an agreement between the parties for payment then appointed date is the date agreed between the parties but in any case, the appointed date shall not extend 45 days from the date of service, which means if agreed date is 50 days from date of service then in that case it will end at the end of 45th date from the date of supply/service.

Appointed date is very crucial as if the payment is made within appointed date it will attract interest on delayed payment and interest on delayed payment which is three times of the bank rate notified by RBI is penal in nature and not allowed while computing income under the head business and profession.

Section 15 of the MSMED Act mandates payments to MSMEs within the time as per the written agreement, which cannot be more than 45 days. If there is no such written agreement, the section mandates that the payment shall be made within 15 days.

Author’s view

1. Section 43B allows deduction only on the basis of payment made till filing of return of income.

2. However sec 43(B)(h) also allows deduction to be claimed on the basis of payment which should be made within the end of the financial year and not date of filing of return of income.

3. Suppose the date of goods supplied/service rendered is 31st march 2024 and payment made within 15th april 2024 then it will be allowed as deduction in the financial year ended on 31.03.2024.

4. Generally payment should be made within 15 days from date of supply however if it is mutually agreed between the parties then in any case it shall not exceed 45 days.

5. Only manufacturers and service providers are covered.

6. Interest paid on delayed payments is not allowed as a deduction.

7. Only micro and small enterprises are covered

Steps to be taken in order to comply

1. Obtain MSME certificate along with declaration on the classification of enterprises on the basis of micro, small, medium enterprises.

2. Prepare an age wise analysis of payment made to the supplier.

3. Prepare a sheet on the basis of amount outstanding due to micro, small, medium enterprises as per MSMED Act,2006.

Conclusion: Understanding the nuances of Section 43B(h) of the Income Tax Act, 1961, is imperative for businesses dealing with micro and small enterprises. Compliance entails timely payments to these entities, adhering to the stipulated timelines outlined in the Micro, Small and Medium Enterprises Development Act, 2006. By obtaining the requisite certificates, conducting thorough analyses of payments, and maintaining accurate records, businesses can navigate the regulatory landscape effectively while ensuring adherence to tax laws.

Author Bio