Introduction

Residential status plays a fundamental role in determining the scope of taxation under Indian income tax law. Whether a person is taxed on global income or only on income sourced from India depends primarily on their residential status. Section 6 of the Income Tax Act, 2025 lays down the provisions for determining the residential status of various persons including individuals, Hindu Undivided Families (HUF), firms, companies and other entities.

The concept of residence under tax law is distinct from citizenship or domicile. A person may be a citizen of India but still be treated as a non-resident for income tax purposes if the conditions specified in the Act are not satisfied.

This article provides a comprehensive overview of Section 6 of the Income-tax Act, 2025 and explains the key rules governing the determination of residential status.

Meaning of Residential Status

Section 6 provides the framework for determining the residential status of a person in India for a particular tax year. The residential status must be determined separately for each tax year, since the number of days of stay and other conditions may change from year to year.

The residential status broadly classifies persons into the following categories:

- Resident

- Resident but Not Ordinarily Resident (RNOR)

- Non-Resident (NR)

The classification determines the extent to which income will be taxable in India.

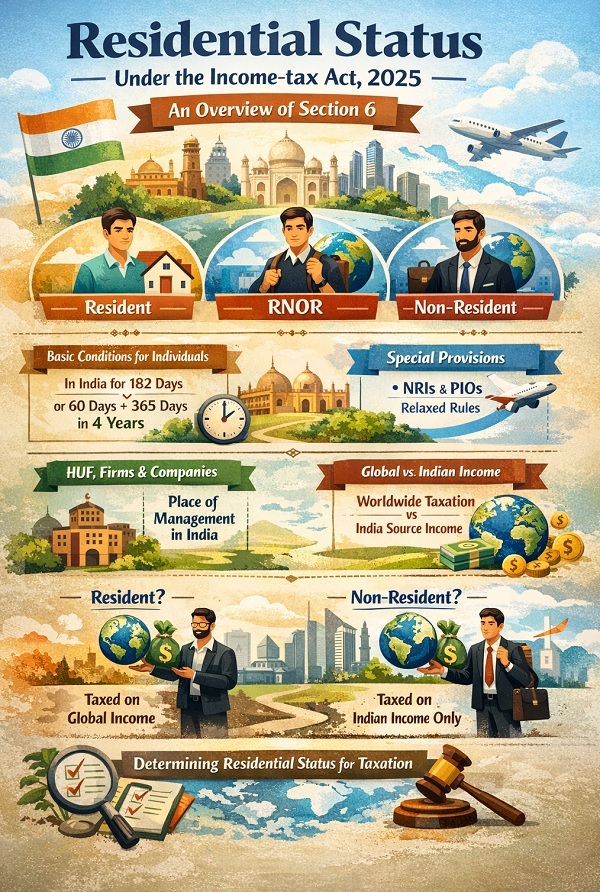

Residential Status of Individuals

An individual will be treated as resident in India if any of the following conditions are satisfied during the relevant tax year:

Basic Conditions

An individual is resident in India if:

1. He is in India for 182 days or more during the relevant tax year; or

2. He is in India for 60 days or more during the tax year and 365 days or more during the four preceding tax years.

3. If none of the above conditions are satisfied, the individual will be treated as a Non-Resident.

Special Provisions for Indian Citizens and Persons of Indian Origin

Certain special provisions apply in the case of:

- Indian citizens leaving India for employment outside India

- Indian citizens or Persons of Indian Origin visiting India

In such cases, the threshold of 60 days is substituted with 182 days, thereby granting relaxation in determining residential status.

These provisions are intended to provide relief to individuals who are temporarily visiting India or leaving India for employment purposes.

Resident but Not Ordinarily Resident (RNOR)

Even if an individual qualifies as a resident, he may still be categorized as Resident but Not Ordinarily Resident (RNOR) if certain additional conditions are not satisfied.

Generally, an individual will be treated as RNOR if:

- He has been a non-resident in India in a specified number of preceding tax years; or

- His total stay in India during preceding years does not exceed the prescribed limits.

The RNOR category provides a transitional status between resident and non-resident, and certain foreign incomes may remain outside the scope of Indian taxation.

Residential Status of Other Persons

Section 6 also prescribes rules for determining residential status of entities other than individuals.

Hindu Undivided Family (HUF), Firm or Association of Persons

A HUF, firm or association of persons is treated as resident in India if the control and management of its affairs is situated wholly or partly in India during the relevant tax year.

If the control and management is situated wholly outside India, the entity will be treated as non-resident.

Residential Status of Companies

A company is treated as resident in India if:

- It is an Indian company, or

- Its place of effective management (POEM) during the tax year is in India.

The concept of POEM refers to the place where key management and commercial decisions necessary for the conduct of business as a whole are, in substance, made.

Importance of Determining Residential Status

Determining residential status is crucial because it determines the scope of total income taxable in India.

Broadly:

- Residents are taxed on their global income.

- Non-Residents are taxed only on income received or deemed to be received in India or accruing or arising in India.

- RNORs are taxed in a limited manner, similar to non-residents for certain foreign incomes.

Therefore, correct determination of residential status is the first step in computing total taxable income.

Practical Significance for Taxpayers

Understanding residential status is particularly important for:

- Non-Resident Indians (NRIs)

- Individuals working abroad

- Foreign companies operating in India

- Global businesses and expatriates

Incorrect classification may lead to incorrect taxation, non-compliance or litigation.

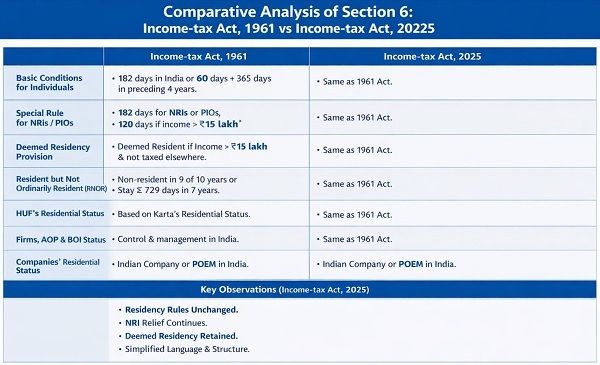

Comparative Analysis

For the benefit of readers and professionals, a comparative summary of the provisions relating to residential status under the Income-tax Act, 1961 and the Income-tax Act, 2025 has also been provided separately to highlight the similarities, structural changes and key differences between the two legislations.

Conclusion

Section 6 of the Income-tax Act, 2025 continues to play a pivotal role in determining the residential status of taxpayers in India. The residential status directly affects the scope of income taxable in India and therefore must be determined carefully for every tax year.

Taxpayers with cross-border presence, frequent travel, or international business operations must evaluate the number of days of stay in India and the control and management structure of their entities to ensure correct determination of residential status.

Proper understanding and application of Section 6 will help taxpayers remain compliant and avoid unnecessary tax disputes.

******

Author’s Note: The views expressed are personal and based on the provisions of the Income-tax Act.

Author Bio