Case Law Details

Sri Channabasaveshwara Swamy Rural Education Society Vs ITO (ITAT Bangalore)

ITAT Bangalore held that no computation of fee u/s. 234E of the Act for delayed filing of return of TDS while processing a return of TDS u/s. 234E of the Act could have been made for tax deducted at source for the assessment years prior to 1.6.2015.

Facts- The assessee is a Trust and is running an educational Institute. An order has been passed U/s 200A of the act, while processing the TDS returns, by levying fees U/s 234E of the Act and raising a demand.

Vide the present appeal, the only issue raised by the assessee is in respect of levy of interest u/s. 234E for belated filing of TDS returns.

Conclusion- Hon’ble Karnataka High Court in the case of Fatehraj Singhvi v. UOI has held that amendment made u/s. 200A of the Income Tax Act providing that fee u/s. 234E of the Act could be computed at the time of processing of return and issue of intimation has come into effect only from 1.6.2015 and had only prospective effect and therefore, no computation of fee u/s. 234E of the Act for delayed filing of return of TDS while processing a return of TDS u/s. 234E of the Act could have been made for tax deducted at source for the assessment years prior to 1.6.2015. Held that the interest u/s. 234E cannot be sustained.

FULL TEXT OF THE ORDER OF ITAT BANGALORE

Present appeals arises out of the following impugned orders passed by the NFAC, Delhi.

| Appeal No. | Assessment Year | Date of passing of the NFAC Order |

| ITA No. 582/Bang/2023 | 2013-14 | 26.08.2021 |

| ITA No. 583/Bang/2023 | 2013-14 | 30.08.2021 |

| ITA No. 584/Bang/2023 | 2013-14 | 30.09.2021 |

| ITA No. 585/Bang/2023 | 2013-14 | 30.09.2021 |

| ITA No. 586/Bang/2023 | 2014-15 | 30.08.2021 |

| ITA No. 587/Bang/2023 | 2014-15 | 30.08.2021 |

| ITA No. 588/Bang/2023 | 2014-15 | 25.08.2021 |

| ITA No. 589/Bang/2023 | 2014-15 | 30.08.2021 |

| ITA No. 590/Bang/2023 | 2014-15 | 30.09.2021 |

| ITA No. 591/Bang/2023 | 2014-15 | 30.08.2021 |

| ITA No. 592/Bang/2023 | 2014-15 | 30.08.2021 |

2. It has been submitted by the Ld.AR that in all the above appeals, the only issue raised by assessee is in respect of levy of interest u/s. 234E for belated filing of TDS returns. However he submitted that due to certain unavoidable circumstances, appeals were filed before this Tribunal with a total delay of 649 days. The Ld.AR submitted that on excluding the period that was contributable to covid pandemic, the effective number of delay would be 438 days. The assessee is a Trust and is running an educational Institute. An order has been passed U/s- 200A of the act, while processing the TDS returns, by levying fees U/s 234E of the Act and raising a demand. The assessee was subsequently informed regarding the decision of Hon’ble Karnataka High Court holding that the orders passed upto 01/06/2015, i.e. the date of amendment to section 200A, for the inclusion of the clause “c”, the adjustments were without authority.

3. The Ld.AR submitted that, the assessee on a bonafide belief that the assessing officer would make necessary corrections and reduce the demands raised, did not prefer an appeal. Thereafter, upon being informed by the Ld.AO that unless the demands were set aside by a judicial order in the assessee’s individual case, he was powerless to reduce the demand. Thereafter the assessee preferred an appeal before the Ld. CIT(A), to delete the addition, with such delay.

4. An order under section u/s 250 of the Income Tax Act, 1961 for the Assessment year 2013-14 was passed on 30/08/2021 by the Ld. CIT(A), National Faceless Appeal Centre, New Delhi and received by the appellant, presumably on 31/08/2021. The Ld. CIT(A) has dismissed the appeal.

5. The Ld.AR submitted that on account of the disruption of the normal business during the pandemic, the appellate order served online, was not brought to the attention of the management, considering the fact that the offices of the assessee were closed for a long time and the staff were also working from home. In view of this, the management of the assessee, were not aware of the passing of the above appellate order.

He submitted that, the fact of the passing of the impugned orders came to the knowledge of the management for the first time when the Ld.AO in or about June 2023, while seeking recovery of demand.

6. It is submitted that, the assessee thereafter approached the counsel for advice, considering the fact that the management was ignorant of the fact that the Ld. CIT(A) orders were passed much earlier and also whether an appeal could be filed with a delay, before this Tribunal.

7. The counsel advised the assessee, that it had a good case on the merits of the matter and advised to prefer appeal before this Tribunal, by seeking a condonation of delay. Under such circumstances, the appeal against the orders of the Ld. CIT(A) were filed before this Tribunal within 60 days from the date of service, i.e. 30/10/2021.

8. The Ld.AR submitted that during the relevant period Hon’ble Supreme Court had extended the period of limitation upto 29.05.2022 and therefore the delay in filing the present appeals has to be computed from 29.05.2022. The Ld.AR submitted that the present appeals has been filed before this Tribunal on 10.08.2023 thereby causing a net effective delay of 438 days. The Ld.AR submitted that this Tribunal raised a defect, stating that the delay was 649 days.

9. It is submitted that the delay was required to be reduced upto 29/05/2022, thus the delay in filing the appeal would stand reduced to 438 days.

10. He thus humbly prayed that this Tribunal may take a lenient and compassionate approach and condone the delay of 438 days in filing the present appeal against the orders of the Ld. CIT(A) passed under section 250 of the Act and hear the same on merits for the advancement of substantial cause of justice.

11. He also relied on the decision of Hon’ble Apex Court in the case of COLLECTOR, LAND ACQUISITION Vs MST. KATIJI AND OTHERS reported in (1987) 167 ITR 471, in the case of CONCORD OF INDIA INSURANCE CO LTD Vs SMT. NIRMALA DEVI AND OTHERS reported in 118 ITR 507 and decision of Hon’ble Supreme Court in the case of M/S. MELA RAM & SONS Vs CIT (PUNJAB) reported in 29 ITR 607. He also relied on the decision of recent judgment of Hon’ble Supreme Court in case of CIT Vs. WEST BENGAL INFRASTRUCTURE DEVELOPMENTFINANCE CORP, where Hon’ble Supreme Court held that delay should be condoned and matters to be heard on merits, when the stakes involved are high.

12. The Ld. DR though objected to the condonation of delay vehemently could not bring out anything on record to establish any malafide on behalf of the assessee in causing such delay to file the present appeals before this

13. On merits of the case, the Ld. DR submitted that the issue has not been considered by the Ld. CIT(A) who dismissed the appeals in limine by not condoning the delay caused in filing the appeals before the first appellate authority. However, he admitted to the fact that the merits of the case is covered by the decision of Hon’ble Karnataka High Court in case of Fatehraj Singhvi v. UOI reported in [2016] 73 taxmann.com 252. However he submitted that the revenue preferred SLP before the Hon’ble Supreme Court against the decision of Hon’ble Karnataka High Court and that he relied on the orders passed by the authorities below.

We have perused the submissions advanced by both sides in the light of records placed before us.

14. On merit, the issue is in favour of assessee as per the ratio of Hon’ble Karnataka High Court in case of Fatehraj Singhvi v. UOI (supra).

15. But there is a technical defect in the appeal as in all the appeals before us are not filed within the period of limitation. The assessee has filed an affidavit establishing the cause for the inability to file the present appeals. Revenue has not filed any counter affidavit denying the averments made by the assessee in the affidavit.

16. The Ld. DR submitted that there was inordinate delay of 438 days and the reason given by the assessee for filing the appeal belatedly cannot be considered as bona fide. It was submitted that the assessee was very negligent in its action and it could have been vigilant to avoid delay in filing the appeal before the Tribunal. Therefore, he submitted that the delay cannot be condoned in this case. According to the Ld. DR in this case, the assessee was sleeping over the matter and not keen to take remedial measures against the order of the CIT(A). Hence, the appeal is to be dismissed in limine.

17. Admittedly there is a delay of 438 days in filing the present appeals before this Hon’ble Supreme Court in case of N. Balakrishnan vs. M. Krishnamurthy reported in AIR 1998 SC 3222 in a similar circumstances, held that when substantial justice and technical considerations are pitted against each other, cause of substantial justice deserves to be preferred, for the other side cannot claim to have vested right in injustice being done because of a non- deliberate delay.

18. The decision of Hon’ble Mumbai Benches in the case of P. Trivedi vs. JCIT in ITA No. 5994/Mum/2010 dated 11/07/2012 held that delay in filing the appeal due to CA’s fault is bona fide and must be condoned and the delay of 438 days was condoned by observing as follows:

“5 After considering the rival submissions and carefully gone through the affidavit filed by the assessee as well as the affidavit of Shri Sunil Hirawat, CA of the assessee, we note that the facts of the case do not suggest that the assessee has acted in a malafide manner or the reasons explained is only a device to cover an ulterior purpose. It is settled proposition of law that the Court should take a lenient view on the matter of condonation of delay.

However, the explanation and the reason for delay must be bonafide and not merely a device to cover an ulterior purpose or an attempt to save limitation in an underhand way. The Court should be liberal in construing the sufficient cause and should lean in favour of such party. Whenever substantial Justice and technical considerations are opposed to each other, cause of substantial Justice has to be preferred.

5.1 In the case in hand, when the reasons explained by the assessee are not found as malafide or a device to cover up ulterior purpose, then a liberal approach has to be taken for considering the sufficiency of course. We are satisfied with the reasons explained by the assessee that due to bonafide mistake and inadvertence, the appeal could not be filed within the period of limitation. Accordingly, in the interest of Justice we condone the delay of 496 days in filing the present appeal.”

19. Hon’ble Madras High Court in case of Sreenivas Charitable Trust vs. DCIT reported in 280 ITR 357 observed that the expression “sufficient cause” should be interpreted to advance substantial justice. Therefore, advancement of substantial justice is the prime factor while considering the reasons for condoning the delay.

20. Further Hon’ble Apex Court in the case of Collector, Land Acquisition v. Mst. Katiji and Ors. (167 ITR 471) laid down six principles. For the purpose of convenience, the principles laid down by the Apex Court are reproduced hereunder:

“(1) Ordinarily, a litigant does not stand to benefit by lodging an appeal late

(2) Refusing to condone delay can result in a meritorious matter being thrown at the very threshold and cause of justice being defeated. As against this, when delay is condoned, the highest that can happen is that a cause would be decided on merits after hearing the parties.

(3) ‘Every day’s delay must be explained’ does not mean that a pedantic approach should be made. Why not every hour’s delay, every second’s delay? The doctrine must be applied in a rational, commonsense and pragmatic manner.

(4) When substantial justice and technical consideration are pitted against each other, the cause of substantial justice deserves to be preferred, for the other side cannot claim to have vested right in injustice being done because of a non- deliberate delay.

(5) There is no presumption that delay is occasioned deliberately, or on account of culpable negligence, or on account of mala fides. A litigant does not stand to benefit by resorting to delay. In fact, he runs a serious risk.

(6) It must be grasped that the judiciary is respected not on account of its power to legalise injustice on technical grounds but because it is capable of removing injustice and is expected to do so.”

21. Thus from the above decisions, when substantial justice and technical consideration are pitted against each other, the cause of substantial justice deserves to be preferred, for the other side cannot claim to have vested right for injustice being done because of nondeliberate delay.

22. In the case on hand, the issue on merit is regarding levy of interest u/s. 234E in the orders passed by the Ld.AO prior to 01.06.2015 which is covered in favour of assessee by the decision of Hon’ble Karnataka High Court. Therefore, we have to prefer substantial justice rather than technicality in deciding the issue. As observed by Hon’ble Apex Court, referred to hereinabove if the application of the assessee for condoning the delay is rejected, it would amount to legalise injustice on technical ground, when the Tribunal is capable of removing injustice and to do justice. Therefore, in our opinion, in the present facts by preferring the substantial justice, the delay of 438 days deserves to be condoned.

23. The next question may arise whether 438 days was excessive or inordinate. In our opinion, there is no question of any excessive or inordinate when the reason stated by the assessee was a reasonable cause for not filing the appeal. We have to see the cause for the delay. When there was a reasonable cause, the period of delay may not be relevant factor. Hon’ble Madras High Court in the case of CIT v. K.S.P. Shanmugavel Nadai and Ors. reported in 153 ITR 596 considered the delay of condonation and held that there was sufficient and reasonable cause on the part of the assessee for not filing the appeal within the period of limitation. Accordingly, the Hon’ble Madras High Court condoned nearly 21 years of delay in filing the appeal.

24. Further Hon’ble Madras High Court in the case of Sreenivas Charitable Trust (supra) held that no hard and fast rule can be laid down in the matter of condonation of delay and the Court should adopt a pragmatic approach and the Court should exercise their discretion on the facts of each case keeping in mind that in construing the expression “sufficient cause” the principle of advancing substantial justice is of prime importance and the expression “sufficient cause” should receive a liberal construction.

In the present facts of the case, the sufficient cause has been made out by the assessee in the affidavits substantiating the delay in filing the present appeals before this Tribunal.

In view of the above, we condone the delay of 438 days in filing the present appeals and admit the same for adjudication on merits.

Accordingly, the delay caused in filing all the above appeals before this Tribunal stands condoned.

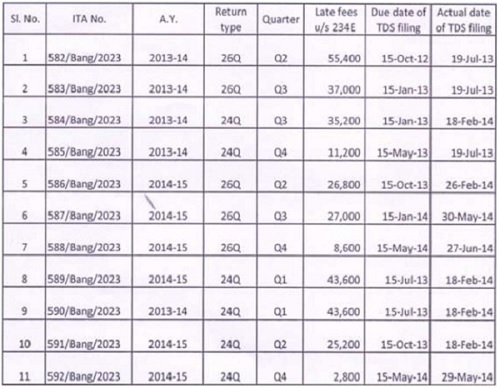

25. On merits of the case, we have perused the submissions advanced by both sides in the light of records placed before us. We note that CPC levied 234E interest for belated filing of the Quarterly TDS return by the assessee. The details are as under:

26. Clause (c) to (f) of section 200A(1) reproduced hereinabove was substituted by the Finance Act, 2015 w.e.f. 1.6.2015. The assessee contended that AO could levy fee u/s.234E of the Act while processing a return of TDS filed u/s.200(3) of the Act only by virtue of the provisions of Sec.200A(1)(c), (d) & (f) of the Act and those provisions came into force only from 1.6.2015 and therefore the authority issuing intimation u/s. 200A of the Act while processing return of TDS filed u/s.200(3) of the Act, could not levy fee u/s. 234E of the Act in respect of statement of TDS filed prior to 1.6.2015. The assessee, thus, challenged the validity of charging of fee u/s. 234E of the Act. The assessee relied on the decision of the Hon’ble High Court of Karnataka in the case of Fatehraj Singhvi v. UOI [2016] 73 taxmann.com 252 wherein the Hon’ble Karnataka High Court held that amendment made u/s. 200A providing that fee u/s. 234E of the Act could be computed at the time of processing of return and issue of intimation has come into effect only from 1.6.2015 and had only prospective effect and therefore, no computation of fee u/s.234E of the Act for delayed filing of return of TDS while processing a return of TDS u/s.234E of the Act could have been made for tax deducted at source for the assessment years prior to 1.6.2015.

27. Coordinate Bench of this Tribunal in case of Mindlogicx Infratec Ltd. vs. ACIT in ITA Nos. 462 to 483/Bang/2022 by order dated 19/07/2022 for A.Ys. 2013-14 to 2015-16 observed and held as under:

“13. It is not in dispute that if the ratio laid down by the Hon’ble Karnataka High Court in the case of Fateeraj Singhvi (supra) if applied then the levy of interest u/s.234-E of the Act would be illegal for returns of TDS in respect of the period prior to 1.6.2015. The present appeals of the assessee relate to TDS returns filed prior to 1.6.2015. The decision of the Hon’ble Karnataka High Court in the case of Fateeraj Singhvi (supra)was rendered on 26.8.2016. As rightly contended by the learned Counsel for the assessee, there is no ambiguity in the non applicability of the provisions of section 200A of the Act for the period prior to 01.06.2015 as interpreted by the Hon’ble Karnataka High Court in the case of Fateeraj Singhvi (supra). Therefore the issue before the AO in the application under section 154 of the Act cannot be said to be a debatable issue on which two views are possible. It cannot also be said that the mistake is not obvious and patent. The law is well settled that the decision of the Jurisdictional High Court is binding on the authorities functioning under its jurisdiction. The AO as well as the CIT(A) ought to have allowed the application of the assessee under section 154 of the Act by following law laid down by the Hon’ble Karnataka High Court in the case of Fateeraj Singhvi (supra).”

Respectfully following the above, all the appeals filed by the assessee are allowed and the interest u/s. 234E as tabulated hereinabove cannot be sustained.

In the result, all the appeals filed by the assessee stands allowed.

Order pronounced in the open court on 26th October, 2023.