1) INTRODUCTION

Hon’ble PM launched Transparent Taxation Scheme on 13th August 2020 in which Income-tax Assessments through electronic mode was made mandatory. The move was made to reduce interaction between Income-tax Officers and Assessee as a result of which corruption will be reduced to greater extent. CBDT laid down procedure, structure working background, roles and responsibilities of Income-tax Officers and Units engaged in Faceless Assessment.

2) STRUCTURE OF INCOME-TAX AUTHORITY

CBDT has set up following units/centre for smooth conduct of e-proceedings and has specified their specific jurisdiction, roles and responsibilities.

3) ROLE OF DIFFERENT AUTHORITY

| NeAC |

|

| ReAC |

|

| Assessment Unit |

|

| Verification Unit |

|

| Technical Unit |

|

| Review Unit |

|

4) HEARING THROUGH VIDEO-CONFERENCING

5) FACELESS ASSESSMENT PROCEDURE

5) FACELESS ASSESSMENT PROCEDURE

1. NeAC Shall serve notice to assessee.

2. Assessee may reply within 15 days of receipt of notice.

3. NeAC shall assign case to specific AU in any one ReAC through automated allocation system.

4. AU may request to NeAC for

5. NeAC shall issue notice to assessee and assign request to VU and TU. After receiving documents from assessee and reports from VU and TU, NeAC shall transfer the same to AU.

6. If assessee fails to comply with notice, then NeAC shall serve notice u/s 144 as to why assessment should not be completed to best of its judgement.

7. Assesee shall within the time frame file reply to NeAC.

8. If assessee fails to file response than-

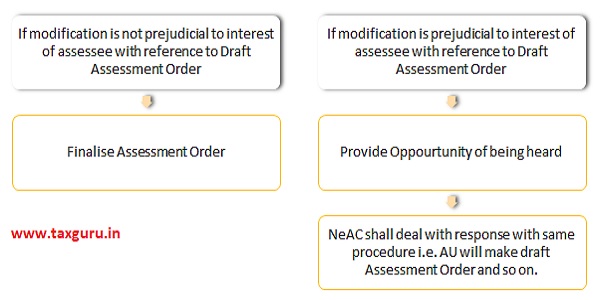

9. NeAC shall examine draft assessment order as per Risk Management strategy and automation examination tool where it may decide to-

10. The RU shall conduct review of Draft Assessment Order and may decide to-

11. NeAC shall-

12. Where SCN has been served to assessee he shall furnish reply within time frame. NeAC shall-

13. NeAC shall after receiving revised Draft Assessment Order-

14. NeAC shall after completion of assessment transfer all the electronic records to Assessing Officer having jurisdiction over the said case for-

- Imposition of Penalty

- Collection and recovery of demand

- Rectification of mistake

- Giving effect to appellate order

- Submission of remand report or any other report

- Representation of record before authorities

- Launch of Prosecution

15. NeAC may at any stage of assessment transfer the case to Assessing Officer having jurisdiction over such case.

6) OUR COMMENTS-

The Scheme was made applicable on pilot basis and total 58,322 cases were selected for A.Y.2018-19. It seems to be beneficial for assessee and business in long run. Implementation of procedure is a challenge as it requires lot of technical use and every person may not be equipped with the same but at the same time it will reduce corruption to great extend and the taxes will be used for nation building if Govt. goes the way it promises to go. Assessee has not option now other than to pay tax honestly or do tax planning with the help of expert to save tax legally.

*****

Disclaimer: The above comments do not constitute professional advice. The Author can be reached at divyaagrawal203@gmail.com or www.financialtreecompany.com . My name is CA Divya Agrawal and I am Practising Chartered Accountant. I also upload educational videos in You tube and name of my channel is FINANCIAL TREE COMPANY. My aim is to help people in improving their financial health by spreading knowledge and love. Stay Financially Fit and Healthy.