Computation of Threshold Limit for E-Way Bill Applicability – Inclusion of Tax, Freight & Insurance

This article explains how to compute the threshold limit for e-way bill applicability, focusing on what constitutes “consignment value” when an invoice contains multiple components such as GST, cess, exempt goods, freight, insurance, or other service charges. It reiterates that e-way bill provisions apply only to taxable movement of goods (subject to the prescribed state-wise threshold, e.g., ₹50,000 in Haryana) and do not apply to exempt/nil-rated/non-taxable goods or to services, since services do not involve physical movement in the manner contemplated for e-way bill generation. For taxable goods, the determining factor is the invoice value of goods, and importantly, GST and cess on such goods are included while checking whether the threshold is crossed. Through practical illustrations, the article demonstrates that where taxable value plus GST (and cess, if any) exceeds the limit, e-way bill becomes mandatory; otherwise, it is not required. A key nuance addressed is treatment of additional values reflected in the same invoice: value of exempt goods should be excluded while computing consignment value for e-way bill applicability. Further, where invoices include freight/transportation, insurance or other service charges, the service value and GST charged on such services should also be excluded, since e-way bill is meant for goods in movement and not for services. This position is supported by e-way bill FAQs clarifying that when an invoice covers both goods and services, consignment value and HSN details are to be determined only for goods, not services. The takeaway is that e-way bill threshold is tested using the value of taxable goods plus GST/cess thereon, excluding exempt goods and all service components.

1. Coverage of this article:

a. In this article, I am discussing the computation of the threshold limit for the applicability of the E-way bill.

b. The limit varies from state to state, but the most crucial point is determining which value should be considered- taxable value or value inclusive of GST component or services value to be considered or not.

2. Applicability of E-way bill on different types of transactions:

| S No | Particulars | Applicability of E-way bill |

| 1 | Taxable supply of goods | Yes, subject to some limit |

| 2 | Exempt supply of goods | No |

| 3 | Nil rated supply of goods | No |

| 4 | Non-taxable supply of goods | No |

| 5 | Taxable supply of services | No |

| 6 | Exempt supply of services | No |

| 7 | Nil rated supply of services | No |

| 8 | Non-taxable supply of services | No |

3. Non applicability on other than taxable goods:

a. In the case of exempt supply, there is no tax liability at the time of supply.

b. Therefore, there is no chances of tax evasion in case of exempt supplies. Hence, exempted goods are exempt from E-way bill.

4. Services exempt from E-way bill:

a. There is no movement in case of services via any mode of transportation. Hence, these are also exempt from the applicability of E-way bill.

b. E-way bill is required in case of movement & it happens in case of goods not in the case of service.

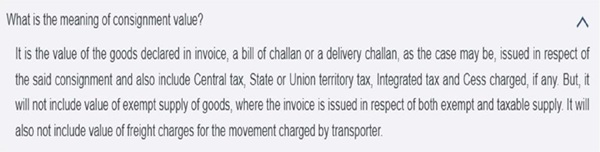

5. Determination of value:

a. Suppose, E-way bill is applicable if value exceeds the 50,000 (This limit applies in Haryana state).

b. We need to consider the invoice value for determining that whether it exceeds the prescribed limit or not. GST & cess both should be included in the limit.

c. But crucial point is whether we need to consider the service value or not. Which I have explained in this article.

6. Practical scenario 1:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 40,000 | |

| 2 | IGST | 18% | 7,200 |

| 3 | Invoice value | 47,200 |

a. In this case, the value inclusive of GST does not exceed 50,000.

b. Therefore, e-way bill is not applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

7. Practical scenario 2:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 45,000 | |

| 2 | IGST | 18% | 8,100 |

| 3 | Invoice value | 53,100 |

a. In this case, the value inclusive of GST exceeds 50,000.

b. Therefore, e-way bill is applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

8. Practical scenario 3:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 40,000 | |

| 2 | IGST | 18% | 7,200 |

| 3 | Cess | 20% | 8,000 |

| 4 | Invoice value | 55,200 |

a. In this case, the value inclusive of GST & cess exceeds 50,000.

b. Therefore, e-way bill is applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

d. GST & cess both should be included in the limit.

9. Practical scenario 4:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 40,000 | |

| 2 | IGST | 18% | 7,200 |

| 3 | Exempt goods | 5,000 | |

| 4 | Invoice value | 52,200 |

a. In this case, the value inclusive of GST & cess does not exceeds 50,000.

b. Therefore, e-way bill is not applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

d. If value of exempt supply includes in the invoice, then such value should not be considered. It should be excluded.

e. Therefore, value for the applicability of e-way bill is 47,200. Hence, e-way bill is not applicable in this case.

10. Practical scenario 5:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 45,000 | |

| 2 | IGST | 18% | 8,100 |

| 3 | Exempt goods | 5,000 | |

| 4 | Invoice value | 58,100 |

a. In this case, the value inclusive of GST & cess exceeds 50,000.

b. Therefore, e-way bill is applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

d. If value of exempt supply included in the invoice, then such value should not be considered. It should be excluded.

e. Therefore, value for the applicability of e-way bill is 53,100. Hence, e-way bill is applicable in this case.

11. Practical scenario 6:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 40,000 | |

| 2 | IGST | 18% | 7,200 |

| 3 | Transportation charges | 5,000 | |

| 4 | GST on Transportation charges | 18% | 900 |

| 5 | Invoice value | 53,100 |

a. In this case, the value inclusive of GST & cess does not exceed 50,000 because we need to exclude the value of service & applicable GST on that service.

b. Therefore, e-way bill is not applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

d. If value of service included in the invoice, then such value should not be considered. It should be excluded.

e. Therefore, value for the applicability of e-way bill is 47,200. Hence, e-way bill is not applicable in this case.

f. If services like freight & insurance included in the invoice then such value & GST levied on these services should also be excluded.

12. Practical scenario 7:

Suppose Mr Krishan supplying the goods to their customers:

| S No | Particulars | Rate | Amount |

| 1 | Taxable value of goods | 45,000 | |

| 2 | IGST | 18% | 8,100 |

| 3 | Transportation charges | 5,000 | |

| 4 | GST on Transportation charges | 18% | 900 |

| 5 | Invoice value | 59,000 |

a. In this case, the value inclusive of GST & cess exceeds 50,000.

b. Therefore, e-way bill is applicable in this case.

c. We need to check invoice value in case of taxable supply of goods.

d. If value of service included in the invoice, then such value should not be considered. It should be excluded.

e. Therefore, value for the applicability of e-way bill is 53,100. Hence, e-way bill is applicable in this case.

f. If services like freight & insurance included in the invoice then such value & GST levied on these services should also be excluded.

13. Note:

a. We need to check the value of taxable goods & GST levied upon it.

b. The value of exempt goods, all types of services & GST levied on taxable services should not be considered in the limit. These should be excluded.

14. As per E-way bill FAQs 1:

15. As per E-way bill FAQs 2:

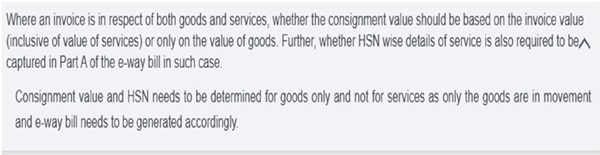

16. Question: Where an invoice is in respect of both goods and services, whether the consignment value should be based on the invoice value (inclusive of value of services) or only on the value of goods. Further, whether HSN wise details of service is also required to be captured in Part A of the e-way bill in such case.

Answer: Consignment value and HSN needs to be determined for goods only and not for services as only the goods are in movement and e-way bill needs to be generated accordingly.

If you have any queries, you can reach the author by email at caashishsingla878@gmail.com.

*****

Disclaimer: The views and opinions expressed in this article are those of the author. This article is intended for general information purposes only and does not constitute professional advice. Readers are strongly advised to consult a qualified professional for guidance specific to their individual situation before making any financial, legal, or tax-related decisions. The author shall not be held liable for any loss or damage of any kind incurred as a result of the use of this information or for any actions taken based on the content of this article.

Author Bio