Intimation for voluntary Payment of Tax, Interest and Penalty (Form No. DRC-3)

DRC-3 is an online form which is required to file by taxpayers to intimate payment of Tax, interest and penalty voluntary.

Mistake is common and natural for all who execute work and takes decisions. Under GST law statue has provided to disclose mistake and pay due tax, interest and penalty voluntary before or after issue of show cause notice (SCN) and intimate the payment to GST authority by filing form no. DRC-3 online on GST efiling portal.

Causes of payment of Tax, Interest and penalty

There are three causes for payment of Tax, Interest and penalty for which DRC-03 is required to file:-

1) Against bonafide mistake (U/s.73).

2) Against Willful Mistake or Fraud (U/s.74).

3) Other than 1 & 2 above.

Against bonafide mistake (U/s.73).

73. (1) Issuance of Show Cause Notice:-

Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded, or where input tax credit has been wrongly availed or utilized for any reason, other than the reason of fraud or any wilful-misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made,or who has wrongly availed or utilised input tax credit, requiring him to show cause as to why he should not pay the amount specified in the notice along with interest payable thereon under section 50 (presently 18% pa.a for delay period only) and a penalty leviable under the provisions of this Act or the rules made there under.

(2) The proper officer shall issue the notice under sub-section (1) at least three months prior to the time limit specified in sub-section (10) for issuance of order.

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of such statement shall be deemed to be service of notice on such person under sub-section (1), subject to the condition that the grounds relied upon for such tax periods other than those covered under sub-section (1) are the same as are mentioned in the earlier notice.

(5) Voluntary payment before SCN- No Penalty:

The person chargeable with tax may, before service of notice under sub-section (1) or, as the case may be, the statement under sub-section (3), pay the amount of tax along with interest payable thereon under section 50 on the basis of his own ascertainment of such tax or the tax as ascertained by the proper officer and inform the proper officer in writing of such payment.

(6) The proper officer, on receipt of such information, shall not serve any notice under sub-section (1) or, as the case may be, the statement under sub-section (3), in respect of the tax so paid or any penalty payable under the provisions of this Act or the rules made there under.

(7) Where the proper officer is of the opinion that the amount paid under sub-section (5) falls short of the amount actually payable, he shall proceed to issue the notice as provided for in sub-section (1) in respect of such amount which falls short of the amount actually payable.

(8) Voluntary Payment within 30 days after SCN- No Penalty:

Where any person chargeable with tax under sub-section (1) or sub-section (3) pays the said tax along with interest payable under section 50 within thirty days of issue of show cause notice, no penalty shall be payable and all proceedings in respect of the said notice shall be deemed to be concluded.

(9) Payment after order is passed- Penalty 10% or Rs.10K whichever is higher:-

The proper officer shall, after considering the representation, if any, made by person chargeable with tax, determine the amount of tax, interest and a penalty equivalent to ten per cent of tax or ten thousand rupees, whichever is higher, due from such person and issue an order.

(10) The proper officer shall issue the order under sub-section (9) within three years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilised relates to or within three years from the date of erroneous refund.

(11) Notwithstanding anything contained in sub-section (6) or sub-section (8), penalty under sub-section (9) shall be payable where any amount of self-assessed tax or any amount collected as tax has not been paid within a period of thirty days from the due date of payment of such tax.

Against Willful Mistake or Fraud (U/s.74)

74. (1) – Issuance of Show Cause Notice:

Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded or where input tax credit has been wrongly availed or utilized by reason of fraud, or any wilful-misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made, or who has wrongly availed or utilised input tax credit, requiring him to show cause as to why he should not pay the amount specified in the notice along with interest payable thereon under section 50 and a penalty equivalent to the tax specified in the notice.

(2) The proper officer shall issue the notice under sub-section (1) at least six months prior to the time limit specified in sub-section (10) for issuance of order.

(3) Where a notice has been issued for any period under sub-section (1), the proper officer may serve a statement, containing the details of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised for such periods other than those covered under sub-section (1), on the person chargeable with tax.

(4) The service of statement under sub-section (3) shall be deemed to be service of notice under sub-section (1) of section 73, subject to the condition that the grounds relied upon in the said statement, except the ground of fraud, or any wilful-misstatement or suppression of facts to evade tax, for periods other than those covered under sub-section (1) are the same as are mentioned in the earlier notice.

(5) Voluntary Payment before service of SCN-Penalty 15% of tax

The person chargeable with tax may, before service of notice under sub-section (1), pay the amount of tax along with interest payable under section 50 and a penalty equivalent to fifteen per cent. of such tax on the basis of his own ascertainment of such tax or the tax as ascertained by the proper officer and inform the proper officer in writing of such payment.

(6) The proper officer, on receipt of such information, shall not serve any notice under sub-section (1), in respect of the tax so paid or any penalty payable under the provisions of this Act or the rules made there under.

(7) Where the proper officer is of the opinion that the amount paid under sub-section (5) falls short of the amount actually payable, he shall proceed to issue the notice as provided for in sub-section (1) in respect of such amount which falls short of the amount actually payable.

(8) Voluntary payment within 30 days of SCN- Penalty 25% of Tax:-

Where any person chargeable with tax under sub-section (1) pays the said tax along with interest payable under section 50 and a penalty equivalent to twenty-five per cent of such tax within thirty days of issue of the notice, all proceedings in respect of the said notice shall be deemed to be concluded.

(9) The proper officer shall, after considering the representation, if any, made by the Person chargeable with tax, determine the amount of tax, interest and penalty due from such person and issue an order.

(10) The proper officer shall issue the order under sub-section (9) within a period of five years from the due date for furnishing of annual return for the financial year to which the tax not paid or short paid or input tax credit wrongly availed or utilized relates to or within five years from the date of erroneous refund.

(11) Payment within 30 days after order is passed- Penalty 50% of Tax

Where any person served with an order issued under sub-section (9) pays the tax along with interest payable thereon under section 50 and a penalty equivalent to fifty per cent. of such tax within thirty days of communication of the order, all proceedings in respect of the said notice shall be deemed to be concluded.

Explanation 1.—For the purposes of section 73 and this section,—

(i) the expression “all proceedings in respect of the said notice” shall not include proceedings under section 132; Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any willful misstatement or suppression of facts.

(ii) Where the notice under the same proceedings is issued to the main person liable to pay tax and some other persons, and such proceedings against the main person have been concluded under section 73 or section 74, the proceedings against all the persons liable to pay penalty under sections 122, 125, 129 and 130 are deemed to be concluded.

Explanation 2.––For the purposes of this Act, the expression “suppression” shall mean non-declaration of facts or information which a taxable person is required to declare in the return, statement, report or any other document furnished under this Act or the rules made there under, or failure to furnish any information on being asked for, in writing, by the proper officer.

At a Glance

| Particulars | Section:73 (Bonafide Mistake) | Section: 74 (Wilful Mistake or Fraud |

| Penalty Amount | Penalty Amount | |

| 1) Payment of Tax and Interest before issue of SCN | NIL U/s. 73(5) | 15% of evaded Tax U/s.74(5) |

| 2) Payment of Tax and Interest within 30 days of SCN | NIL U/s. 73 (8) | 25% of evaded Tax U/s.74(8) |

| 3) Payment of Tax and interest after issue of Order | 10% of Tax evaded or Rs.10K whichever is higher U/s. 73(9) | 50% of evaded Tax U/s. 74(11) |

Relevant Extract of Rule no. 142 of Central Goods and Services Tax Rules, 2017 is as given below-

142. Notice and order for demand of amounts payable under the Act.-(1) The proper officer shall serve, along with the

(a) notice under sub-section (1) of section 73 or sub-section (1) of section 74 or sub-section (2) of section 76, a summary thereof electronically in FORM GST DRC-01,

(b) Statement under sub-section (3) of section 73 or sub-section (3) of section 74, a summary thereof electronically in FORM GST DRC-02, specifying therein the details of the amount payable.

(2) Where, before the service of notice or statement, the person chargeable with tax makes payment of the tax and interest in accordance with the provisions of sub-section (5) of section 73 or, as the case may be, tax, interest and penalty in accordance with the provisions of sub-section (5) of section 74, he shall inform the proper officer of such payment in FORM GST DRC-03 and the proper officer shall issue an acknowledgement, accepting the payment made by the said person in FORM GST DRC-04.

(3) Where the person chargeable with tax makes payment of tax and interest under sub-section (8) of section 73 or, as the case may be, tax, interest and penalty under sub-section (8) of section 74 within thirty days of the service of a notice under sub-rule (1), he shall intimate the proper officer of such payment in FORM GST DRC-03 and the proper officer shall issue an order in FORM GST DRC-05 concluding the proceedings in respect of the said notice.

(4) The representation referred to in sub-section (9) of section 73 or sub-section (9) of section 74 or sub-section (3) of section 76 shall be in FORM GST DRC-06.

(5) A summary of the order issued under sub-section (9) of section 73 or sub-section (9) of section 74 or sub-section (3) of section 76 shall be uploaded electronically in FORM GST DRC-07, specifying therein the amount of tax, interest and penalty payable by the person chargeable with tax.

(6) The order referred to in sub-rule (5) shall be treated as the notice for recovery.

(7) Any rectification of the order, in accordance with the provisions of section 161, shall be made by the proper officer in FORM GST DRC-08.

Procedure for intimation of voluntary payment of GST in FORM GST DRC 03

FORM GST DRC 03: HOW TO APPLY

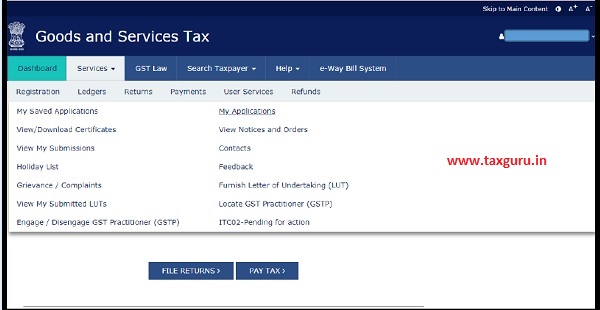

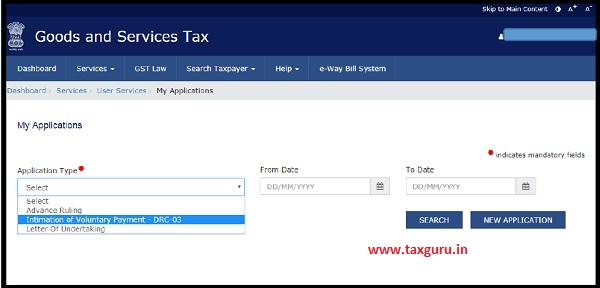

After login, go to and select Services->User Services->My Applications

In “Application Type*”, select “Intimation of Voluntary Payment- DRC 03” from drop-down and click on “NEW APPLICATION”

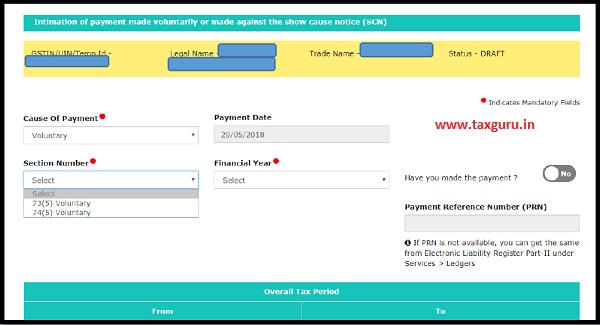

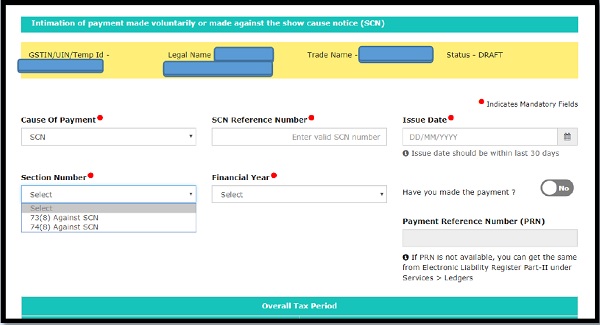

The following page will appear.

Here select “Cause of Payment*” from (a) Voluntary, (b) SCN and (c) Others. If Payment is made, then provide PRN.

Illustration 1: Voluntary-> Select appropriate section and FY.

Illustration 2: SCN->Select appropriate section and FY; provide SCN Reference No. and date (either system generated or manual)

Illustration 3: Others->Provide appropriate section and FY;

After filling details accordingly, go to the bottom of the screen to select period and Act and then Proceed to pay.

FAQ (Freequently Asked Questions)

1. What is the facility for Payment on Voluntary Basis?

Payment on Voluntary Basis is a facility given to tax payers to make payment u/s 73 or 74 of the CGST Act, 2017 within 30 days of issuance of Show Cause Notice (SCN). Payment could also be made by taxpayers before SCN is issued.

2. When can I make voluntary payment?

You can make voluntary payment before issue of notice u/s 73 or 74 of the CGST Act, 2017 or within 30 days of issue of show cause notice (SCN) under the said sections. You cannot make voluntary payment after 30 days of issue of SCN.

3. What are the pre-conditions to make voluntary payment?

The pre-conditions to make voluntary payment are:

a. In case, voluntary payment is made before issue of SCN

- Show Cause Notice under determination of tax should not have been issued.

- b. In case, voluntary payment is made after issue of SCN or statement

- 30 days’ time has not lapsed since SCN is issued.

4. Can I make partial payment against a liability declared voluntarily?

GST Portal does not allow for making partial payments against a liability declared voluntarily. The payment has to be made with reference to amount being demanded or already demanded in SCN.

Author Bio