Trade & Industry is in the panic situation, especially after Advance Ruling by Karnataka Advance Ruling Authority in the case of COLUMBIA ASIA HOSPITALS PRIVATE LIMITED where the question on which advance ruling was sought on below matter:

Whether the activities performed by the employees at the corporate office in the course of or in relation to employment such as accounting, other administrative and IT system maintenance for the units located in the other states as well i.e. distinct persons as per Section 25(4) of the Central Goods and Services Tax Act, 2017 (CGST Act) shall be treated as supply as per Entry 2 of Schedule I of the CGST Act or it shall not be treated as supply of services as per Entry 1 of Schedule III of the CGST Act?”

and the same was addressed and ruling was

The activities performed by the employees at the corporate office in the course of or in relation to employment such as accounting, other administrative and IT system maintenance for the units located in the other states as well i.e. distinct persons as per Section 25(4) of the Central Goods and Services Tax Act, 2017 (CGST Act) shall be treated as supply as per Entry 2 of Schedule I of the CGST Act.

The discussions & findings reported in Advance Ruling mainly based on the followings:

♦ The entry 2 of Schedule I, which deals with the activities that are to be treated as supplies even if made without consideration, reads as under:

2. Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business”

♦ The explanation given in Section 15 of CGST Act 2017, defines the “related persons” as under:

For the purposes of this Act,––

(a) persons shall be deemed to be “related persons” if––

i. such persons are officers or directors of one another’s businesses;

ii. such persons are legally recognised partners in business;

iii. such persons are employer and employee;

iv. any person directly or indirectly owns, controls or holds twenty-five per cent. or more of the outstanding voting stock or shares of both of them;

v. one of them directly or indirectly controls the other;

vi. both of them are directly or indirectly controlled by a third person;

vii. together they directly or indirectly control a third person; or

viii. they are members of the same family;

♦ Clause (c) of sub-section (1) of Section 7 which is related to the scope of supply clearly states as under:

“(1) For the purposes of this Act, the expression “supply” includes––

(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. . .

(b) . . .

(c) the activities specified in Schedule I, made or agreed to be made without a consideration; and

(d) . . .

Hence any activities made between related persons made or agreed to be made without a consideration shall be covered under supply of goods or services. The valuation of such services is to be done as per the provisions of section 15 of the Central Goods and Services Tax Act, 2017.

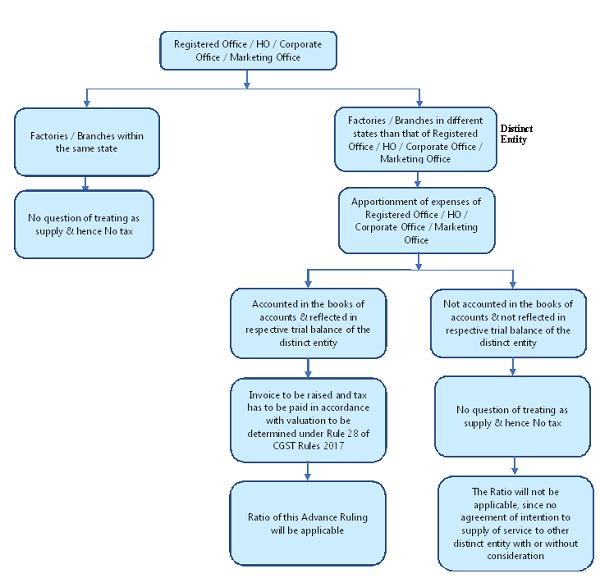

The premise of this advance ruling seems to be that corporate office is the service provider and is providing the services to its distinct entity and therefore this will tantamount to taxable supply and tax will have to be paid. The question arises, whether corporate office / registered office is performing their statutory role or role assigned to them and whether the same has to be considered as a supply, as if they are providing services to their other distinct entity.

Let us understand, the role of Registered Office / Corporate Office. In accordance with Section 12 of The Companies Act 2013, each company will have to declare the registered office for receiving and acknowledging the communication. Further, every company shall –

(a) paint or affix its name, and the address of its registered office, and keep the same painted or affixed, on the outside of every office or place in which its business is carried on, in a conspicuous position, in legible letters, and if the characters employed therefor are not those of the language or of one of the languages in general use in that locality, also in the characters of that language or of one of those languages;

(b) have its name engraved in legible characters on its seal;

(c) get its name, address of its registered office and the Corporate Identity Number along with telephone number, fax number, if any, e-mail and website addresses, if any, printed in all its business letters, billheads, letter papers and in all its notices and other official publications; and

(d) have its name printed on hundies, promissory notes, bills of exchange and such other documents as may be prescribed:

Books of Accounts have to be kept and retained at the Registered Office. Similarly Registered Office / HO / Corporate Office have to also perform the activities like accounting, auditing, etc. which is also part of statutory compliance. Basic duty of the Registered Office / HO / Corporate Office / Marketing Office is ensuring smooth functioning of the companies and being statutory compliant and therefore if they are employing certain employees or appointing service provider for such activities, the relevant cost cannot be considered as supply of services to the distinct entity of the same legal entity.

It seems that, integrated accounting system is envisaged in the GST Regime, which is not so. Apportionment of overheads at Registered Office / HO / Corporate Office / Marketing office is only for the purpose of determining of the profitability of the product cost / services, but it cannot be considered by any stretch of imagination as supply of service. Even the same is not envisaged in Ind AS or Accounting Standards. Allocation & apportionment to various cost centres cannot be said to be supply of services and consideration thereof. It is only for the purpose of calculation of cost of production, cost of sales of goods or services.

Let us really understand the principles which has been laid down in the said advance ruling.

Whether employee is of company or employer or its distinct entity?

In the said advance ruling, it has been considered, perhaps wrongly understood that, employer is different when employee is deputed at different distinct entity and it has been considered as follows :

- Entry No.1. of the Schedule III which is related to the activities which are to be treated neither as a supply of goods nor supply of services reads as under:

- “Services by an employee to the employer in the course of or in relation to his employment.”

- The services provided to the employer, i.e. the corporate office by the persons employed by the corporate office are in the nature of the employee-employer relationship. Further, since the corporate office and the units are distinct persons under the Act, there is no such relationship between the employees of one distinct entity with another distinct entity, at least as per the Goods and Service Tax Acts, even if they are belonging to the same legal entity.

- Further, the activities made between the related persons are treated as supplies and the valuation includes all costs, the employee cost also needs to be taken into consideration at the time of valuation of goods or services provided by one distinct entity to the other distinct entities.

- However, in our opinion, employees irrespective of deployed anywhere, either in corporate office or HO / Registered Office / Marketing Office / Factories / Branches, anywhere in India or abroad are the employees of the company and they have the transferrable clause in the appointment letter and therefore employees and employer relationship cannot be restricted to any location, but it is of the legal entity. Same principle has been adopted for the determination of threshold limit of applicability of taxes. The aggregate turnover is PAN India basis having turnover of the same PAN number and same treatment has to be considered for the employees and hence employees of corporate office providing services to the other distinct entity will also be considered as services provided by employees to the employer. Similarly, advances paid / gift paid by corporate office to the employee deployed at / working at place of distinct entity will also be covered under Entry No. 2 of Schedule 1 to the Section 7 of CGST Act 2017.

Author Bio

will the integrated accounting fulfill the place of supply gst provisions for inter state dealings if all transactions are accounted pan india at centralized corporate office state location only. courts may differ with advance ruling impracticable ruling for raising service invoice for inter state transactions within the company including stock transfers and share of corporate office expenses apportionment. accounting system under company act to be followed also be discussed

whether integrated accounting supports place of supply for inter state transactions assuming all transactions are accounted from corporate office.

GST IS CLASHING WITH THE CONCEPT OF ADVANTAGES AND ECONOMIES IN COST FOR DECENTRALIZATION STRUCTURE OF MANAGEMENT OF ORGANISATION-GOVT/PVT

FOR COMPLIANCE WITH LAW AND WITHIN THE SAME ENTITY/COMPANY DOCUMENTATION OF SERVICE INVOICES FOR INTER STATE DECENTRALISED CONTROL PRESENCE, KEEPING IN VOLUMES IT MAY NOT BE FEASIBLE TO CENTRALISE/ INTEGRATE THE CORPORATE FUNCTIONS OF ADMINSTRATION/HR/CS/COST & FINANCIAL ACCOUNTS/LEGAL/PURCHASE/MARKETING ETC SINCE THE COST OF CENTRALIZED OPERATIONS AND CONTROLS WILL BE WEAK SINCE THE DIFFERENT OBJECTIVES ARE SET FOR CENTRALIZED AND DECENTRALIZED FUNCTIONS. HOW THIS WILL APPLY TO GOVT. AND PUBLIC SECTOR ORGANISATIONS PAN INDIA BASIS INCLUDING BANKS ETC NEED SERIOUS REVIEW ALONG WITH SCREEN SHOTS FOR GST PORTAL TO DISCLOSE INTERNAL INVOICES. ACCOUNTING TREATMENT UNDER SCH III OF COMPANIES ACT FOR FINAL ACCOUNTS NEED REVIEW.

GST PORTAL IS NOT DESIGNED TO CAPTURE COMPLEXITIES OF CLASHING WITH OTHER STATUTES AND MANAGEMENT PRINCIPLES. GST CAN BE COMPLIES FOR WORK CONTRACT ONLY IF THE BOOKS OF ACCOUNT ARE KEPT ON CASH BASIS. GST IS LAW WITH PROBLEMS WITHOUT SOLUTIONS

KOI SHAQUE YAA SAAVAL????