Indirect Access and Input Credit Chains: Rethinking Liability and Benefit Flow under India’s GST Regime

The introduction of the Goods and Services Tax (GST) in India in 2017 heralded a structural shift in indirect taxation. By unifying state and central levies into a destination-based tax system with input tax credit (ITC) mechanisms, GST promised transparency, efficiency, and elimination of cascading taxes. Yet, the very design of GST—particularly the chain of ITC across multiple intermediaries—creates a phenomenon best described as “indirect access” to tax benefits and liabilities. Through intermediaries, entities may claim credits or assume liabilities without direct engagement with the underlying supplier, producing both opportunities for efficiency and risks of non-compliance, dispute, and litigation.

This article critically examines the legal and policy dimensions of indirect access in input credit chains, highlighting systemic vulnerabilities, jurisprudential interpretations, and the potential for reform. It argues that understanding the legal anatomy of credit flow is essential for investors, intermediaries, and policymakers to reconcile revenue integrity with commercial efficiency.

1. The Conceptual Framework of Indirect Access in GST

Under the GST framework, a registered person is entitled to input tax credit for taxes paid on purchases used in the course or furtherance of business. Sections 16–19 of the CGST Act, 2017codify eligibility, while Section 41 and the ITC rules detail credit flow, reversal, and adjustment mechanisms.

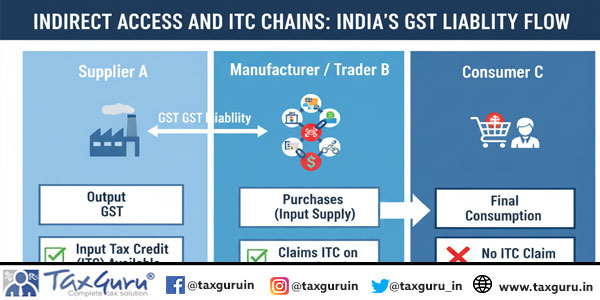

Indirect access arises when the ITC is not directly claimed from the supplier, but via an intermediary transaction. For example:

1. Manufacturer A supplies goods to Distributor B, who in turn sells to Retailer C.

2. Retailer C claims ITC on the GST charged by Distributor B.

3. The actual supplier, A, may have delivered goods at a lower or higher tax point than reflected in B’s invoice.

Here, C gains “indirect access” to A’s output credit through the intermediary B. Legally, this is permissible only if all statutory conditions are met—matching invoices, correct GSTIN filings, and timely GSTR compliance. However, discrepancies in reporting, delayed filing, or fraudulent claims create disputes, often magnified by multi-tiered supply chains.

The concept is not merely technical. By tracing credit flow through intermediaries, tax authorities and courts interpret Sections 16 and 41 to determine liability, reversal, and fraud detection. Hence, indirect access operates at the intersection of law, technology, and compliance.

II. Jurisprudential Interpretations of ITC Chains

Several judicial decisions illustrate the evolving understanding of indirect access:

1. State of Maharashtra v. Mahindra & Mahindra Ltd. (2020) – The Bombay High Court examined whether a distributor could claim ITC on a component purchased from a sub-vendor when the primary invoice did not reflect the component separately. The court emphasized substantive entitlement over procedural form, holding that as long as the transaction forms part of the registered person’s business activity, credit flow could be recognized, provided statutory safeguards were observed.

2. Bajaj Auto Ltd. v. Union of India (2021) – Here, the dispute concerned wrongly claimed ITC via intermediaries. The tribunal noted that Section 16(2)(c) prohibits ITC if the recipient has no possession of a proper tax invoice, but also highlighted digital matching mechanisms under GSTR 2B that enable indirect reconciliation.

These rulings reveal a judicial trend towards functional interpretation: the law recognizes indirect credit access when supported by adequate documentation, alignment of invoices, and verification of supplier compliance. At the same time, courts caution against excessive leniency that could encourage tax leakage via intermediary manipulation.

III. Systemic Challenges: Opacity and Disputes

Indirect access in ITC chains creates unique compliance challenges:

1. Mismatch and Fraud Risk: When multiple intermediaries exist, errors in reporting or deliberate under-reporting of output tax by upstream suppliers propagate downstream. For instance, if Distributor B under-reports tax liability, Retailer C’s ITC may exceed the actual GST remitted. This mismatch triggers recovery proceedings under Section 42–43 and interest liability under Section 50.

2. Cross-State Complexity: GST is a dual levy (CGST + SGST/UGST), and inter-state sales attract IGST, requiring credit flow reconciliation between jurisdictions. The indirect nature of access magnifies complexity: input credits may cross state boundaries via intermediaries, and failures in matching can delay claims or create disputes.

3. Technological Dependence: GST compliance relies on the electronic invoicing system (e-invoicing) and GSTR forms. Intermediary delays, system errors, or mismatches in e-way bills can inadvertently create denial of ITC, even when the transaction is bona fide. The indirect access chain thus introduces procedural liability that is technically indirect but substantively direct, a nuance often overlooked in practical compliance.

IV. Policy Implications: Balancing Revenue and Commerce

From a policy perspective, indirect access chains pose a dual problem:

1. Revenue Protection: Tax authorities must prevent ITC leakage due to unverified or fraudulent claims. Multi-layered supply chains complicate audits, as tracing actual tax remittance becomes laborious. Authorities often use matching engines and risk-based audits to reconcile upstream and downstream credits, but systemic gaps remain.

2. Business Efficiency: Overly restrictive interpretations of indirect access threaten the very purpose of GST: seamless credit flow. Investors and intermediaries rely on credit mechanisms to reduce cascading taxes, improve working capital efficiency, and encourage formalization. Procedural delays or denials of ITC disrupt cash flow, creating economic inefficiencies.

Reconciling these objectives requires legal clarity and administrative sophistication. Section 16(2)(aa) attempts to regulate claims through proper documentation, while Section 41 provides corrective mechanisms. Yet, gaps in intermediary accountability persist: should liability rest solely on the immediate supplier, or can downstream claimants be penalized for upstream failures?

V. Intermediary Liability and Anti-Abuse Doctrine

The indirect access concept also interacts with legal doctrines of anti-abuse:

1. GAAR-Analogous Principles: While GST does not have a formal GAAR, courts increasingly examine purposeful structuring of intermediary transactions aimed at maximizing ITC without substantive business justification. The Mahindra and Bajaj Auto rulings underscore the principle: indirect access is legitimate when aligned with bona fide business purposes, but artificial intermediaries designed solely to create ITC are susceptible to disallowance.

2. Digital Audit and Matching: Section 42–43 empowers authorities to provisionally assess ITC claims if discrepancies exist in supplier-reported tax. The matching mechanism effectively governs indirect access: downstream entities can claim credit only when upstream suppliers have discharged their obligations. This procedural control ensures equitable allocation of tax liability and constrains artificial credit chains.

3. Transparency and Compliance Obligations: Intermediaries are required to maintain records, issue valid invoices, and file returns in a timely manner. Judicial guidance emphasizes shared responsibility: while the recipient can claim ITC, non-compliance upstream triggers recovery, interest, and penalty. This legal architecture balances credit flow with risk management.

VI. Technological Integration: E-Invoicing and GSTR Reconciliation

Indirect access is increasingly managed through technology:

- E-invoicing: Standardized, digitally signed invoices create a real-time verification trail, reducing disputes over ITC claimed via intermediaries.

- GSTR 2B auto-population: Downstream recipients can reconcile their ITC claims against supplier filings. This system operationalizes the concept of indirect access with accountability, as ITC cannot be claimed if upstream filing is incomplete.

- AI-driven audits: Authorities are beginning to use data analytics to detect abnormal credit chains, including intermediary transactions with no underlying supply substance.

Legal interpretation now recognizes indirect access as contingent and conditional, rather than absolute entitlement: credit flows through the chain only when upstream compliance is intact.

VII. Towards Reform: Legal and Policy Recommendations

1. Clarifying Liability Distribution: Amendments to Sections 16–19 could explicitly define the intermediary threshold—when downstream claimants are responsible for upstream misreporting—to reduce litigation.

2. Strengthening Procedural Safeguards: Introduce automatic pre-verification of invoices in e-invoicing systems before ITC is credited, reducing disputes over indirect access.

3. Incentivizing Compliance: Provide limited safe harbor for downstream claimants who acted in good faith but were victims of upstream non-compliance. This approach aligns with investor confidence and reduces administrative burden.

4. Transparency Reporting: Require intermediaries to publish aggregate ITC disbursed via indirect access chains, enabling regulators and auditors to identify systemic risks without compromising confidentiality.

5. Judicial Interpretation: Encourage courts to adopt a functionalist, substance-over-form approach—recognizing indirect access when genuine business activity is present, while disallowing credit when intermediaries are used solely for tax arbitrage.

VIII Conclusion: Redefining Indirect Access in GST Law

The GST regime’s input credit architecture embodies both promise and complexity. Indirect access via intermediary chains allows businesses to maximize efficiency but creates latent compliance and litigation risks. Courts and authorities are moving toward functional, substance-based interpretations, balancing economic efficiency against revenue protection.

For legal professionals and investors, understanding the legal anatomy of credit flow is critical. Proper documentation, technological reconciliation, and awareness of judicial trends are essential to mitigate risk. From a policy perspective, formalizing intermediary obligations, integrating audit-friendly technologies, and clarifying downstream liability can preserve the integrity of the GST system while honoring its core purpose: a seamless, fair, and transparent indirect tax structure.

India’s GST jurisprudence is evolving, and indirect access is now a central lens through which courts, regulators, and practitioners must analyse credit entitlement, procedural compliance, and fiscal responsibility. Structuring intermediary transactions prudently, aligned with statutory intent and judicial guidance, ensures that ITC functions as intended—fueling commerce without enabling abuse.

References:

- Central Goods and Services Tax Act, 2017, §§16–19, 41, 42–43, 50

- CGST Rules, 2017, ITC reconciliation and reversal provisions

- State of Maharashtra v. Mahindra & Mahindra Ltd., Bombay HC, 2020

- GST Council Circulars on ITC, E-invoicing, and GSTR reconciliation

***

Author- Shweta Upadhyay | Founder & Partner | Solace Law Practice | Shweta@solacelawpractice.com