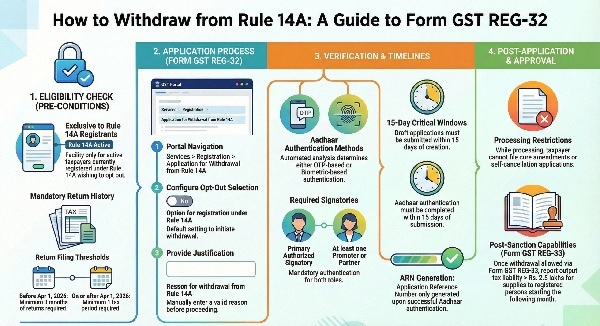

GSTN has introduced an online facility enabling eligible active taxpayers registered under Rule 14A of the CGST Rules to withdraw from the option by filing Form GST REG-32 on the GST Portal. The application can be accessed through Services → Registration → Application for Withdrawal from Rule 14A, and is available only to active Rule 14A registrants. Applicants must provide a reason for withdrawal and complete Aadhaar authentication of the Primary Authorised Signatory and at least one Promoter/Partner, through OTP or biometric verification. Filing is permitted only if prescribed return conditions are satisfied, including minimum return filing requirements and submission of all due returns. The draft application must be submitted within 15 days, and Aadhaar authentication completed within 15 days of submission, failing which ARN will not be generated. During processing, amendments and cancellation requests are restricted. Upon approval through Form GST REG-33, taxpayers can declare specified output tax liabilities from the succeeding month.

1. Who can apply

- Active Taxpayers who are registered under Rule 14A, may apply for OPT OUT in accordance with the provisions of the law.

2. How to apply on the GST Portal

- After login, navigate to:

- Services -> Registration -> Application for Withdrawal from Rule 14A

The link will be visible only if the taxpayer is registered under Rule 14A and is active.

- The field “Option for registration under Rule 14A” will be selected as “No” by default.

- Enter “Reason for withdrawal from Rule 14A”.

- Proceed to Aadhaar Authentication tab for Aadhaar Authentication of Primary Authorised Signatory and one Promoter/Partner.

3. Key pre-conditions

The registered person shall not be allowed to file Form GST REG-32 unless he has furnished,

(a) returns for a period of minimum three months, if Form GST REG-32 is filed before 1st April, 2026;

(b) returns for a period of minimum one tax period, if Form GST REG-32 is filed on or after 1st April, 2026; and

(c) all the returns due for the period from the effective date of registration till the date of filing of Form GST REG-32.

4. Aadhaar authentication

- Based on data analysis, the taxpayer will have to undergo either OTP based Aadhaar authentication or Biometric based Aadhaar Authentication.

- Authentication is required for:

- Primary Authorised Signatory (mandatory), and

- At least one Promoter/Partner (where applicable).

- ARN will be generated only after successful Aadhaar authentication.

5. Important timelines

- Draft application must be submitted within 15 days of creation.

- Aadhaar/Biometric authentication must be completed within 15 days from submission.

- If authentication is not completed within the prescribed time, ARN will not be generated.

6. Restrictions during processing

- While Form GST REG-32 is pending after submission, Taxpayer cannot file Core amendment, non-core amendment and Self-cancellation application.

7. Post-Sanction of Opt-Out

- The taxpayer who has received an order in Form GST REG-33 allowing withdrawal shall be able to furnish the details of output tax liability on supply of goods or services or both made to registered persons, exceeding the output tax liability of Rs.2.5 lakhs, from the first day of succeeding month in which the said order has been issued.