All about GST Refunds | A Reference Manual | Version 2.0 | 1st July 2020 is issed by DGTS – CBIC, Bengaluru & CGST (GST), Bengaluru Zone.

The information in this Reference Manual is intended only to provide a general overview and is not intended to be treated as legal advice or opinion. For greater details, you are requested to refer to the respective CGST/SGST/UTGST/IGST Acts, Rules, Notifications, Circulars & Orders issued from time to time.

Sabrina Cano, Superintendent

Principal Chief Commissioner’s Office

Central Tax (GST), Bengaluru Zone

Amitesh Bharat Singh

Additional Director General

Directorate General of Taxpayer Services –CBIC

Bengaluru

Download All about GST Refunds | A Reference Manual | Version 2.0 | 1st July 2020

Introduction

Goods and Services Tax (GST) in India, is a form of a Value–Added Tax (VAT). The overarching purpose of GST was to impose a broad-based tax on Consumption. It is a destination-based consumption tax.

The existing taxes before GST operated under the origin principle – the jurisdiction where the taxable activity took place levied and collected the tax. Origin based taxation created a scope at the sub-national level for a State to either export taxes onto other states or to undermine the companion State’s tax base by undercutting the tax rates charged elsewhere. Levying VAT on an origin basis, as it was happening in VAT before GST meant that taxes were being charged on the value that was added to a product in a different jurisdiction, at the rates charged by those jurisdictions which could well have been different from the rates in the destination states. The Firms producing in multiple jurisdictions then had an incentive to transfer price value-added into low tax jurisdictions, for instance by charging high internal prices for intrafirm sales out of them.

The change in GST to the destination principle places all firms competing in a given jurisdiction on an even footing. Thus, the tax paid on any taxable supply made under GST is determined by a set of rules to decide where this tax revenue will be destined to. These ground rules are contained in Sections 8 through 14 of the Integrated Goods and Services Tax (IGST) Act, 2017 that determine the nature and the place of consumption for every transaction of ‘supply’. All revenues in GST accrue to the jurisdiction where the supply is said to be consumed. There is a widespread consensus now that the destination principle, with revenue accruing to the country (and at a sub-national level – to the State/UT) where the final consumption occurs, is preferable to the origin principle from both a theoretical and practical standpoint.

The GST has unified the tax base at the Federal and the sub-national level in the Indian context. This has happened through uniformity of laws, tax rates, and the adoption of a single taxable event across both national and sub-national levels. The taxable event in Indian GST is that of ‘supply’ which is more broad-based than any single taxable event like manufacture or sale, in the taxes that it replaced. In GST, we have managed to achieve compliance symmetry (Identical compliance requirement for inter- and intra-provincial traders) – it was desirable to have such a compliance symmetry to have significant cost savings and efficiency at the firm level and thereby, at an aggregate level for the nation.

In general, the GST is imposed at every stage of the economic process and a deduction of taxes on purchases is allowed by all but the final consumer. The mechanism of input tax credits through the supply chain, except by the final consumer, ensures the neutrality of the tax, whatever the nature of the product, the structure of the distribution chain, and the means used for its delivery (e.g. retail stores, physical delivery, Internet downloads). There is a clear mechanism in place that allows for a credit of the tax levied on transactions between businesses. The system is based on tax collection in a staged process, with successive businesses entitled to deduct input tax on “capital goods”, “inputs” or “input services” and account for a tax on “outward supplies”. As a result of the staged payment system, GST thereby “flows through the businesses” to tax supplies made to final consumers. Following the destination principle, in GST exports are not subject to tax with a refund of input taxes (that is “zero-rated”) being made available, but imports are taxed (through the impost of an Integrated Goods and Services Tax -IGST) on the same basis and at the same rates as domestic supplies. These features give GST one of its main characteristics, that of neutrality.

This destination principle is sanctioned by the World Trade Organization (WTO) rules. In the predecessor GATT System that existed before the WTO, addenda to Article XVI of the 1947 General Agreement on Trade and Tariffs (GATT) excluded explicitly that such an exemption could be considered a subsidy: The exemption of an exported product from duties or taxes borne by the like product when destined for domestic consumption or the remission of such duties or taxes in amounts not over those which have accrued were not deemed to be a subsidy. Consequently, Article 6.4 of the 1947 General Agreement stipulated that: No product of the territory of any contracting party imported into the territory of any other contracting party shall be subject to … countervailing duty by reason of [such exemptions or refunds]. This principle was not changed within the framework of the WTO system, since Article I of the Uruguay Round Subsidies Agreement, which defines a subsidy, stipulates once again in footnote 1 that: the exemption of an exported product from duties or taxes borne by the like product when destined for domestic consumption or the remission of such duties or taxes in amounts not in excess of those which have accrued, shall not be deemed to be a subsidy1.

In GST law, the Integrated Goods and Service Tax (IGST) Act, 2017, in Chapter VII deals with the ZERO RATED SUPPLY. Section 16 of the IGST Act defines a “zero-rated supply” to mean any of the following supplies of goods or services or both, namely:-

a) Export of goods or services or both; or

b) Supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit.

The credit of input tax can also be availed for making zero-rated supplies subject to the provisions of sub-section (5) of section 17 of the Central Goods and Services Tax Act, 2017 (CGST Act). Under the provisions of section 54 of the Central Goods and Services Tax Act any person registered under GST and making zero-rated supply is eligible to claim a refund under either of the following options: –

a) He may supply goods or services or both under bond or Letter of Undertaking, without payment of integrated tax and claim refund of the unutilised input tax credit; or

b) He may supply goods or services or both, on payment of integrated tax and claim a refund of such tax paid on goods or services or both supplied.

More generally, the following kinds of Refunds are available to eligible taxpayers under GST:

i. A refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies,

ii. A Refund of tax on the supply of goods regarded as deemed exports,

iii. A refund of the unutilized input tax credit.

‘Supply’ in GST

In GST, the taxable event is the event of a “Supply”. In ordinary language, supply means make (something needed or wanted) available to someone; to provide. Supply could be an interstate supply or an intrastate one.

The GST is levied in the form of a Central Goods and Services Tax (CGST) and a State or Union Territory Goods and Services Tax (SGST or UTGST) on all intra-State supplies of goods or services or both, except on the supply of alcoholic liquor for human consumption. The value taken for the charge of the tax is determined under Section 15 of the CGST Act and the tax is calculated at such rates, not exceeding twenty percent, as may be notified by the Government on the recommendations of the Council. An Integrated Goods and Services Tax (IGST) is levied instead of a Central Goods and Services Tax and a State or Union Territory Goods and Services Tax whenever the supply happens to be an interstate one.

In terms of Section 7 of the CGST Act that deals with the “Scope of Supply’, “supply” includes all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business. Thus, the general tests for a transaction to be reckoned as a supply or not are two – the first being the Business Test (whether the supply is made in the course or furtherance of business) AND the Second is the Test of the Consideration for the particular supply concerned in the transaction that may have been made or agreed to be made. However, in GST law, the Business Test mentioned above does not apply to the situation of import of services for a consideration. Any Import of Services thus become liable to tax whether or not made in the course or furtherance of business. Besides, there is a set of activities specified in Schedule I to the CGST Act, made or agreed to be made without any consideration, that if engaged in have to be construed as being an instance of a ‘supply’.

Schedule II to the CGST Act contains a listing of activities or transactions that constitute a supply in the sense of the meaning assigned to the expression but are to be treated either as a supply of goods or supply of services to ease the matters relating to the determination of the place of supply and matters relating to the rate of tax attracted on the particular transactions.

Furthermore, Activities or transactions specified in Schedule III to the CGST Act; or such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council are to be treated neither as a supply of goods nor a supply of services.

Input Tax Credits in GST

Chapter V of the CGST Act deals with Input Tax Credit (ITC).

Section 16 of the CGST Act entitles every registered person to take credit of input tax charged on any supply (of goods or services or both) to him which are used or intended to be used in the course or furtherance of his business.

Credit is permitted to be taken on ‘capital goods’, ‘inputs’, and on ‘input services’. The entitlement to credit is subject to certain prescribed conditions and restrictions. The ITC is made available to the registered person as a credit in his electronic credit ledger. To take credit, the registered person should have a tax invoice or debit note (or any other prescribed taxpaying documents) issued by a GST registered supplier and he should also have received the goods or services or both on which the ITC is sought to be taken. Section 49 of the CGST Act deals with how the input tax credit is credited to the electronic credit ledger of the registered taxpayer.

The CGST law – Section 16 (2) (c) & (d) also entails that before the ITC is taken by the Recipient of either goods or services or both, the tax charged in respect of such input supplies should have been actually paid to the Government, either in cash or through utilization of input tax credit admissible in respect of the such a supply; and that the supplier making the input supplies furnish the return under section 39.

In terms of the 1st, and 2nd Provisos to Section 16(2)(c) of the CGST Act, where the goods against an invoice are received in lots or installments, the registered person is entitled to take credit upon receipt of the last lot or installment. Besides, it is also stipulated that the recipient of input supplies (either goods or services or both) should pay the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis- in case, the stipulated payments are not made in this time of 180 days an amount equal to the input tax credit availed by the recipient would be added to his output tax liability of the recipient, along with interest thereon.

The 3rd Proviso to Section 16(2) (c) of the CGST Act deals with the reverse charge situations and provides that the recipient of goods and services or both, is entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Section 16 (3) of the CGST Act disallows the registered person from claiming input tax credit on the tax component of the cost of capital goods and plant and machinery that has been claimed as depreciation on under the provisions of the Income-tax Act, 1961 (43 of 1961). Section 16 (4) permits input tax credit in respect of any invoice or debit note for the supply of goods or services or both but puts a timeline within which such a credit can be taken.

The amount of input tax credit is restricted to so much of the input tax as is attributable to the purposes of his business – in cases where the goods or services or both are used by the registered person partly for any business and partly for other purposes [Section 17(1) of the CGST Act] – this is a practice consistent with the laws and practices in many other tax jurisdictions outside India which follow GST/ VAT models. In cases where the goods or services or both are used by the registered person partly for effecting taxable supplies including zero-rated supplies and partly for effecting exempt supplies under the said Acts, the amount of credit is restricted to the input tax as can be attributed to the said taxable supplies including zero-rated supplies [Section 17(2) of the CGST Act]. The value of exempt supply can be worked out using [Section 17(3) of the CGST Act]. Section 17(4) of the CGST Act gives two options on the manner of taking ITC, either one of which may be exercised, to a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances.

Section 17(5) restricts the input tax credit from being available in respect of certain input supplies – like on certain classes of motor vehicles, vessels, and aircraft, on food and beverages, outdoor catering, beauty treatment, health services, cosmetic and plastic surgery, life insurance, etc. However, some of these exclusions are not absolute and there are specific situations in which ITC can be taken on some such supplies.

Section 18 of the CGST Act makes input tax credit available in respect of inputs and capital goods sent for a job-work, subject to observance of stipulated conditions.

Section 20 of the CGST Act deals with the manner of distribution of credit by an “Input Service Distributor”.

The framework of the input tax credit mechanism outlined above applies to all three taxes in GST – the central tax, the integrated tax, and the State Tax.

Exports in GST

In terms of Section 2 (5) of the IGST Act, “export of goods” with its grammatical variations and cognate expressions, means taking goods out of India to a place outside India. An “export of services” in terms of Section 2(6) of the IGST Act means the supply of any service when, –

(i) The supplier of service is located in India;

(ii) The recipient of service is located outside India

(iii) The place of supply of service is outside India

(iv) The payment for such service has been received by the supplier of service in convertible foreign exchange [or in Indian rupees wherever permitted by the Reserve Bank of India]; and

(v) The supplier of service and the recipient of service are not merely establishments of a distinct person

In GST certain establishments are treated as establishments of distinct persons where a person has –

(i) An establishment in India and any other establishment outside India;

(ii) An establishment in a State or Union territory and any other establishment outside that State or Union territory; or

(iii) An establishment in a State or Union territory and any other establishment registered within that State or Union territory.

The location of the supplier of service, the location of the recipient of service, and the place of supply of service are determinable in terms of Sections 2(15) and Section 2(14) of the IGST Act. In cases where the location of the supplier or location of the recipient is outside India, the place of supply of the concerned service can be determined with reference to provisions of Section 13 of the IGST Act.

Zero‐rated supplies under GST

Export of goods or services or both, and the supply of goods or services or both, to a Special Economic Zone developer or a Special Economic Zone unit – are zero-rated as per Section 16(1)(a) & (b) respectively of the IGST Act, 2017.

By zero-rating it is meant that the tax impact on the entire supply chain leading up to the particular transaction that is being ‘Zero Rated” is made tax free i.e. there is no burden of tax to be borne either on the inputs leading up to the particular outward supply or on the outward supply itself. [In terms of Section 2 (83) of the CGST Act 2017, “outward supply” in relation to a taxable person, means a supply of goods or services or both, whether by sale, transfer, barter, exchange, licence, rental, lease or disposal or any other mode, made or agreed to be made by such person in the course or furtherance of business.]

Zero- rating in GST implies the following: –

(i) The credit of input tax may be availed for making zero-rated supplies; notwithstanding that such supply may be an exempt supply (note: credit eligibility still needs to be checked with reference to terms of provisions of Chapter V of the CGST Act, 2017).

(ii) A registered person making zero rated supply shall be eligible to claim refund in accordance with the provisions of section 54 of the CGST Act under either of the following options, namely :-

(a) he may supply goods or services or both under bond or Letter of Undertaking, without payment of integrated tax and claim refund of unutilised input tax credit; or

(b) he may supply goods or services or both, on payment of integrated tax and claim refund of such tax paid on goods or services or both supplied.

The Zero- Rated situations can be contrasted with the other situation where a particular supply under the GST has been exempted from the charge of the tax – in the latter situation, it is only that the outward supply or the output that is exempted from tax, but the tax borne on all the inputs that may have gone into making this outward supply is not refunded. The essence of zero-rating is thus, to make Indian goods and services competitive in the international market by ensuring that domestic taxes do not get added as a cost in exports.

The objective of zero-rating of exports and supplies to SEZ/SEZ Developer is achieved through the provision contained in Section 16(3) of the IGST Act, 2017.

Refund in GST

When tax, interest, or any other amount is paid to the Government more than the liability incurred or accrued, then a refund situation arises. In terms of the explanation to Section 54 of the CGST Act, “refund” includes a refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies, or refund of tax on the supply of goods regarded as deemed exports, or refund of the unutilized input tax credit.

Statutory provisions relating to refunds in GST

Chapter XI of the CGST Act, 2017, in Sections 54 to 56 deal with refunds under GST. The procedure for claiming refunds is contained in Chapter X of the CGST Rules, 2017 under Rules 89 to 97A.

GST Council Resolution on permitting refunds without matching and without excluding the amount of provisionally accepted input tax credit

Since the functionality of furnishing of FORM GSTR‐2 and FORM GSTR‐3 remains unimplemented, it has been decided by the GST Council to sanction refund of provisionally accepted input tax credit. However, the applicants applying for refund must give an undertaking to the effect that the amount of refund sanctioned would be paid back to the Government with interest in case it is found subsequently that the requirements of clause (c) of sub-section (2) of section 16 read with sub-section (2) of section 42 of the CGST Act have not been complied with in respect of the amount refunded. This undertaking should be submitted electronically along with the refund claim

The concerned portion of the Minutes of 24th GST Council Meeting held on 16 December 2017 is reproduced below:

Agenda item 3:

Any other agenda item with the permission of the Chairperson

(i) Refund of provisionally accepted input tax credit

8. Introducing this agenda item, the Secretary stated that as no automated refund system had been operationalised as yet, the refund applications were being filed online and then the applicants would take a hard copy of the same to the jurisdictional officer for processing the refund claim manually, after which a single order would be passed. He stated that some officers in the field had raised a doubt that as per the law, refund could be given only if the inward and outward supplies were matched and tax was paid on the supply. He stated that as presently no matching was possible, it was proposed to take an undertaking as part of refund application itself that the amount of refund would be paid back to the Government in case it was subsequently found that the tax had not been paid on the supply as required under Section 16(2)(c) of the CGST Act/SGST Act or the inward and the outward supply involving the refund claim did not match (requirements under Sections 41 and 42 of CGST/SGST Act). He stated that it was proposed to allow following refunds (both provisional and final) without matching and without excluding the amount of provisionally accepted input tax credit: (i) Unutilised input tax credit in case of zero rated supplies (exports and supplies to SEZs) of goods or services or both; (ii) Unutilised input tax credit in case of inverted duty structure in case of goods (including supply of goods to merchant exporters); (iii) IGST paid on zero rated supplies (exports and supplies to SEZs) of goods or services or both; (iv) IGST or CGST/SGST/UTGST paid on deemed export of goods subject to furnishing an undertaking as part of refund application itself that the amount of refund would be paid back to the Government in case it is found subsequently that the requirement of Section 1 6(2)(c) read with Section 42 (2) of the CGST/SGSTAct have not been complied with. He stated that this relaxation was proposed by exercising the power conferred under Section 148 of the CGST/SGST Act regarding special procedure for certain processes.

8.1. The Hon’ble Minister from West Bengal strongly supported the proposal. He stated that since GSTR‐2 stood suspended, no matching of inward .and outward supply was possible, and therefore, it was a very good proposal to permit refund without matching. The Hon’ble Minister from Tamil Nadu had circulated a written speech in which it was mentioned that Section 148 of the CGST/SGST Act had no non‐obstante (“notwithstanding clause”) and hence, it needed to be examined whether the special process prescribed under Section 148 would over‐ride the substantive provision of Section 54(6) of the CGST/SGST Act which required that any claim for refund on account of zero rated supply of goods or services or both made by registered persons be refunded on a provisional basis to the extent of 90% of the total amount so claimed, excluding the amount of input tax credit provisionally accepted. In the written speech, he also pointed out that refund based on GSTR‐3B returns might lead to bogus claim of input tax credit by unscrupulous taxpayers taking advantage of non‐matching of input tax credit. He suggested to stipulate sufficient safeguards for the revenue as well as for the Departmental officers. In view of this, he recommended that the matter be examined in further detail as it involved substantial question of law. However, the Hon ‘ble Minister from Tamil Nadu did not express these apprehensions during the Council Meeting. No other Member expressed any reservation on the proposal. The Hon ‘ble Chairperson suggested that the proposal made by the Secretary could be approved. The Council approved the same.

9. for agenda item 3(i), the Council approved the following:

a. to allow following refunds (both provisional and final) without matching and without excluding the amount of provisionally accepted input tax credit: (i) Unutilised input tax credit in case of zero rated supplies (exports and supplies to SEZs) of goods or services or both; (ii) Unutilised input tax credit in case of inverted duty structure in case of goods (including supply of goods to merchant exporters); (iii) IGST paid on zero rated supplies (exports and supplies to SEZs) of goods or services or both; (iv) lGST or CGST/SGST/UTGST paid on deemed export of goods.

b. Such refund shall be given subject to furnishing an undertaking as part of refund application itself that the amount of refund would be paid back to the Government in case it is found subsequently that the requirement of Section 16(2)(c) read with Section 42 (2) of the CGST/SGST Act have not been complied with in respect of the amount refunded

Types of refund in GST

Refunds under GST are broadly categorized as follows:

(a) Refund of tax paid on supplies of goods or services or both

a. Refund of tax paid on export of good with payment of tax

b. Refund of tax paid on export of services with payment of tax

c. Refund of tax paid on supplies made to SEZ Unit/SEZ Developer with payment of tax

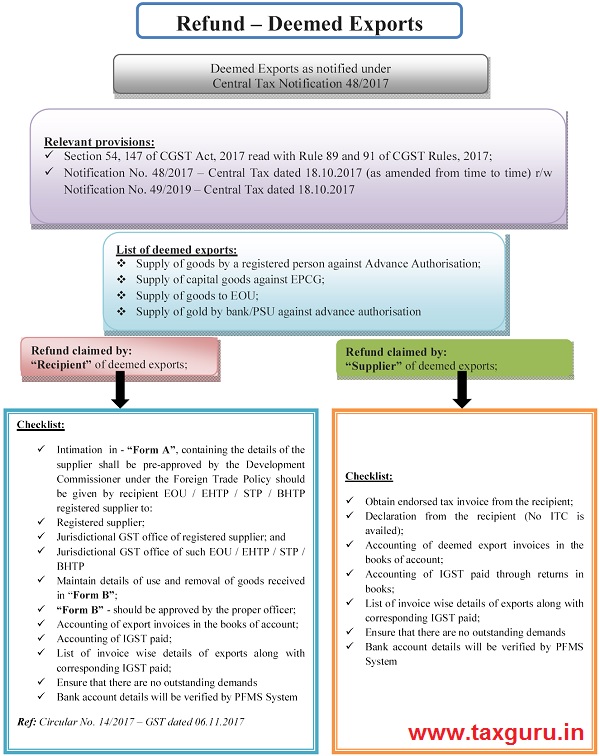

d. Refund to the supplier of tax paid on deemed export supplies.

e. Refund to the recipient of tax paid on deemed export supplies.

(b) Refund of unutilized ITC

a. Refund of unutilized input tax credit (ITC) on account of exports without payment of tax.

b. Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax.

c. Refund of unutilized ITC on account of accumulation due to an inverted tax structure.

(c) Refund of balance in electronic cash ledger

(d) Refund of advance tax deposited by Casual Taxpayer or Non-resident Taxpayer

(e) Refund of tax paid on supplies received by Embassies, Consulates, Agencies of UNO, etc.

(f) Others

a. Refund of excess payment of tax.

b. Refund of tax paid on an intra-State supply which is subsequently held to be inter-State supply and vice versa.

c. Refund on account of assessment/provisional assessment/appeal/any other order.

d. Refund on account of “any other” ground or reason.

Time limits to claim a refund in GST

The time limit for claiming a refund is two years from the relevant date. However, in terms of the Explanation to Section 54, the ‘relevant date’ or the reference date is different for different situations as indicated in the following table: –

Table 1

| S. No. | Refund event | Relevant Date |

| 1. | Goods exported out of India where the refund is in respect of the goods themselves or with respect of the inputs or input services used in such goods: | |

| (a) Goods are exported by sea or air | The date on which the ship or aircraft in which such goods are loaded, leaves India | |

| (b) Goods exported by land | The date on which such goods pass the frontier | |

| (c) Goods exported by post | Date of despatch of goods by the Post Office concerned to a place outside India | |

| 2. | Goods supplied as deemed exports | The date on which the return relating to such deemed exports is furnished |

| 3.

|

Export of services where the refund is in respect of the services themselves or in respect of the inputs or input services used in such services: | |

| (a) Where the supply of services has been completed before the receipt of payment | Date of receipt of payment in convertible foreign exchange | |

| (b) Where the payment for the services has been received in advance before the date of issue of invoice | Date of issue of invoice | |

| 4. | Refund arising out of a judgment, decree, order or direction of the Appellate Authority, Appellate Tribunal or any court | Date of communication of such judgment, decree, order or direction |

| 5 | Refund of unutilized Input Tax credit | The end of the financial year in which such claim for refund arises |

| 6 | Refund of tax paid provisionally | Date of adjustment of tax after the final assessment |

| 7 | Refund claimed by a person other than the supplier | Date of receipt of goods or services or both by such person |

| 8 | In any other case | Date of payment of tax |

Please Note:-

A refund application filed after correction of deficiency is treated as a fresh refund application, and such a rectified refund application, submitted after correction of deficiencies, will also have to be submitted within 2 years of the relevant date as defined in the explanation after sub-section (14) of section 54 of the CGST Act.

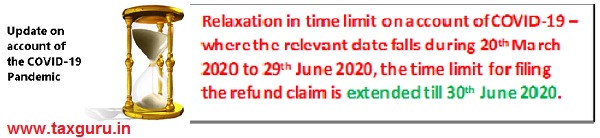

In wake of COVID pandemic, date further extended till 3 1.08.2020 for certain compliance under GST laws and till 30.09.2020 for certain compliance Customs, Central Excise and Service Tax Laws – https://www.cbic.gov.in/htdocs-cbec/home_links/tickers as of 30.6.2020 at 19:30 hours

The Refund Mechanism in GST

After the rollout of GST w.e.f. 1-7-2017, on account of the unavailability of electronic refund module on the common portal, a temporary mechanism had to be devised and implemented wherein applicants were required to file the refund application in FORM GST RFD‐01A on the common portal, take a print out of the same and submit it physically to the jurisdictional tax office along ith all supporting documents. Further processing of these refund applications, i.e. issuance of acknowledgment of the refund application, issuance of deficiency memo, the passing of provisional/final order, payment advice, etc., was also being done manually.

RULE 97A of the CGST Rules had enabled the Manual filing and processing of refund claims‐ It states that notwithstanding anything contained in CHAPTER X of the CGST Rules 2017, dealing with REFUND and with respect to any process or procedure prescribed for refunds, any reference to electronic filing of an application, intimation, reply, declaration, statement or electronic issuance of a notice, order or certificate on the common portal shall, in respect of that process or procedure, include manual filing of the said application, intimation, reply, declaration, statement or issuance of the said notice, order or certificate in the concerned Forms as appended were appended to the CGST rules.

To make the process of submission of the refund application electronic, Circular No. 79/53/2018-GST, dated 31-12-2018 was issued wherein it was specified that the refund application in FORM GST RFD‐01A, along with all supporting documents, is to be made electronically on the GST portal. However, various post submission stages of processing of the refund application continued to be manual.

The necessary capabilities for making the refund procedure fully electronic, in which all steps of submission and processing were undertaken electronically, was deployed on the common portal with effect from 26‐9‐2019 ‐ the refund from this date on is processed by a single tax authority, in contrast to the earlier treatment where the claim was processed for the State or the Central part by the concerned tax agency and processed by the disbursement was processed by the accounting departments of state and central individually.

The refund mechanism under GST is now fully automated. Barring the refund of IGST paid on the export of goods, the following types of refunds are dealt with under the provisions of Rule 89 of the CGST Rules.

With effect from 26‐9‐2019, the claim in respect of the following types of refund is now to be filed online on the GST Portal in Form GST RFD 01 and is processed electronically:

(a) Refund of unutilized input tax credit (ITC) on account of exports without payment of tax.

(b) Refund of tax paid on export of services with payment of tax.

(c) Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax.

(d) Refund of tax paid on supplies made to SEZ Unit/SEZ Developer with payment of tax.

(e) Refund of unutilized ITC on account of accumulation due to an inverted tax structure.

(f) Refund to a supplier of tax paid on deemed export supplies.

(g) Refund to a recipient of tax paid on deemed export supplies.

(h) Refund of excess balance in the electronic cash ledger.

(i) Refund of excess payment of tax.

(j) Refund of tax paid on an intra-State supply which is subsequently held to be inter-State supply and vice versa.

(k) Refund on account of assessment / provisional assessment/appeal/any other order.

(l) Refund on account of “any other” ground or reason.

In case an exporter makes supplies of goods out of India on payment of integrated tax, the refund process is governed by Rule 96 of the GST Rules. The refund in such cases shall be processed by the system designated by the Customs Department. This does not apply to the export of services out of India.

In all other cases, the refund application shall be processed by the proper officers under GST from the Centre or the State Tax Administration.

Refund of IGST paid on Export of Goods

The case of a refund of the IGST paid on exports of goods is dealt with under Rule 96 of the CGST Rules, 2017. The most important point here is that there is no specific form that needs to be filled out for claiming refund of IGST paid on export of goods- As per Rule 96(1) of the CGST Rules, 2017, the shipping bill filed by an exporter of goods shall be deemed to be an application for refund of IGST paid on the goods exported out of India.

Such an application is deemed to have been filed only when:

i. The person in charge of the conveyance carrying the export goods duly files an export manifest or an export report covering the number and the date of shipping bills or bills of export; and

ii. The applicant has furnished a valid return in FORM GSTR-3 or FORM GSTR-3B, as the case may be. The term valid return means a return furnished under section 39(1) of the GST Act, 2017 on which self-assessed tax has been paid in full.

Filing of a correct EGM is a must for treating the shipping bill or bill of export as a refund claim. The details of the relevant export invoices contained in FORM GSTR-1 are transmitted electronically by the GST portal to the Customs system and the said system, in turn, transmits back to the GST portal a confirmation that the goods covered by the said invoices have been exported out of India.

Filing of a valid return in GSTR 3B is another pre-condition for considering the shipping bill/bill of export as the claim for refund. Upon receipt of information regarding furnishing of a valid return in FORM GSTR-3B from the common portal the Customs System, processes the claim for refund and an amount equal to the integrated tax paid in respect of each shipping bill or bill of export is electronically credited to the bank account of the applicant mentioned in the taxpayer exporter’s registration particulars. Shipping Bill formats (both manual/ electronic) have been modified to make them congruent with the requirements of the IGST law.

In cases where the exporter has filed the GSTR 3B and the information furnished by the exporter in the returns GSTR 1 and GSTR 3B matches with the details filed by them in the Shipping Bills, the refunds are disbursed to the bank account of the exporter.

Important:- Remember to file your GSTR 3B and the GSTR 1 details in time; ensure that the details entered in these returns concerning what has been claimed as Exports matches with the details declared in the Shipping Bills‐ this will ensure that there are no unnecessary hitches in the clearance of your claims for refunds by the Customs Authority concerned.

IGST Refund module for exports is operational in ICES since 10.10.2017. The procedure for refund of IGST paid on export of goods under Rule 96 of CGST Rules, 2017 for all EDI locations, was provided vide instruction 15/2017- Customs, dated 9-10-2017 issued from F. No. 450/119/2017-Cus IV. The IGST refund module has been designed in line with the Rule 96 of the CGST Rules and has an in built mechanism to automatically grant refund after validating the Shipping Bill data with available in ICES against the GST Returns data transmitted by GSTN. The matching between the two data sources is done at Invoice level and any mis-match of the laid down parameters returns following error/response codes:

| Code | Meaning |

| SB000 | Invoice successfully validated |

| SBV00 | SB already validated successfully |

| SB001 | Invalid SB details |

| SB002 | EGM not filed |

| SB003 | GSTIN mismatch |

| SB004 | Invoice already received and validated |

| SB005 | Invalid Invoice Number |

| SB006 | Gateway EGM not available |

If the necessary matching is successful, ICES shall process the claim for refund and the relevant amount of IGST paid with respect to each Shipping Bill or Bill of export shall be electronically credited to the exporter’s bank account as mentioned with the Customs authorities

M.F. (D.R.) Instruction No. 20/2018-Cus., dated 26-11-2018 issued from F. No. 450/119/2017-Cus. IV (Pt-I) deals with the Refund of IGST paid on exports of goods done from Non‐EDI sites. The facility to disburse IGST refund of goods exported from Non-EDI locations is provided by DG (Systems). The procedure for processing IGST refund claims for exports made from Non-EDI sites, indicated in this Instruction, are:

- Firstly, the export data is to be captured using offline utilities and transmitted by the field formations to DG (Systems) by email.

- The data is then uploaded for verification and final submission by the Customs officer in ICES at the nearest EDI site.

- The refund scroll is then generated for the verified SBs after these are matched with the GST Returns data received from GSTN;

- A public inquiry has been made available on ICEGATE website for checking the details and IGST status of manual SBs verified in ICES.

- Specific IGST related errors or mismatches can also be checked by an importer/Customs Broker for his SBs using his ICEGATE login.

- It is only when a SB is verified by the Customs officer in ICES does it become ready for the IGST validation procedure.

The Error Codes explained

(i) SB000: Successfully Validated

This response code comes when all the decided parameters like GSTIN, SB number, Invoice Number etc. match between GSTN and Customs databases. This code implies that the SB is ripe for inclusion in the IGST refund scroll.

However, it might happen that even with SB000, the SB does not appear in the refund scroll. This could be due to:

a) The exports might have been made under bond or LUT, hence not liable for

b) If a shipping bill covers multiple invoices, few of the invoices might have been successfully validated with code SB000 whereas other invoices might be stuck with any of the other errors.

c) Higher rate of Drawback has been claimed for that SB, thus making the SB ineligible for IGST refund.

d) Where the IGST claim amount is less than Rs. 10 00/-.

In all the above cases, the scroll amount (check SB Wise IGST Claimed Status Report) shall automatically become zero and the SBs shall not be included in the refund scroll. There are two more reasons where the SBs will figure in the Temporary IGST Scroll but not in the Final Scroll. This could happen if there is an alert/suspension on the IEC in ICES or if the account of the IEC is not validated by PFMS. These cases have been elaborated below.

In respect of (a) above, there may be cases that the exporter has erroneously declared exports under LUT or zero IGST amount paid in the Shipping Bill while actually having declared and paid it in the GST Returns. Such cases can be dealt with through the officer interface.

(ii) SB001: Invalid Shipping Bill Number

This may occur due to a mismatch between the SB No. furnished in GSTR1/6A and the SB No. with customs. The possible reason for such mismatch could be a clerical error made by the exporter at the time of filing of GSTR1/6A, which can be rectified by making amendments in GSTR-1 by using Form 9A. Form 9A has been made available by GSTN w.e.f 15.12.2017 in exporter’s login at the GST Common Portal.

(iii) SB002: EGM not filed

Exporter may approach the Shipping Lines to file the EGM immediately. If EGM is already filed by shipping Line correctly, “Revalidate EGM” option may be used by EGM Officer.

(iv) SB003: GSTIN mismatch

This error occurs when GSTIN declared in the SB does not match with the GSTIN used to file the corresponding GST Returns. In this case too, the Exporter may be asked to make necessary adjustments in GSTR-1 by use of amendment Form 9A. If, however, the exporter has declared PAN instead of GSTIN in the Shipping Bill, the option to sanction the refund through officer interface shall be available, provided that the PAN given in the SB matches with the PAN of the GSTIN used to file the returns. Even in cases where the exporter has used one GSTIN to file the returns and another GSTIN issued on the same PAN to file the SB, officer interface can be used to sanction the refund. Detailed procedure is given in Annexure D.

(v) SB004: Record already received

This error code occurs due to duplicate/repeat transmission of SB-Invoice record from GSTN. The previous transmission would have already been validated with SB000 by ICES. Since these invoices are already validated, this response code may not be treated as an error. The scroll status of such SBs can be checked. If, however, the corresponding SBs are not getting scrolled out despite having SB004 response code, the reasons could be any of those listed above for SB000 cases.

(vi) SB005: Invalid Invoice Number

This is the most common error faced by the exporters, which occurs due to mismatch of invoice number as declared in the Invoice Table in the SB and that declared in the GSTR 1 for the same supply. This can happen due to:

a) Typographical mistake while entering data in GSTR 1 or the SB.

b) The exporter uses two sets of invoices, one invoice for GST and another invoice for exports resulting in mismatch of invoice numbers.

After the implementation of GST, it was explained that the details an exporter is required to enter in the “invoice” column while filing the SB pertains to the invoice issued by him compliant to GST Invoice Rules. The invoice number shall be matched with GSTN to validate exports and IGST payment. It was understood that there would not be any difference between Commercial Invoice and GST Invoice after GST since as per the GST Laws, the IGST is to be paid on the actual transaction value of the supply between the exporter and the consignee, which should be the same as the one declared on the commercial invoice. However, cases have been noticed on the continuing use of separate commercial invoice leading to mismatch. If SB005 is due to a data entry mistake in GSTR 1, it can be amended now in Form 9A. But any mistake in the SB cannot be amended once EGM is filed. Also, if the exporter has indeed used a separate invoice in the SB, he cannot include that in his GSTR 1 in lieu of his GST Invoice. Thus SB005 error, largely, cannot be corrected by any amendment either in GSTR 1 or in the Shipping Bill. It is advised that the exporters not repeat this mistake and ensure that the same GST compliant export invoice is declared at both ends.

(vii) SB006: Gateway EGM not available

In case of ICDs, if the Gateway EGM is not filed electronically or is stuck in some error, response code SB006 shall appear. The EGM shall have to be filed in ICES at the gateway port. Gateway EGM pendency and error reports can be viewed in New MIS role. The Gateway EGM details can also be checked by the exporters on ICEGATE website. In case of pending Gateway EGMs, Shipping Lines may be approached at gateway ports to file supplementary EGMs. The essential steps to file the gateway EGM successfully are:

a) File Train/Truck Summary immediately after cargo leaves the ICD.

b) Ensure that shipping Line mentions the ICD SB in his EGM filed at gateway port along with the transference copy received from gateway port.

c) Errors may be rectified through an amendment in Service Centre and approved by the proper officer. Some of the common EGM errors and their corrective action have been elaborated in Annexure B.

(viii) SBV00 – SB already validated

This response code comes in cases of SBs which had certain mismatch error(s) but was validated and sanctioned through the officer interface utility as detailed in Annexure C and D. Even for those single invoice SBs with invoice mismatch where the refund was sanctioned as per the interim procedure mentioned under para (vi) above, SBV00 shall appear. Since these SBs are already validated, this response code may not be treated as an error. The scroll status of these SBs shall also be “Ready” in the IGST Claimed Status Report.

Issues connected with the Non Transmission of Returns Data from GSTN

The above error codes can be seen by the field officer in the GSTN Integration Status Report in NewMIS. But this report includes only those SBs on which the IGST validation procedure is run. This view is also available to exporters in their ICEGATE login. As mentioned above, the validation procedure for IGST refund is run only for those SBs where EGM has been filed and for which the GSTN has transmitted the GSTR 1 returns data to Customs.

There are primarily two conditions for GSTN to transmit the data:

a) Both, GSTR1/6A and GSTR3B should have been filed for that supply

b) Invoice details (Invoice no, Invoice date or Port Code) are missing or are incorrect for that supply in GSTR 1

c) The cumulative IGST paid on exports declared in GSTR 3B (table 3.1 b) upto the month should not be less than that declared in GSTR1/6A

In respect of (a) and (b) above, the exporter can file or amend the returns accordingly. In case of (c), if the exporter has paid lesser amount in Table 3.1b of GSTR 3B, he can pay the remaining amount in the next GSTR 3B. Since GSTN compares the cumulative amounts, once the difference is paid and the cumulative of GSTR 3.1b becomes greater or equal to the cumulative of GSTR 1-Table 6A, GSTN would start transmitting the data to ICEGATE. However, in cases where the IGST on exports in GSTR 3B has been paid in the column for domestic interstate supplies (Table 3.1a) instead of Zero Rated Supplies, procedure as detailed in Board’s Circular 12/2018 dated 29.05.2018 may be followed. If the exporter finds that even after the correct filing of returns as above, their SBs do not reflect in this report, they may be advised to write to GSTN helpdesk.

Issues related to Scroll Generation

The refund of IGST on exports shall be given by generating a scroll of eligible Shipping Bills. The temporary IGST refund scroll shall be generated by the authorized officer in the CLK role in ICES. Consequently, a permanent scroll shall be generated by the authorized officer in the AC_DBK role. Only those SBs for which Temporary Scroll has been generated shall be considered for the final scroll. Once the final scroll is generated, there is no further action required from the sanctioning officer. The scroll will automatically be transmitted to PFMS and there is no further need to send the scroll to the bank separately. If a Shipping Bill is appearing in Temporary IGST refund scroll but not in Permanent IGST scroll, there could be two reasons for this:

a) Account details of the exporter have not been validated by PFMS and these scrolls may appear with the “#“ tag. A report consisting of account details which are not validated by PFMS is available both in New MIS role and COM role in ICES. The exporter may be advised to furnish correct bank account details to the proper officer in order to update the same in ICES through CLK List of possible PFMS errors reflected in the report and their solution is enclosed as Annexure A.

b) IEC of the exporter might have been suspended by the customs house for want of arrears and e-BRC etc. The SBs shall be available in the final scroll once the suspension is revoked.

There may be cases where the money does not get credited to the exporter’s account despite the SB having scrolled out successfully. Primarily, the two possible scenarios are:

i. The entire scroll gets rejected by PFMS. This happens in cases where the account details available with PFMS at the time of receipt of scroll is different than that in the scroll for one or more IECs. In such cases, the jurisdictional System Manager, after having confirmed that the money was indeed not credited to any of the exporters’ accounts from that scroll, can write to ICEGATE helpdesk at once 6 giving the scroll details. The reconciliation and scroll cancellation process may take 2-3 weeks. Once the scroll is cancelled, the SBs shall again be available for the next scroll.

ii. The scroll gets accepted by PFMS but the accounts of some exporters get failed by the respective banks due to inactive or invalid account. In such cases, only the exporters with failed accounts shall not have the credit of the refund. These are referred to by PFMS as “Failed after Success” cases for which ICES Advisory 21/2018 dated 17.05.2018 may be seen for the interim procedure to be followed.

The Role of the Exporter in Resolution of issues

(a) The exporter has the option to check the GST validation Status for his SBs in his ICEGATE website login. This report shows the exporter the response/error codes for each of his SBs wherever data has been received from GSTN. The reasons for non-receipt of data from GSTN have already been elaborated above.

(b) The exporter also has the option to view the SB details relevant for IGST validation on the ICEGATE website. The exporter can view this while filing the GST Returns and ensure that the details are entered accurately in the Returns as well so that no mismatch occurs.

(c) In case, the exporter’s account is not validated by PFMS, he may approach jurisdictional Customs Commissionerate with correct account details and get it updated in ICES. iv. If the exporter is not getting the refund due to suspension/alert on his IEC, he may clear his dues or submit e-BRC and have the suspension revoked.

Errors in PFMS Validation and their Rectification

| S. No. | Error Code | Error Description | Rectification |

| 1. | TBE0001 | Error in reading file, File is malformed or Failed during schema validation. | Not Applicable |

| 2. | TBE0002 | Mandatory Tags values are missing in the Header Part. | Not Applicable |

| 3. | TBE0003 | Invalid Batch Format | Not Applicable |

| 4. | TBE0004 | Duplicate Batch ID/Message ID not allowed. | Not Applicable |

| 5. | TBE0005 | Invalid Assessee Type | Not Applicable |

| 6. | TBE0006 | Same [Assessee Code, Location Code, Assessee Type, Source] already exists in PFMS. This validation will be not be applied for Update and Delete type requests. | Submit again |

| 7. | TBE0007 | [Assessee Code, Location Code, Assessee Type, Source] not exists in PFMS. This validation will be applied for Update and Delete type requests. | Submit Again |

| 8. | TBE0008 | Rejected by Bank, As per Bank Account Number is Invalid. | Check the Account Number for correctness – Submit correct details: Ensure that details are submitted only once during the day |

| 9. | TBE0009 | Bank Name is not as per PFMS Bank Master. | Not applicable – May occur only with other errors |

| 10. | TBE0010 | Bank Account details have not been provided | Check the Account Number for correctness – Submit correct details |

| 11. | TBE0011 | Mobile Number should be of 10 digits only. | Not Applicable |

| 12. | TBE0012 | Invalid Value for Location Code | Inform DG systems for rectification |

| 13. | TBE0013 | Invalid Value for Division Code | Inform DG systems for rectification |

| 14. | TBE0014 | Invalid value for Purpose, It should be A/U/D. | Not Applicable |

| 15. | TBE0015 | Invalid IFSC Code. | Check the IFSC Code for correctness – Submit correct details |

| 16. | TBE0016 | Rejected by Bank, Account No does not exist in Bank | Check the Account Number for correctness – Submit correct details |

| 17. | TBE0017 | Rejected by Bank, Account status is closed. | Check the Account Number for validity – Submit correct details |

| 18. | TBE0018 | Duplicate Assessee Details [Assessee Code, Location Code, Assessee Type, Source] Found In The File. – Applied for ICEGATE. Can be modified for ACES | Submit Again |

| 19. | TBE0019 | Blocked Account | Submit another valid Account details |

| 20. | TBE0020 | One or more mandatory tags values are missing in the detail section. | Not Applicable |

| 21. | TBE0021 | IFSC Code does not exists in PFMS. | Inform DG System for Rectification |

| 22. | TBE0022 | Actual records count and No. of records in details, it should be same. | Not Applicable |

| 23. | TBE0023 | Assessee already exists. | Submit Again |

| 24. | TBE0024 | Assessee code does not exist during update. | Submit Again |

| 25. | TBE0025 | More than one record found during update data. | Submit Again |

”Not applicable” means that these are Structural errors which shall not appear in this report.

Other Common EGM errors and their Rectification

(a) Errors at Gateway Port – SB002 error Container No. Mismatch (Error Code: C)

If the Container Number mentioned in the Shipping Bill(S/B) differs from the Container Number mentioned in the EGM against that S/B, EGM will be submitted with error flag ‘C’ and the S/B will move to the EGM Error Queue with this error code.

(i) If the mistake is in the EGM, request for EGM Amendment – Update has to be submitted at the service centre. This EGM Amendment has to be approved by proper officer.

(ii) If the mistake is in the S/B, Container Number has to be amended in the S/B.

(b) Number of Container Mismatch (Error Code: N)

If the Total Number of Containers mentioned in the S/B differs from the Total Number of Containers mentioned in the EGM against that S/B, EGM will be submitted with error flag ‘N’ and the S/B will move to the EGM Error Queue with this error code.

(i) If the mistake is in the EGM, request for EGM Amendment – Delete has to be submitted at the service centre for deleting the concerned SB from EGM. This EGM Amendment has to be approved by the proper officer. After deletion, Amendment – Add has to be submitted at the service centre for adding SB with correct details. This too shall then be approved by the proper officer.

(ii) If the mistake is in the S/B, post stuffing stage, direct amendment is not possible in the S/B. In those cases, a procedure as detailed separately below has to be followed.

(c) LEO date greater than Sailing Date (Error Code: L)

If LEO granted for a S/B is cancelled in the System for amendments, the same would be granted again after carrying out the amendments in the System. If Sailing Report for the vessel (EGM), under which the said S/B is covered, is entered in the System before granting the subsequent LEO, then EGM will be submitted with error flag ‘L’

At times, while entering the Sailing Report, the Preventive Officer posted at Harbour Main Gate may enter the sailing date wrongly.

There is no option to rectify this error. In such cases, officers posted in EDC have to be contacted for exercising the option “Forceful Removal of SBs from EGM-ERROR”, which will remove the concerned S/B from the EGM Error queue.

(d) Nature of Cargo Mismatch (Error Code: T), Number of Packets Mismatch (Error Code: P)

(i) If the mistake is in the EGM, request for EGM Amendment – Update has to be submitted at the service centre. This EGM Amendment has to be approved by the officers posted in EDC.

(ii) If the mistake is in the S/B, post stuffing stage, direct amendment is not possible in the S/B. In those cases, a procedure as detailed separately below has to be followed.

(e) Procedure for correcting errors in Shipping Bill filed at Gateway Port (for SB002 error):

(i) Annexure has to be submitted at the Service Centre for EGM Amendment Delete for deleting the concerned SB from the EGM. This EGM Amendment has to be approved by proper officer.

(ii) After the approval of deletion, LEO granted for the concerned S/B has to be cancelled.

(iii) After the cancellation of LEO, amendments have to be carried out at the Service Centre, as per the procedure. These SB Amendments have also to be approved.

(iv) After the approval, Goods Registration and LEO has to be granted again in the System.

(v) After granting of LEO, Stuffing Report, if required, has to be entered in the System.

(vi) After LEO and/or Stuffing, Annexure has to be submitted at the Service Centre for EGM Amendment– Add for including that SB in the concerned EGM and have it approved by the proper officer.

NOTE: In some cases, after cancellation of LEO, entering correct details at the time of Re-registration, LEO and/or Stuffing alone will solve the problem.

(f) EGM related errors at ICD (SB006) – Mismatches between the Truck/Train Summary and Gateway EGM

Step 1: Check the Gateway EGM Status in ICES/ICEGATE

A view has been given both in ICES (in View SB) as well as ICEGATE public enquiry giving Gateway EGM details. The filing status and EGM error, if any, can be ascertained here. Gateway EGM error and success reports are also available in New MIS. Following are the main errors noticed in Gateway EGM filing:

M – Gateway Port code given in truck summary different from actual gateway port.

N – No. of Container Mismatch

C – Container No. Mismatch

T – Nature of Cargo Mismatch

L – LEO Date > Sailing Date

Step 2: Gateway EGM details are Blank:

2a. If the gateway EGM detail is blank in the SB View, kindly ascertain whether the Gateway EGM has indeed been filed and the Gateway EGM in which the particular cargo was exported.

2b. Enquire with the Shipping Line, if the EGM filed has the correct details of SB/AWB as the case may be.

2c. If the EGM is already filed, option “Revalidate EGM” in seaports or “Revalidate AWB” in air cargo may be used. The option is available in the EGM role

2d. If the EGM is not filed/ filed incorrectly, supplementary EGM needs to be filed by Shipping Line and approved by Gateway Port Officer.

Step 3: The Gateway EGM is in Error:

For errors M and L, ICES Advisory 04/2018 dt. 19.02.2018 may be seen. An option has been made available in the role of AC (Exports) of ICDs to rectify Gateway EGM errors M and L resulting in SB006 mismatch. In case of error M, the officer can fill in the actual gateway port of export, and in case of error L, the officer can give the actual sailing date as the LEO date after doing necessary verifications of actual exports as suggested in the advisory.

For errors N and C, an option has been made available in the Preventive Officer role (PREV_OFF) at the Gateway Port to rectify container details. (ICES Advisory 08/18 dt. 09.03.2018). The preventive officer can amend container details in the Gateway EGM CTR Amendment Option to remove the mismatch after verifying the package and quantity details and satisfying himself that there is no short shipment.

For Error A in Gateway EGM, the option of “Revalidate EGM” may be used.

Once the above corrections are made, the gateway port has been given the option to Revalidate EGM in the EGM role to validate the gateway EGM with the corrected values. Even in cases where the local EGM/truck summary is submitted after the filing of the Gateway EGM for some reason, the option to Revalidate EGM should be used first.

With the above options, solution is available with the customs officer for rectifying all the major EGM errors.

Alternate Mechanism with Officer Interface for SBs with Invoice Mismatch Error (SB005)

Board has issued Circular 05/2018 dt. 23.02.2018 in this regard, consequently, the officer interface module has been designed and made available in ICES (ICES Advisory 05/20 18 dt. 26.02.20 18).

The advisory lists the steps to be followed while using the officer interface.

(i) It may be noted that this utility is available only for those SBs where:

a) The error is SB005 only. The SB wise error can be seen from the IGST Integration Status Report in New MIS. Since this report is at invoice level, it may be verified that there is no error other than SB005 for any of the SBs. Only those SBs where there SB005 error exists for at least one invoice and the remaining invoices are validated with SB000 shall be available for rectification in this module. On entering any ineligible SB number, the system shall not allow further processing.

b) If all the invoices of that SB are already validated with SB000, that SB shall not be available for any modification in this utility. Similarly, those single invoice SBs filed before 31.10.2017 where the SB level validation was run despite the SB005 error shall also be not available in this For each of these invoices, the system will throw up an error stating that there is no invoice for this SB pending validation.

c) The SBs whose data have not been transmitted by GSTN will also not appear in this module. These SBs shall not be available in the IGST Integration Report either. For such SBs, system will throw up an error that “There is no information received from GSTN for this SB”. The exporter may be advised to correct the inconsistencies in GST Returns as detailed in Para 5 first before submitting the concordance table.

(ii) As discussed in the advisory, after entering the eligible SB number, the first screen shown on the system shall be the details as declared by the exporter in his GSTR 1 and as transmitted by GSTN. The next screen shall show the officer the details available in the SB. Here, the officer can accept/change the IGST refund amount basing on the concordance table as also discussed elaborately in the Illustration given in the advisory. The officer shall have to verify each invoice and enter the IGST Refund amount for the system to allow to continue to the next screen. The option to rectify the approved IGST amount has been given to the officer for him to correct any mistakes made by the exporter in declaring the same in SB. The officer can also change the amount if the exporter had inadvertently entered zero value in the SB although he has declared and paid the IGST in the GST Returns for that SB. While the officer shall do the verification basing on the concordance table submitted by the exporter, he can calculate the IGST amount against each invoice himself (ref ICES Advisory 011/2017 dt. 26.07.2017) in case he finds the concordance table to be inaccurate.

(iii) Once the verified IGST amount is entered for all the invoices, the officer can move to the next screen and confirm the invoice mapping as per the concordance table. Once completed, the system shall calculate the IGST scroll amount for that SB. It may be noted here that notwithstanding the amount entered by the officer, the IGST Scroll amount shall be reduced appropriately for the invoices where composite rate of drawback has been claimed for some items. In case, all the items in an invoice are composite drawback rate availed, the IGST scroll amount shall consequently be calculated as zero.

(iv) The verified SBs shall be available for the next scroll even if the error code in the IGST Integration status report does not change immediately. As also discussed above, once all the invoices of a SB are verified, it shall not be available again for any further rectification in this module.

With this module, solution is available with the customs officer for all the pending SB005 SBs.

Alternate Mechanism with Officer Interface for SBs with Certain Other Errors

In consonance with Para 2(ii) of Board’s Circular 08/2018 dt. 23.03.2018 and subsequent instructions from Board, the officer interface facility has been extended to sanction refund in the following two cases, in addition to invoice mismatch cases:

a) Cases where the exporter has erroneously declared that the shipment is without payment of IGST, although they have declared and paid the IGST in GST Returns.

b) SBs with error code SB003, where the exporter has either declared a different GSTIN in the SB or has only declared PAN, and the corresponding returns have been filed through another GSTIN with the same PAN

2. Such cases may now be handled through officer interface the same way as the Invoice Mismatch (SB005) cases, the procedure of which is detailed in Annexure C. In case of (a) above The officer may verify the actual IGST payment in GST Returns for each invoice which is displayed to the officer in the officer interface and basing that, may enter the admissible IGST refund amount in the next screen where data as declared in Shipping Bill is displayed. It is re-iterated that only those SBs where no other mismatch exists shall be available for rectification.

3. In case of (b), an undertaking may be obtained from the GST registered unit which has filed the returns that they have no objection to the refund being granted to the exporter who has filed the Shipping Bill and that they will not claim any IGST Refund for exports under that SB separately. Once satisfied, the Officer may sanction the applicable IGST Refund through the Officer interface.

Restrictions on the claim of refund of IGST paid on export of goods and services

In certain situations, the Exporters having already availed of specified benefits may not be eligible to claim a refund of the IGST relating to exports – these are dealt with in Sub-rule (10) of rule 96 of the CGST Rules.

As such, the refund of IGST paid on exported goods and services is not allowed if the goods are procured from a supplier who has availed the benefit of the following notifications: –

(i) Notification no. 40/2017-Central Tax (Rate) or Notification No 41/2017-Integrated Tax (Rate) both dated 23rd October 2017: – This notification prescribes a CGST rate of 0.05% / IGST 0.1% if goods are supplied by a registered supplier to a registered recipient for export (merchant exporter) subject to certain conditions.

(ii) Notification no. 48/2017-Central Tax dated 18th October 2017:- This notification notifies supplies to be considered as deemed exports.

However, exporters who have used the EPCG scheme to bring in Capital Goods, either through import in terms of notification No. 79/2017-Customs dated 13.10. 2017 or through domestic procurement in terms of notification No. 48/2017-Central Tax, dated 18.10.2017, continue to be eligible to claim a refund of Integrated tax paid on exports and would not be hit by the restrictions provided in sub-rule (10) of rule 96 of the CGST Rules.

Further, the refund of IGST paid on exported goods and services is also not allowed if the exporter has availed the benefit of the following Notifications:

a) Notification no. 78/2017-Customs dated 13th October 2017:- This notification provides an exemption to IGST and compensation cess levied on goods imported by EOU.

b) Notification no. 79/2017-Customs dated 13th October 2017:- This notification provides IGST exemption and Compensation Cess exemption to goods imported against advance authorization.

Please Note:- The exporter of goods and services in such cases can still export the goods and services only under LUT/ bond but cannot make such export on payment of the integrated tax (IGST).

The explanation to Rule 96(10) clarifies that, the benefit of the notifications mentioned above shall not be considered to have been availed only where the registered person has paid Integrated Goods and Services Tax and Compensation Cess on inputs and has availed exemption of only Basic Customs Duty (BCD) under the said notifications. This makes it clear that the exporter can import goods by availing the Basic Customs Duty exemption under the above notifications but on payment of IGST. In such a case, the provisions of Rule 9 6(10) will not be attracted, and the exporter can export on payment of IGST.

In any other case, the exporter of goods and services can export the goods and services only under LUT/ bond and cannot export on payment of the integrated tax (IGST).

The tabulation below explains the restrictions made under Rule 9 6(10) of the CGST Rules, 2017:

| The persons claiming refund of integrated tax paid on exports of goods or services should not have received supplies on which the following benefits have been availed:- | ||

| 1.

|

Notification No. 48/2017- Central Tax, dated the 18th October, 2017, except so far it relates to receipt of capital goods by such person against Export Promotion Capital Goods Scheme

|

Supply of goods by a registered person against Advance Authorisation |

| Supply of capital goods by a registered person against Export Promotion Capital Goods Authorisation | ||

| Supply of goods by a registered person to Export Oriented Unit | ||

| Supply of gold by a bank or Public Sector Undertaking specified in the | ||

| notification No. 50/2017-Customs, dated the 30th June, 2017 (as amended) against Advance Authorisation. | ||

| Notification 48/2017- CT.– Seeks to notify the above supplies as deemed exports under section 147 of the CGST Act, 2017. | ||

| 2. | Notification No. 41/2017- Integrated Tax (Rate), dated the 23rd October, 2017 | Notification 41/2017-Integrated Tax (Rate), dt. 23- 10-2017 – Seeks to prescribe Integrated Tax rate of 0.1% on inter-State supply of taxable goods by a registered supplier to a registered recipient for export subject to specified conditions. |

| 3. | Notification No. 40/2017- Central Tax (Rate), dated the 23rd October, 2017, | Notification 40/2017-Central Tax (Rate) ,dt. 23-10- 2017 – Seeks to prescribe Central Tax rate of 0.0 5% on intra-State supply of taxable goods by a registered supplier to a registered recipient for export subject to specified conditions. |

| The persons claiming refund of integrated tax paid on exports of goods or services should not have availed the benefit under the following: – | ||

| 1. | Notification No. 78/2 017- Customs, dated the 13th October, 2017 | Seeks to exempt goods imported by EOUs from integrated tax and compensation cess by amending Notification No. 52/2003-Customs, dated 31st March, 2003 |

| 2. | Notification No. 79/2017- Customs, dated the 13th October, 2017, except so far it relates to receipt of capital goods by such person against Export Promotion Capital Goods Scheme. | Notification No. 79/2017-Customs, dated the 13th October, 2017 – Seek to amend various Customs exemption notifications to exempt Integrated Tax/Cess on import of goods under AA/EPCG schemes – the notification amended by this are the following: 16/2015-Customs, dated 1st April, 2015; 18/2015-Customs, dated 1st April, 2015; 20/2015- Customs, dated 1st April, 2015; 21/2015-Customs, dated 1st April 2015; 22/2015-Customs, dated 1st April, 2015 & 45/2016-Customs, dated 13th August, 2016 |

Applying for a refund on the GST Portal

A refund application in FORM GST RFD‐01 shall be filled on the common portal by an applicant seeking refund under any of the following categories:

(a) Refund of unutilized input tax credit (ITC) on account of exports without payment of tax.

(b) Refund of tax paid on export of services with payment of tax.

(c) Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax.

(d) Refund of tax paid on supplies made to SEZ Unit/SEZ Developer with payment of tax.

(e) Refund of unutilized ITC on account of accumulation due to inverted tax

(f) Refund to supplier of tax paid on deemed export supplies.

(g) Refund to recipient of tax paid on deemed export supplies.

(h) Refund of excess balance in the electronic cash ledger.

(i) Refund of excess payment of tax.

(j) Refund of tax paid on intra-State supply which is subsequently held to be inter-State supply and vice versa.

(k) Refund on account of assessment/provisional assessment/appeal/any other order.

(l) Refund on account of “any other” ground or reason.

Important :- The statements/declarations/undertakings which are part of FORM GST RFD-01 itself, and also other documents/invoices which are to be uploaded as indicated in Table 2 above shall be required to be provided by the applicant for processing of the refund claim.

No other document needs to be provided by the applicant at the stage of filing of the refund application

Submitting Refund Pre‐Application Form

Refund Pre-Application is a form, which needs to be submitted by the taxpayers to provide certain information related to nature of business, Aadhaar Number, Income Tax details, export data, expenditure and investment etc. To submit Refund Pre-Application Form, perform following steps:

1. Login to the GST Portal. Navigate to Services> Refunds > Refund pre‐ application Form option.

Note:

- Taxpayer is not required to sign the Refund Pre-Application form.

- Once the form is submitted, you cannot edit or re-submit the form.

2. Refund pre‐application Form page is displayed.

3. Select the Nature of Business from the options given.

4. Select the Date of Issue of IEC (Only for Exporters).

5. Enter the Aadhaar Number of Primary Authorized Signatory.

6. Enter the Value of Exports made in the Financial Year 2019‐2020 (till date) (Only for Exporter), Income tax paid in Financial Year 2018‐2019, Advance tax paid in Financial Year 2019‐2020 (till date) and Capital Expenditure and investment made in Financial Year 2018‐2019.

7. Select the declaration checkbox and click SUBMIT.

8. A confirmation message about the submission of the form is displayed.

Note: On submitting the refund pre-application form, an acknowledgement message will be shown to you on the screen. No separate e-mail or SMS will be sent to you for the same.

Documents/Statements/Undertakings/Declarations to be made along with the refund application being filed on the GST Portal

| S. No. | Type of Refund | Declaration/Statement/Undertaking/ Certificates to be filled online | Supporting documents to be additionally uploaded |

| 1. | Refund of unutilized ITC on account of exports without payment of tax | a) Declaration under the second and third proviso to section 54(3)

b) Undertaking in relation to sections 16(2)(c) and section 42(2) c) Statement 3 under rule 89(2)(b) and rule 89(2)(c) d) Statement 3A under rule 89(4)2 |

a) Copy of GSTR-2A of the relevant period

b) Statement of invoices in prescribed format Annexure B c) Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period d) BRC/FIRC in case of export of services and shipping bill (only in case of exports made through non-EDI ports) in case of goods |

| 2. | Refund of tax paid on export of services made with payment of tax | a) Declaration under second and third proviso to section 54(3)

b) Undertaking in relation to sections 16(2)(c) and section 42(2) c) Statement 2 under rule 89(2)(c) |

a) BRC/FIRC /any other document indicating the receipt of sale proceeds of services

b) Copy of GSTR-2A of the relevant period Statement of invoices c) Self-certified copies of invoices entered in Annexure-A whose details are not found in GSTR-2A of the relevant period d) Self-declaration regarding non-prosecution under sub-rule (1) of rule 91 of the CGST Rules for availing provisional refund |

| 3. | Refund of unutilized ITC on account of Supplies made to SEZ units/developer without payment of tax | a) Declaration under third proviso to section 54(3)

b) Statement 5 under rule 89(2)(d) and rule 89(2)(e) c) Statement 5A under rule 89(4) d) Declaration under rule 89(2)(f) e) Undertaking in relation to sections 16(2)(c) and section 42(2) f) Self-declaration under rule 89(2)(l) if amount claimed does not exceed two lakh rupees, certification under rule 89(2)(m) otherwise |

a) Copy of GSTR-2A of the relevant period

b) Statement of invoices (Annexure-B) c) Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period d) Endorsement(s) from the specified officer of the SEZ regarding receipt of goods/services for authorized operations under second proviso to rule 89(1) |

| 4. | Refund of tax paid on supplies made to SEZ units/develop er with payment of ta | a) Declaration under second and third proviso to section 54(3)

b) Declaration under rule 89(2)(f) c) Statement 4 under rule 89(2)(d) and rule 89(2)(e) d) Undertaking in relation to sections 16(2)(c) and section 42(2) e) Self-declaration under rule 89(2)(l) if amount claimed does not exceed two lakh rupees, certification under rule 89(2)(m) otherwise |

a) Endorsement(s) from the specified officer of the SEZ regarding receipt of goods/services for authorized operations under second proviso to rule 89(1)

b) Self-certified copies of invoices entered in Annexure-A whose details are not found in GSTR-2A of the relevant period c) Self-declaration regarding non-prosecution under sub-rule (1) of rule 91 of the CGST Rules for availing provisional refund |

| 5. | Refund of ITC unutilized on account of accumulation due to inverted tax structure | a) Declaration under second and third proviso to section 54(3)

b) Declaration under section 54(3)(ii) c) Undertaking in relation to sections 16(2)(c) and section 42(2) d) Statement 1 under rule 89(5) |

a) Copy of GSTR-2A of the relevant period