REFUND UNDER GST

1. INTRODUCTION

1.1 Government of India levies and collects duties and taxes from the taxpayers. However, in specified situations, if any amount, which is not due to the Government is paid by any person then the Government refunds the such amount to such person, on following the due process prescribed under the GST law.

1.2. The relevant provisions of CGST Act, 2017 IGST Act, 2017 and CGST Rules, 2017, pertaining to this Chapter are as under –

| Sr. No. | Section/Rule | Provision pertaining to |

| 1 | Section 27 of CGST Act, 2017 | Special provisions relating to casual taxable person and non-resident taxable person |

| 2 | Section 54 of CGST Act, 2017 | Refund of tax |

| 3 | Section 55 of CGST Act, 2017 | Refund in certain cases |

| 4 | Section 56 of CGST Act, 2017 | Interest on delayed refunds |

| 5 | Section 107 of CGST Act, 2017 | Appeals to Appellate Authority |

| 6 | Section 112 of CGST Act, 2017 | Appeals to Appellate Tribunal |

| 7 | Section 115 of CGST Act, 2017 | Interest on refund of amount paid for admission of appeal |

| 8 | Section 16 of IGST Act, 2017 | Zero rated supply |

| 9 | Rule 89 of CGST Rules, 2017 | Application for refund of tax, interest, penalty, fees or any other amount |

| 10 | Rule 90 of CGST Rules, 2017 | Acknowledgement |

| 11 | Rule 91 of CGST Rules, 2017 | Grant provisional refund |

| 12 | Rule 92 of CGST Rules, 2017 | Order sanctioning refund |

| 13 | Rule 93 of CGST Rules, 2017 | Credit of the amount of rejected refund claim |

| 14 | Rule 94 of CGST Rules, 2017 | Order sanctioning interest on delayed refunds |

| 15 | Rule 95 of CGST Rules, 2017 | Refund of tax to certain persons |

| 16 | Rule 96 of CGST Rules, 2017 | Refund of integrated tax paid on goods (or services) export-ed out of India |

| 17 | Rule 96A of CGST Rules, 2017 | Export of goods or services under Bond or Letter of Undertaking |

| 18 | Rule 96B of CGST Rules, 2017 | Recovery of refund of unutilized input tax credit or integrat-ed tax paid on export of goods where export proceeds not realized. |

| 19 | Rule 96C of CGST Rules, 2017 | Bank Account for credit of refund |

1.3 GST refund is a process in which, any person (registered or unregistered) can claim refund of any balance in electronic cash ledger or any tax, interest, penalty, fees or any other amount paid which was not required to be paid by him. “Refund” under the GST law includes: –

(a) Any balance amount in the electronic cash ledger or any tax which was paid in excess;

(b) Interest paid on such tax;

(c) Any other amount paid, which was not required to be paid;

(d) Tax paid on export of goods or services or both, tax paid on the deemed exports as notified in Notification No. 48/2017-C.T. dated 18.10.2017, as amended;

(e) Any unutilized input tax credit on account of-

(i) zero rated supplies made without payment of tax; or,

(ii) inverted duty structure.

(f) Supply which is not provided, either wholly or partially and for which invoice has not been issued or refund voucher has been issued;

(g) Any other amount paid on intra-State supply, which is subsequently held to be inter-State supply and vice versa;

(h) Refund to Casual Taxable Person/ Non-Resident Taxable Person (subject to furnishing all returns for the period of continuity of registration);

(i) Refund of pre-deposit;

(j) Tax paid by the notified agency of UNs or Embassy/Consulate, etc. on inward supply.

1.4 GST provides for an efficient invoice based tracking system with the help of the periodical GSTR-1 Returns, wherein the registered person furnishes the details of the outward supplies, which help in verifying the transactions on an individual basis and thus, allowing systematic checking of the same.

1.5 Timely refund of the amount claimed is essential in tax administration, as it facilitates trade through release of blocked funds for working capital, expansion and modernization of existing business.

1.6 The provisions pertaining to refund contained in the GST law aim to streamline and standardise the refund procedures. The claim and sanctioning procedure are completely online and time bound.

1.7 All types of refunds, including the refund of input tax credit and refund of IGST paid on export of services is handled by GST department, except refund of IGST paid on goods exported, which is handled by Customs.

1.8 Refund claim needs to be filed within two years from the ‘relevant date’.

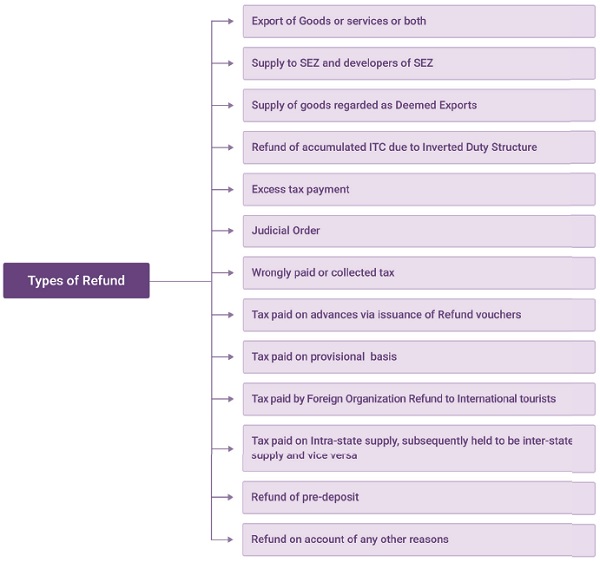

2. SITUATIONS LEADING TO REFUND CLAIMS:

2.1 A Refund Claim under GST may arise on account of the following;

2.2 TYPES OF REFUNDS

(I) Export of Goods with payment of tax/ Export of Goods or services without payment of tax –

(i) One of the categories under which claim for refund may arise would be on account of exports. All exports, whether of goods or services, have been categorized as ‘Zero Rated Supplies’ in the IGST Act, 2017. On account of zero rating of supplies, the supplier is entitled to claim Input Tax Credit in respect of goods or services or both used for supplies exported under Bond or Letter of Undertaking, though exempt from payment of tax.

(ii) Every person making claim of refund on account of zero rated supplies has two options, either he can export under Bond/LUT and claim refund of accumulated Input Tax Credit; or he may export the goods and/or services on payment of Integrated tax and claim refund of the tax paid as per the provisions of Rule 96 of CGST Rules, 2017. The concept here is that the goods and services are to be exported but not the taxes incurred by the registered taxpayers in manufacture and supply of goods or for providing services, so that India as a country remains competitive in global world trade.

For example, a registered manufacturer purchases his inputs and incurs tax liability on his purchases. When this registered manufacturer exports his final products/goods to some person outside India, then under the GST law the tax borne on such inputs, accumulated as input tax credit balance in his Electronic Credit Ledger, is either allowed to be used for payment of tax in respect of the domestic taxable supplies or refunded in cash as per the entitlement vis-à-vis the exports made, which is computed as per the formula provided in Rule 89(4) of the CGST Rules, 2017. Same is the case with export of services. (Section 54 of CGST Act, 2017)

(II) Supply of goods and services to SEZ and developers of SEZ – Special Economic Zones (SEZ) are geographically located in India but are considered as a foreign territory for the purpose of taxation. All the goods and services produced/generated from an SEZ are meant for exports only. Therefore, any registered person in the taxable territory of India, when supplies his goods or services to a non-taxable territory geographically located in India, such as SEZ unit or to developers of SEZ, then that supplier is entitled to get the refund of his accumulated ITC. Supplies made to SEZ unit or developer of SEZ are also ‘zero rated’ supplies and are also termed as ‘deemed exports’.

(III) Supply regarded as Deemed Exports: Notf. No 48/2017-CE dated 18.10.2017 has notified certain supplies as ‘Deemed Export’. The application for Refund of deemed exports may be filed;

(a) by the recipient of deemed export supplies; or

(b) by the supplier of deemed export supplies in case the recipient does not avail ITC on such supply.

(IV) Purchases made by Foreign organizations – All foreign establishments such as those of United Nations, Embassies and Consulates of other nations, having establishments geographically located in India are also considered to be foreign territories for the purpose of taxation. Section 55 of the CGST Act, 2017 provides for refund of tax paid on notified supplies received by UN bodies and embassies and other international organisations notified by the Government. A taxable person making supplies to such bodies would charge the tax due and remit the same to government account. However, the UN bodies and other notified entities can claim refund of the taxes paid by them on their purchases. The claim has to be made before the expiry of two years from the last day of the quarter in which such supply was received. (Section 55 of the CGST Act)

(V) Refund of accumulated ITC on Inverted Duty Structure – There are certain scenarios where the output product has lesser GST rate than the input GST rate. This is called as the ‘inverted duty structure’. In such a scenario, there is a net accumulation of Input Tax Credit (ITC) in the Electronic Credit Ledger of the registered taxpayer. This can be claimed as refund under the GST law.

(VI) Refund of Excess tax payment – Sometimes the taxpayer can make mistake in calculation of his liability and deposit excess tax, more than his actual liability. Under GST law, such excess amount of tax is refunded to the taxpayers.

(VII) Refund due to Judicial Order – Court or Appellate Authority or judicial forum can direct the government to refund certain amount due to various reasons, which are generally recorded in the speaking order passed by that judicial or quasi-judicial authority. GST law provides for refund of such amount.

(VIII) Refund of wrongly paid or collected tax–A registered taxpayer can wrongly pay one form of tax in place of other. For example, a person mistakenly pays IGST in place of CGST and SGST and vice versa. In order to rectify such mistake, GST law provides that the taxpayer first pay the tax amount in proper head and then claim refund of the wrongly paid tax. Interest will not be charged in such case. Further, a person collecting wrong amount of tax should deposit the same to the government.

(IX) Refund of tax paid on advances via issuance of Refund vouchers – It generally happens that during a contract, suppliers demand a minimum confirmation advance from the buyer to supply the desired goods and services. The advance paid by the recipient of goods and services to the supplier is subjected to GST. However, when the contract is not executed and cancelled, the supplier generates refund voucher and credits the account of the supplier the amount of advance received, excluding the GST paid on such advance. Here the receiver can claim back the tax amount paid to that supplier from GST Department as refund by following the due process, as there is no supply.

(X) Refund of tax paid on provisional basis–Sometimes, there is no full clarity with respect to the value of goods and services or the rate of tax applicable on such goods and services. In such non-clear scenarios, the taxpayer requests for the ‘provisional’ assessment of the rate of duty and pays the tax amount then applicable. However, once the exact value of supply and the rate of tax applicable on such supply is clear the exact amount of tax becomes calculable and the taxpayer becomes eligible for refund of tax on finalization of the assessment, if the tax under provisional assessment deposited is greater than the actual tax.

(XI) Refund to International tourists – While travelling to India, many international tourists make purchases of goods and services during their stay and hence bear the taxes incorporated in the market value of such goods and services. The GST law has provision to refund the tax Component on all such purchases made by international tourists when they finally leave India, subject to the fulfilment of certain terms and conditions. However the said section has not yet been notified on recommendations of GST Council.

(XII) Tax paid on Intra-state supply, subsequently held to be inter-state supply and vice- versa – Intra-state supply will attract CGST and SGST while inter-state supply will attract IGST. Thus, if a taxpayer considers a supply as intra-state, he will pay CGST and SGST. However, due to some reasons later on the same supply is treated as inter-state supply, then such taxpayer shall pay IGST first and then will be eligible to get the refund of CGST and SGST paid earlier. A vice-versa scenario is also possible.

(XIII) Refund of pre-deposit–For filing appeal against any order before the Appellate Authority or Tribunal, the appellant has to make pre-deposit of the amount stipulated in the relevant provisions of CGST Act. In case the Appellate Authority or the Tribunal decides the case in favour of the appellant and such order is accepted by the Department, i.e. no appeal is filed against such order, then the amount of pre-deposit can be claimed by the appellant as refund. Section 115 of the CGST Act also provides for payment of interest on such pre-deposit. (Section 115 of CGST Act, 2017)

(XIV) Refund on account of any other reasons– Refund of any amount, which is not liable to be paid by the taxpayer but has been paid and not covered under any of the above reason, are covered under this category of refund. Some of the reasons are –

(a) Tax collected by the taxable person more than the tax due on such supplies must be credited to the Government account. The law makes explicit provision for the person who has borne the incidence of tax to file refund claim in accordance with the provisions of Section 54 of CGST Act, 2017. (Section 54 of CGST Act, 2017)

(b) A casual/Non-resident Taxable Person has to pay tax in advance at the time of registration. Refund may become due to such persons at the end of the registration period because the tax paid in advance may be more than the actual tax liability on the supplies made by them during the period of validity of registration period. The law envisages refund to such categories of taxable persons also. But the amount of excess advance tax shall not be refunded unless such person has filed all the returns due during the time their registration was effective.

(XV) Canteen Store Departments (CSDs) have been notified under Section 55 of the CGST Act, 2017 vide Notification No. 6/2017- Central Tax (Rate) dated 28.06.2017 for refund of 50% of applicable Central Tax paid on all inward supplies of goods received by it for the purposes of subsequent supply of such goods to the Unit Run Canteens of the CSD or to the authorized customers of the CSD.

3. STATUTORY PROVISIONS AND MANNER OF FILING CLAIM FOR REFUND UNDER GST LAW.

3.1 (a)The refund application for balance in Electronic Cash Ledger is required to be made in FORM GST RFD-01. The balance in the Electronic Cash Ledger is required to be refunded after the taxpayer discharges the entire liability towards tax, interest, penalty, fee or any other amount payable under the Act or the rules made thereunder, in accordance with the provisions of Section 54 of CGST Act. (Section 54, 54(4) of CGST Act, 2017)

3.1 (b) The application for refund should be accompanied by-

- Documentary evidence prescribed to establish that a refund is due to the applicant; and

- Evidence that incidence of duty has not been passed on by him to any other person.

- However, where the amount claimed as refund is less than two lakh rupees, self-declaration based on documents available with him is sufficient – Section 54(4) of CGST Act.

3.2 Refund of IGST paid on services exported – Refund of IGST paid on services exported shall be filed in FORM GST RFD-01 and shall be dealt in accordance with provisions of Rule 89 of CGST Rules. (Rule 96(9) of CGST Rules, 2017) (Rule 89 & 96(9) of CGST Rules, 2017)

3.3 Refund of IGST paid on goods exported–

(a) Refund of IGST paid on export of goods is processed and disbursed by Customs.

(b) As per Rule 96(1) of the CGST Rules, 2017, the Shipping Bill filed by an exporter is deemed to be an application for refund of integrated tax paid on the goods exported out of India and such application is deemed to have been filed only when (Rule 96 of CGST Rules, 2017):

(i) the person in charge of the conveyance carrying the export goods duly files an export manifest or an export report covering the number and the date of Shipping Bills or Bills of Export; and

(ii) the applicant has furnished a valid return in FORM GSTR-3B, as the case may be.

(c) The details of the relevant export invoices contained in FORM GSTR-1 (or Table 6A thereof) are transmitted electronically by the common portal to the system designated by the Customs and the said system shall transmit to the common portal the confirmation that the goods covered by the said invoices have been exported out of India.

(d) On receipt of information regarding furnishing of return in FORM GSTR-3B and FORM GSTR-1 from the common portal, the system designated by the Customs (or the proper officer) process the claim for refund and an amount equal to the Integrated tax paid in respect of each Shipping Bill or Bill of Export is credited to the bank account of the applicant mentioned in his registration particulars and as intimated to the Customs authorities.

3.4 Refund application in case of supply of goods to SEZ or SEZ Developer – In respect of supply of goods to a Special Economic Zone unit or a Special Economic Zone Developer, the application for refund in FORM GST RFD-01 shall be filed by the supplier of goods along with the documentary evidences mentioned in Rule 89(2) of CGST Rules, after the goods have been admitted in full in the Special Economic Zone for authorized operations, as endorsed by the specified officer of the Zone. (Rule 89(1) of CGST Rules, 2017) (Rule 89(1), (2) of CGST Rules, 2017)

3.5 Refund application in case of supply of services to SEZ- In respect of supply of services to a Special Economic Zone unit or a Special Economic Zone Developer, the application for refund in FORM GST RFD-01 shall be filed by the supplier of services along with such evidence specified in Rule 89(2) of the CGST Rules, regarding supply and receipt of services for authorized operations, as endorsed by the specified officer of the Zone. (Rule 89(1) of CGST Rules, 2017)

3.6 Refund claim in case of ‘Deemed Export’ either by recipient or supplier–

(i) Notification No. 48/2017-CT dated 18.10.2017 specifies certain supplies of goods as deemed export.

(ii) In respect of supplies regarded as deemed exports, the application may be filed in FORM GST RFD-01 by-

(a) The recipient of deemed export supplies; or

(b) The supplier of deemed export supplies in cases where the recipient does not avail of input tax credit on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund.

(iii) In case such refund is sought by the supplier of deemed export supplies, the documentary evidences specified in Notification No. 49/2017-CT dated 18.10.2017 are required to be furnished, which includes acknowledgment by the jurisdictional Tax Officer of the Advance Authorisation holder or Export Promotion Capital Goods (EPCG) Authorisation holder, as the case may be, about the receipt of the deemed export supplies or a copy of the tax invoice under which such supplies have been made by the supplier, duly signed by the recipient Export Oriented Unit (EOU) acknowledging the receipt of deemed export supplies, an undertaking by the recipient of deemed export supplies that he shall not claim the refund in respect of such supplies and that no input tax credit on such supplies has been availed by him.

(iv) In case the refund is filed by the recipient of deemed export supplies, an undertaking by the supplier of deemed export supplies to the extent that he shall not claim the refund in respect of such supplies is also required to be furnished.

(v) The procedure regarding procurement of supplies of goods from DTA by Export Oriented Unit (EOU) / Electronic Hardware Technology Park (EHTP) Unit / Software Technology Park (STP) Unit/Bio Technology Parks (BTP) Unit under deemed export as laid down in Circular No. 14/14/2017-GST dated 06.11.2017 needs to be complied with.

(vi) As per the provisions of Rule 89(2)(g) of the CGST Rules, 2017, the statement 5B of FORM GST RFD-01 is required to be furnished for claiming refund on supplies declared as deemed exports.(Rule 89(2)(g) of CGST Rules, 2017)

(vii) Rule 89(4A) of CGST Rules, provides for refund of ITC availed in respect of other inputs or input services used in making zero-rated supply of goods or services or both, where the supplier has availed benefit of Notification No. 48/2017-CT dated 18.10.2017. (Rule 89 (4A) of CGST Rules, 2017)

(viii)Rule 89(4B) of CGST Rules, provides for grant of refund of input tax credit availed in respect of inputs received for export of goods and the input tax credit availed in respect of other inputs or input services to the extent used in making such export of goods, to the exporter, on which supplier has availed benefit under Notification No. 40/2017-Central Tax (Rate) dated 23.10.2017 or Notification No. 41/2017-Integrated Tax (Rate) dated 23.10.2017, or when the exporter has himself availed the benefit of duty/tax free procurement under the Notification No. 78/2017-Customs dated 13.10.2017 or Notification No. 79/2017-Customs dated 13.10.2017. (Rule 89(2)(g), (4B) of CGST Rules, 2017)

3.7 Refund of advance tax by Casual or Non-resident taxable person- Refund of any amount, after adjusting the tax payable by the applicant out of the advance tax deposited under Section 27 of the CGST Act (casual taxable person or non-resident taxable person) at the time of registration, shall be claimed by way of filing application in FORM GST RFD-01 only after the last return required to be furnished by him has been so furnished (Rule 89(1) of CGST Rules, 2017) (Section 27 of CGST Act, 2017) (Rule 89(1) of CGST Rules, 2017)

3.8 Refund claims on account of ‘inverted duty structure’–

(i) Refund of unutilized ITC in case of ‘inverted tax structure’, as provided in Section 54(3) of the CGST Act, 2017 is available where ITC remains unutilized even after setting off of available ITC for the payment of output tax liability. (Section 54(3) of CGST Act, 2017)

(ii) Refund claim in respect of unutilized input tax credit, accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies) has to be made electronically in FORM GST RFD-01 for a tax period or by clubbing tax periods.

(iii) The refund claim for a tax period may be filed only after filing the details in FORM GSTR-1 for the said tax period.

(iv) It should be ensured that a valid return in FORM GSTR-3B has been filed for the last tax period before the one in which the refund application is being filed.

4. PROCEDURE AND CONDITIONS FOR FILING REFUND CLAIM

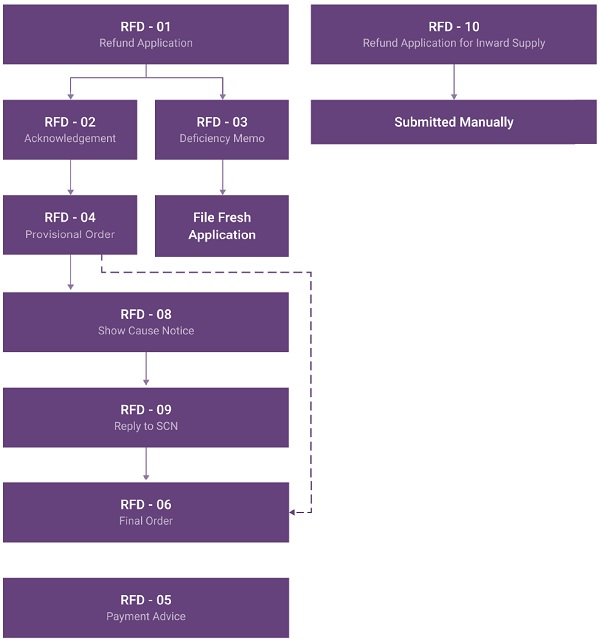

4.1 FORM GST RFD-01 shall be filled on the common portal by an applicant for the purpose of refund and uploaded with supporting documents, as provided in Annexure-A of CBIC Circular No. 125/44/2019 – GST dated 18-112019 read with Circular No. 197/09/2023-GST, dated 17.07.2023.

4.2 In case a Deficiency Memo has been issued, the applicant has to fi le a fresh refund application as the refund application with deficiencies would not be processed.

4.3 Debit to Electronic Cash Ledger if refund claimed from Electronic Cash Ledger–

(i) If a person has claimed refund of any amount from the balance in Electronic Cash Ledger then the said amount shall be first debited in the Electronic Cash Ledger. (Rule 87(10) of CGST Rules, 2017)

(ii) The debit in Electronic Cash Ledger is required as on sanction, the refund will be credited to the bank account of the applicant.

(iii) Refund from balance in Electronic Cash Ledger can be made without limitation of time. (Section 54(1) of CGST Act)

(iv) If the refund so claimed is rejected, either fully or partly, the amount equivalent to the amount rejected shall be credited, to the Electronic Cash Ledger by the Proper Officer by an order made in FORM GST PMT-03. (Rule 87(11) of CGST Rules, 2017)

4.4 Debit to Electronic Credit Ledger if refund of Input Tax Credit (ITC) claimed under Section 54 of CGST Act –

(i) If a registered person has claimed refund of any unutilized ITC amount from the Electronic Credit Ledger in accordance with the provisions of Section 54 of CGST Act (refund in case of zero rated supply or inverted tax structure), the amount to the extent of the claim shall be debited in the said ledger at the time of filing the refund claim. (Rule 86(3) of CGST Rules, 2017)

(ii) In case of refund claim of ITC pertaining to export of goods or services or supplies to SEZ, the amount is required to be debited at the time of filing refund claim, as the amount will be refunded to the person by crediting his bank account.

4.5 Procedure for re-credit of amount erroneously refunded in Electronic Credit Ledger – Procedure for re-credit of amount erroneously refunded has been specified in Circular No. 174/06/2022-GST dated 6-7-2022, which is as follows-

(i) The taxpayer shall deposit the amount of erroneous refund along with applicable interest and penalty, wherever applicable, through FORM GST DRC-03 by debit of amount from Electronic Cash Ledger. While making the payment through FORM GST DRC-03, the taxpayer should clearly mention the reason for making payment in the text box as ‘deposit of erroneous refund of unutilised ITC’, or ‘deposit of erroneous refund of IGST’ obtained in contravention of Rule 96(10) of the CGST Rules. (Rule 96(10) of CGST Rules, 2017)

(ii) The taxpayer has to make a written request, in format prescribed, to jurisdictional Proper Officer to re-credit the amount equivalent to the amount of refund paid back in cash, to Electronic Credit Ledger.

(iii) If the Proper Officer is satisfied that the full amount of erroneous refund along with applicable interest and penalty, has been paid by the taxpayer in FORM GST DRC-03 by way of debit in Electronic Cash Ledger, he shall re-credit the amount in Electronic Credit Ledger, equivalent to the amount of erroneous refund so deposited by the registered person. An order in FORM GST PMT-03A has to be passed, preferably within a period of 30 days from the date of receipt of request for re-credit of erroneous refund amount so deposited or from the date of payment of full amount of erroneous refund along with applicable interest, and penalty, whichever is later.

4.6 A refund claim for a particular tax period can be filed only after furnishing all the returns in FORM GSTR-1 and FORM GSTR-3B, which were due to be furnished on or before the date on which the refund application is being filed. However, in case of a claim for refund filed by a Composition Taxpayer, a Non-Resident taxable person, or an Input Service Distributor (ISD), furnishing of returns in FORM GSTR-1 and FORM GSTR-3B is not required. Instead, the applicant should have furnished returns in FORM GSTR-4 (along with FORM GST CMP-08), FORM GSTR-5 or FORM GSTR-6, as the case may be, which were due to be furnished on or before the date on which the refund application is being filed.

4.7 Circular No. 188/20/2022-GST dated 27-12-2022, prescribes the manner of filing refund claim by unregistered persons in the following situations-

(i) Unregistered buyers, who had entered into an agreement/contract with a builder for supply of services of construction of flats/building, etc. and had paid the amount towards consideration for such service, either fully or partially, along with applicable tax, had to get the said contract/agreement cancelled subsequently due to non-completion or delay in construction activity in time or any other reasons.

(ii) Long-term insurance policies where premium for the entire period of term of policy is paid upfront along with applicable GST and the policy is subsequently required to be terminated prematurely due to some reasons.

The application for refund is required to be filed in FORM GST RFD-01 on the common portal under the category ‘Refund for unregistered person’. The applicant is required to upload statement 8 (in pdf format) and all the requisite documents as per the provisions of sub-rule (2) of rule 89 of the CGST Rules. The applicant should also upload the certificate issued by the supplier in terms of clause (kb) of sub-rule (2) of rule 89 of the CGST Rules, 2017, and any other document(s) to support his claim that he has paid and borne the incidence of tax and that the said amount is refundable to him.

4.8 Functionality has been made available on the common portal, which allows unregistered persons to take a temporary registration and apply for refund under the category ‘Refund for Unregistered person’. Statement 8 has been inserted in FORM GST RFD-01 to provide for the documents required to be furnished along with the application of refund by the unregistered persons and the statement has to be uploaded along with the refund application.

4.9 In cases where the amount paid back by the supplier to the unregistered person on cancellation/termination of agreement/contract for supply of services is less than the amount paid by such unregistered person to the supplier, only the proportionate amount of tax involved in such amount paid back shall be refunded to the unregistered person.

4.10 The applicant can withdraw the application for refund filed in FORM GST RFD-01, at any time before issuance of provisional refund sanction order in FORM GST RFD-04 or final refund sanction order in FORM GST RFD-06 or payment order in FORM GST RFD-05 or refund withhold order in FORM GST RFD-07 or notice in FORM GST RFD-08, by filing an application in FORM GST RFD-01W (CGST Rule 90(5) of CGST Rules, 2017). On submission of application for withdrawal of refund in FORM GST RFD-01W, any amount debited from Electronic Credit Ledger or Electronic Cash Ledger, as the case may be, while filing application for refund, shall be credited back to the ledger from which such debit was made.

5. RELEVANT DATE FOR FILING THE REFUND CLAIM

5.1 The relevant date provision embodied in Section 54 of the CGST Act, 2017, provision contained in Section 77 of the CGST Act, 2017 and the requirement of submission of relevant documents as listed in Rule 89(2) of CGST Rules, 2017 is an indicator of the various situations that may necessitate a refund claim. The GST law requires that every claim for refund is to be filed within 2 years from the relevant date. (Rule 89(2) of CGST Rules, 2017) (Section 54, 77 of CGST Act, 2017)

5.2 The ‘relevant date’ in respect of the certain cases would be as under –

(i) In the case of goods exported out of India where a refund of tax paid is available in respect of the goods themselves or the inputs or input services used in such goods –

(a) if the goods are exported by sea or air, the date on which the ship or the aircraft in which such goods are loaded, leaves India; or

(b) if the goods are exported by land, the date on which such goods pass the frontier; or

(c) if the goods are exported by post, the date of dispatch of goods by Post Office concerned to a place outside India.

(ii) In case of supply of goods regarded as deemed exports where a refund of tax paid is available in respect of the goods, the date on which the return relating to such deemed exports is filed.

(iii) In case of zero-rated supply of goods or services or both to a Special Economic Zone Developer or a Special Economic Zone unit where a refund of tax paid is available in respect of such supplies themselves, or as the case may be, the inputs or input services used in such supplies, the relevant date is the due date for furnishing of return under Section 39 in respect of such supplies. (Section 39 of CGST Act, 2017)

(iv) In case of services exported out of India where a refund of tax paid is available in respect of services themselves or, as the case may be, the inputs or input services used in such services, the relevant date would be the date of –

(a) receipt of payment in convertible foreign exchange or in Indian rupees wherever permitted by RBI, where the supply of service had been completed prior to the receipt of such payment; or

(b) issue of invoice, where payment for the service had been received in advance prior to the date of issue of the invoice.

(v) In case where the tax becomes refundable as a consequence of judgement, decree, order or direction of Appellate Authority, Appellate Tribunal or any Court, the date of communication of such judgement, decree, order or direction would be the relevant date.

(vi) In the case of refund of unutilised input tax credit under clause (ii) of the first proviso to Section 54(5) of the CGST Act, the due date for furnishing of return under Section 39 of the CGST Act for the period in which such claim for refund arises, would be the relevant date. (Section 54(5) & 39 of CGST Act, 2017)

(vii) In the case where tax is paid provisionally under CGST Act or the rules made thereunder, the date of adjustment of tax after the final assessment thereof would be the relevant date.

(viii) In the case of a person, other than the supplier, the date of receipt of goods or services by such person would be the relevant date.

(ix) In any other case, the date of payment of tax.

5.3 The time period from the date of filing of the refund claim in FORM GST RFD-01 till the date of communication of the deficiencies in FORM GST RFD-03 by the Proper Officer, shall be excluded from the period of two years, as specified under Section 54(1) of CGST Act, in respect of any such fresh refund claim filed by the applicant after rectification of the deficiencies. (Section 54(1) of CGST Act, 2017)

5.4 CBIC, vide Circular No. 166/22/2021-GST dated 17-11-2021, has clarified that time limit prescribed under Section 54(1) of CGST Act is not applicable to refund claim for excess balance in Electronic Cash Ledger. This also applies to TDS/TCS deposited in Electronic Cash Ledger.

5.5 In respect of refund claims under Section 77 of the CGST Act of tax paid in respect of a transaction considered to be an Intra-State supply, which is subsequently held to be an Inter-State supply, an application is required to be filed electronically in FORM GST RFD-01 through the common portal, before the expiry of a period of two years from the date of payment of the tax on the supply, either directly or through a Facilitation Centre notified by the Commissioner. (Rule 89(1A) to CGST Rules) (Section 77 of CGST Act, 2017) (Rule 89(1A) of CGST Rules, 2017)

6. DOCUMENTS TO BE FILED WITH REFUND CLAIM

As per Rule 89(2) of CGST Rules, 2017, the application for refund under Rule 89(1) of the CGST Rules, shall be accompanied by any of the following documentary evidences, as applicable to the individual claim, to establish that a refund is due to the applicant – (Rule 89(1)(2) of CGST Rules, 2017)

(i) The reference number of the order and a copy of the order passed by the Proper Officer or an Appellate Authority or Appellate Tribunal or Court, resulting in such refund or reference number of the payment of the amount specified in Section 107(6) and Section 112(8) claimed as refund. (Section 107(6) & 112(8) of CGST Act, 2017)

(ii) In a case where the refund is on account of export of goods, other than electricity, a statement containing the number and date of shipping bills or bills of export and the number and date of relevant export invoices.

(iii) In case where refund is on account of export of electricity, a statement containing the number and date of the export invoices, details of energy exported, tariff per unit for export of electricity as per agreement, along with the copy of statement of scheduled energy for exported electricity by Generation Plants issued by the Regional Power Committee Secretariat as a part of the Regional Energy Account (REA) under Regulation 2(l)(nnn) of the Central Electricity Regulatory Commission (Indian Electricity Grid Code) Regulations, 2010 and the copy of agreement detailing the tariff per unit.

(iv) In a case where the refund is on account of export of services, a statement containing the number and date of invoices and the relevant Bank Realization Certificates or Foreign Inward Remittance Certificates, as the case may be.

(v) In case of supply of goods made to a Special Economic Zone unit or a Special Economic Zone Developer, along with a declaration to the effect that tax has not been collected from the Special Economic Zone (SEZ) unit or the Special Economic Zone (SEZ) developer, a statement containing the number and date of invoices as prescribed in Rule 46, along with the evidence that the goods have been admitted in full in the SEZ, by way of endorsement specified in the first proviso (a) to Rule 89(1) of CGST Rules. (Rule 46, 89(1) of CGST Rules, 2017)

(vi) Where the refund is on account of supply of services made to a Special Economic Zone unit or a Special Economic Zone Developer, along with a declaration to the effect that tax has not been collected from the Special Economic Zone (SEZ) unit or the Special Economic Zone (SEZ) developer, a statement containing the number and date of invoices, the evidence regarding receipt of services for authorized operations, by way of endorsement specified in the first proviso (b) to Rule 89(1), the details of payment along with proof thereof made by the recipient to the supplier for authorized operations, as defined under the SEZ Act, 2005.

(vii) Where the refund is on account of Deemed Exports, a statement containing the number and date of 101 | Handbook of GST Law and Procedures invoices along with such other evidence, as notified in this behalf.

(viii) In a case where the claim pertains to refund of any unutilized input tax credit under Section 54(3) of the CGST Act, where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (inverted duty structure), other than nil-rated or fully exempt supplies, a statement containing the number and date of invoices received and issued during a tax period. (Section 54(3) of CGST Act, 2017)

(ix) In a case where the refund arises on account of finalisation of provisional assessment, the reference number of the final assessment order and a copy of the said order.

(x) A statement showing details of transactions considered as intra-state supply subsequently held as interstate supply.

(xi) A statement showing the details of the amount of claim on account of excess payment of tax.

(xii) In a case where the refund is claimed by an unregistered person where the agreement or contract for supply of service has been cancelled or terminated, a statement containing the details of invoices viz. number, date, value, tax paid and details of payment, in respect of which refund is being claimed along with copy of such invoices, proof of making payment to the supplier, a certificate issued by the supplier to the effect that he has paid tax in respect of the invoices on which refund is being claimed by the applicant, the copy of agreement or registered agreement or contract entered with the supplier for supply of service, the letter issued by the supplier for cancellation or termination of agreement or contract for supply of service, details of payment received from the supplier against cancellation or termination of such agreement along with proof thereof.

(xiii) A declaration to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person, in a case where the amount of refund claimed does not exceed two lakh rupees. However, a declaration is not required to be furnished in respect of cases covered under Section 54(8)(a), 54(8)(b), 54(8)(c) or 54(8)(d) of CGST Act, 2017, i.e. refund of tax paid on export of goods and/or services or inputs and input services used in making such exports, refund of unutilized ITC accumulated on account of zero rated supplies and on account of inverted tax structure, refund of tax paid on non-supply or incomplete supply or refund voucher cases and refund of tax paid on intra-state supply, which is later held as inter-state supply or vice- versa.(Section 54(8)(a), (b) (c) & (d) of CGST Act, 2017)

(xiv) A Certificate in Annex 2 of FORM GST RFD-01 issued by a Chartered Accountant or a Cost Accountant to the effect that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person, in a case where the amount of refund claimed exceeds two lakh rupees. Such a declaration is not required to be furnished in respect of cases covered under said Sections 54(8)(a), 54(8) (b), 54(8)(c) or 54(8)(d) of CGST Act, 2017 and in cases where refund is claimed by an unregistered person who has borne the incidence of tax.

7. EXAMINATION OF REFUND APPLICATIONS AND THE ACTION TO BE TAKEN BY OFFICERS

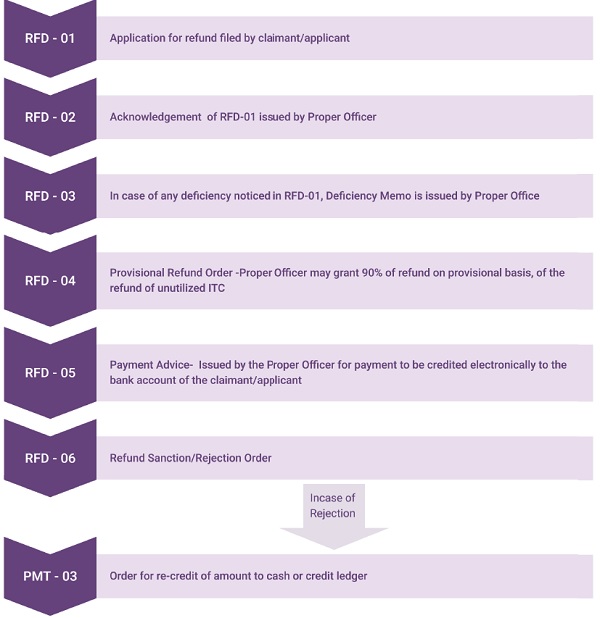

7.1 The Deputy/Assistant Commissioner of Central Tax is designated as ‘Proper Officer’ for the purpose of granting refund and all related actions specified under Section 54 of CGST Act, 2017 and Rules 89 to 96 of CGST Rules, 2017, like issuance of acknowledgement, issuance of Deficiency Memo, issuance of Provisional Refund Sanction order, Payment order, Final order and Refund Withhold order. (Section 54 of CGST Act, 2017) (Rule 89 to 96 of CGST Rules, 2017)

7.2 Refund Application in FORM GST RFD-01 will be filed by the applicant on the common portal for the purpose of refund, along with supporting documents, as provided in Annexure-A of CBIC Circular No. 125/44/2019-GST dt. 18-11-2019.

7.3 The Application Reference Number (ARN) will be generated only after the applicant has completed the process of filing the refund application in FORM GST RFD-01, and has completed uploading of all the relevant documents and wherever required, the amount has been debited from the Electronic Credit/Cash Ledger.

7.4 Acknowledgement or a Deficiency Memo should be issued within the stipulated period of 15 days, starting from the date of generation of ARN. The acknowledgement for the complete application in FORM GST RFD-02 would be issued electronically by the jurisdictional tax officer based on the documents so received from the common portal.

7.5 As per Sub-rule (3) of Rule 90 of the CGST Rules, 2017 the Deficiency Memo in FORM GST RFD-03 has to be issued within 15 days from the date of ARN, by the Proper Officer, communicating the deficiencies noticed during preliminary scrutiny of the Refund claim. (Rule 90(3) of CGST Rules, 2017)

7.6 Once an acknowledgement has been issued in relation to a refund application, no Deficiency Memo, on any grounds, can be subsequently issued for the said application.

7.7 After a Deficiency Memo has been issued, the refund application would not be further processed and a fresh application will have to be filed by the applicant. The applicant is required to rectify the deficiencies highlighted in Deficiency Memo and file fresh refund application electronically in FORM GST RFD-01 again for the same period and this application would have a new and distinct ARN. (CBIC Circular No. 125/4/2019-GST dated 18.11.2019).

7.8 The time period, from the date of filing of the refund claim in FORM GST RFD-01 till the date of communication of the deficiencies in FORM GST RFD-03 by the Proper Officer, shall be excluded for computing the period of two years, as specified under Section 54(1) of CGST Act, in respect of any fresh refund claim filed by the applicant consequent to issuance of the Deficiency Memo. (Proviso to Rule 90(3) of CGST Rules, 2017) (Section 54(1) of CGST Act, 2017)

7.9 Any amount of input tax credit/cash debited from Electronic Credit/Cash Ledger would be re-credited automatically once the Deficiency Memo has been issued.

7.10 In terms of Section 54(6) of CGST Act, 2017, the Proper Officer may grant 90% of refund of unutilized input tax credit on provisional basis, claimed on account of zero-rated supply of goods and services, subject to the conditions specified in Rule 91 of the CGST Rules, 2017. The Proper Officer shall make an order in FORM GST RFD-04 within seven days from the date of issuance of acknowledgement in FORM GST RFD-02. (Section 54(6) of CGST Act, 2017) (Rule 91 of CGST Rules, 2017)

7.11 The payment order in FORM GST RFD-05 shall be issued by the Proper Officer and the same shall be credited electronically to the bank account of the applicant mentioned in the registration particulars. The payment order is required to be revalidated in case if the refund is not disbursed within the same financial year in which the payment advice was issued.

7.12 On examination if the refund application is found in order and the Proper Officer is satisfied that a refund under Section 54(5) of CGST Act, 2017, is due and payable to the applicant then he will pass an order in FORM GST RFD-06, sanctioning the entitled amount of refund, mentioning therein the amount of refund granted on provisional basis, if any, amount adjusted against any outstanding demand and the balance amount refundable. The amount determined as refundable shall be credited to the ‘Consumer Welfare Fund’, except in cases mentioned in Section 54(8) of the CGST Act, 2017 and where it is proved that the burden of tax is not passed on to another person. Before sanction of refund the data sent by DGARM is to be checked. (Section 54(5), 54(8) of CGST Act, 2017)

7.13 (a) If a registered person claims refund of any amount of tax wrongly paid or paid in excess for which debit has been made from the Electronic Credit Ledger, the said amount, if found admissible, shall be re-credited to the Electronic Credit Ledger by the Proper Officer by an order made in FORM GST PMT-03. (Rule 86(4A) of CGST Rules, 2017) (CBIC Circular No.135/05/2020-GST dated 31-3-2020). The functionality of FORM GST PMT-03A allows Proper Officer to re-credit the amount in the Electronic Credit Ledger of the taxpayer. (Rule 86(4A), 86(4B) of CGST Rules, 2017)

(b)As per Rule 86(4B) of CGST Rules, 2017, if the registered person deposits the amount in respect of the following categories of refund sanctioned erroneously, along with interest and penalty, wherever applicable, through FORM GST DRC-03, by debiting the Electronic Cash Ledger, on his own or on being pointed out, an amount equivalent to the amount of erroneous refund deposited by the registered person shall be re-credited to the Electronic Credit Ledger by the Proper Officer by an order made in FORM GST PMT-03A –

(a) Refund of IGST obtained in contravention of Rule 96(10) of CGST Rules, 2017.

(b) Refund of unutilized ITC on account of export of goods/services without payment of tax. (Rule 96(10) of CGST Rules, 2017)

(c) Refund of unutilized ITC on account of zero-rated supply of goods/services to SEZ developer/Unit without payment of tax.

(d) Refund of unutilized ITC due to inverted tax structure.

7.14 Time limit for deciding refund claim – The order under which the refund application is decided, either rejecting or accepting refund claim, shall be issued by the Proper Officer within sixty days from the date of receipt of application complete in all respects. – Section 54(5) of CGST Act, 2017.

7.15 If any tax refundable under Section 54(5) of the CGST Act, 2017, to any applicant is not refunded within sixty days from the date of receipt of application, interest at the specified rate is payable for the period of delay beyond sixty days, from the date of receipt of such application till the date of refund of such tax. (Section 56 of CGST Act, 2017) (Section 54(5) & 56 of CGST Act, 2017)

7.16 No refund if amount less than Rs. 1,000/- – No refund shall be paid to an applicant if the amount of refund is less than Rupees One Thousand. The limit of Rupees One Thousand shall be applied for each tax head separately and not cumulatively. (CBIC Circular No. 125/44/2019 – GST dated 18-11-2019). (Section 54(14) of CGST Act, 2017)

7.17 Powers to withhold refund in certain cases – Section 54(11) of the CGST Act, 2017 provides that where an order giving rise to a refund is the subject matter of an appeal or further proceedings or where any other proceedings under CGST Act, 2017 is pending and the Proper Officer or the Commissioner is of the opinion that grant of such refund is likely to adversely affect the revenue in the said appeal or other proceedings on account of illicit activity or fraud committed, he may pass an order in Part A of FORM GST RFD-07, providing the reasons for withholding of the refund amount. Once the reasons for withholding refund no more exist, such withheld refunds may be released by passing an order in Part-B of FORM GST RFD-07.

7.18 On examination of the refund application, if the Proper Officer is satisfied that the whole or any part of the amount claimed as refund is not admissible or is not payable to the applicant then he will issue a notice in FORM GST RFD-08 to the applicant.

7.19 The applicant will file reply electronically in FORM GST RFD-09, if he so desires, within 15 days of the receipt of said notice. The Proper Officer after considering the reply filed, will issue an order electronically in FORM GST RFD-06, sanctioning the amount of refund in whole or part or rejecting the refund claim, as the case may be. No claim can be rejected without giving applicant an opportunity.

7.20 Guidelines provided under Instruction No. 03/2022-GST dated 14.06.2022 and Instruction No. 04/2022-GST dated 28.11.2022 should be followed while examining the refund claims.

8. UNJUST ENRICHMENT

8.1 GST is an indirect tax whose incidence is to be borne by the consumer and hence, a presumption is always drawn that the taxpayer will shift the incidence of tax to the final consumer. It is for this reason that every claim of refund (barring specified exceptions) needs to pass the test of unjust enrichment.

8.2 Every refund claim, if sanctioned, is first transferred to the Consumer Welfare Fund.

8.3 The test of unjust enrichment is inapplicable in case of refund of accumulated ITC, refund on account of exports, refund of payment of wrong tax (Integrated tax instead of Central tax plus State tax and vice versa), refund of tax paid on a supply which is not provided or where refund voucher is issued or if the applicant shows that he has not passed on the incidence of tax to any other person. In all other cases the test of unjust enrichment needs to be satisfied for the claim to be paid to the applicant.

8.4 If the refund claim is less than Rupees 2 Lakhs, then a self-declaration of the applicant to the effect that the incidence of tax has not been passed to any other person will suffice to process the refund claim. For refund claims exceeding Rupees 2 Lakh, a certificate from a Chartered Accountant/ Cost Accountant has to be given.

9. POWERS TO CENTRAL GOVERNMENT TO REFUND STATE TAX AND VICE VERSA.

During the initial days after introduction of GST taxation system a taxable person under jurisdiction of Central Government had to go to State/Union Territory GST authorities to get refund of SGST/UTGST if Central Government Officers sanction refund. Subsequent to insertion of Section 54(8A) of CGST Act, 2017, a system of integrated refund has been introduced. Thus, officer of CGST/SGST/UTGST will sanction and disburse both CGST and SGST/UTGST and vice-versa, in such manner and within such time, as prescribed. (Section 54(8A) of CGST Act, 2017)

10. DISBURSAL OF REFUNDS OF ALL TAXES BY JURISDICTIONAL OFFICER ONLY.

10.1 CBIC Circular No. 125/44/2019 – GST dated 18-11-2019 has clarified that in respect of a refund application assigned to a Central Tax Officer, both the sanction order (FORM GST RFD-04/06) and the corresponding payment order (FORM GST RFD-05) for the sanctioned refund amount, under all tax heads, shall be issued by the Central Tax Officer only and vice-versa.

10.2 If a refund application is electronically transmitted to the wrong jurisdictional officer, he/she shall reassign it to the correct jurisdictional officer electronically as soon as possible, but not later than three working days, from the date of generation of the ARN. Deficiency Memo shall not be issued in such cases merely on the ground that the applications were received electronically in the wrong jurisdiction. Facility to reassign such refund applications is already available with the Commissioner or the officer(s) authorized by him.

10.3 The refund application in FORM GST RFD-01 filed by migrated taxpayers should be forwarded for processing by the common portal to the jurisdictional Proper Officer of the tax authority from which the taxpayer has originally migrated. Such officers will continue to process these applications up to the stage of issuance of final order in FORM GST RFD-06 and the related payment order in FORM GST RFD-05 even if the applicant is assigned to the counterpart tax Authority while the refund claim is under processing. However, if such an applicant gets assigned to one of the tax authorities after generation of the ARN and a Deficiency Memo gets issued for the refund application submitted by him, then the re-submitted refund application, after correction of deficiencies, shall be treated as a fresh refund application and shall be forwarded to the jurisdictional Proper Officer of the tax authority to which the taxpayer has now been assigned, irrespective of which authority handled the initial refund claim and issued the Deficiency Memo.

11. ADJUDICATION OF SCN BY PROPER OFFICER SANCTIONING REFUND

11.1 The proper officer for sanctioning refund will also be the proper officer for adjudicating the cases relating to refund application.

11.2 The notice shall be adjudicated following the principles of natural justice and an order shall be issued in FORM GST RFD-06 under Section 54 of the CGST Act, 2017.

11.3 FORM GST RFD-08 and FORM GST RFD-06, are to be considered as show cause notice and adjudication order, respectively, under both Section 54 (for rejection of refund) and Section 73/74 of the CGST Act, 2017, as the case may be (for recovery of erroneous refund).

12. FUNCTIONS OF RANGE AND DIVISION OFFICERS IN REFUND PROCESSING

The Division/Range Officer is required to undertake the following functions:

(i) Scrutiny of Application for refund with prescribed documents as per Chapter X of CGST Act, 2017 and Chapter IX of CGST Rules, 2017.

(ii) The acknowledgement for the complete application in FORM GST RFD-02 to be issued electronically based on the documents so received from the common portal as per Rule 90 of CGST Rules, 2017.

(iii) In case there is any deficiency in the application, a Deficiency Memo has to be issued in FORM GST RFD-03, within 15 days from the date of filing a refund application as per Rule 90 of CGST Rules, 2017.

(iv) 90% of refund of the refund of unutilized input tax credit claimed on account of zero-rated supply of goods and services has to be given on provisional basis, subject to the conditions specified in Rule 91 of the CGST Rules, 2017, in FORM GST RFD-04 within seven days from the date of issuance of acknowledgement in FORM GST RFD-02.

(v) The payment order in FORM GST RFD-05 shall be issued by the Proper Officer and the same shall be credited electronically to the bank account of the applicant mentioned in the registration particulars.

(vi) On examination of the refund application, if the whole or any part of the amount claimed as refund is not admissible or is not payable to the applicant then notice in FORM GST RFD-08 is to be issued to the applicant, as specified in Rule 92 of CGST Rules, 2017.

(vii) After considering the reply filed, an order may be issued electronically in FORM GST RFD-06, sanctioning the amount of refund in whole or part or rejecting the refund claim, as the case may be, as per Rule 92 of CGST Rules, 2017.

(viii) If a registered person claims refund of any amount of tax wrongly paid or paid in excess for which debit has been made from the Electronic Credit Ledger, the said amount, if found admissible, shall be re-credited to the Electronic Credit Ledger by the Proper Officer by an order made in FORM GST PMT-03. (Rule 86(4A) of CGST Rules, 2017)

(ix) FORM RFD-07 has to be issued by the officer in cases where refund claimed by the applicant is fully adjusted against any outstanding demands (PART A) or refund is withheld due to certain reasons (PART B).

(x) If any interest is due and payable to applicant under Section 56 of CGST Act, 2017, the officer shall make an order along with a payment advice in FORM GST RFD-05, as specified in Rule 94 of CGST Rules, 2017.

(xi) The proper officer has to ensure that the registered person availing the option to supply goods or services for export without payment of Integrated tax has furnished a bond or a Letter of Undertaking in FORM GST RFD-11, binding himself to pay the tax due along with the interest specified as per Section 50(1) of CGST Act, 2017.

(xii) The Range Officer has to check the ITC eligibility and data of zero rated supplies, if such verification is required.

(xii) The records of the receipt of refund applications received and disposed of along with all relevant details are to be maintained by Division/Range Officer.

13. SOPS ISSUED IN RESPECT OF REFUND

(I) Instruction No. 3/2022-GST, dated 14.06.2022 pertains to procedure relating to sanction, post-audit and review of refund claims.

(II) Instruction No. 4/2022-GST dated 28.11.2022 pertains to the manner of processing and sanction of IGST refunds, withheld in terms of clause (c) of sub-rule (4) of Rule 96, transmitted to the jurisdictional GST authorities under sub-rule (5A) of Rule 96 of the CGST Rules, 2017.

(III) Circular No.131/1/2020-GST dated 23.01.2020 issued to CGST formations provides for the procedure to be followed for verification of risky exporters and their suppliers.

(IV) SOP vide CBEC-20/16/07/2020-GST dated 20.05.2020 is regarding changes in SOP dated 23.01.2020 for verification of IGST refunds and other related aspects.

14. CIRCULARS ISSUED BY CBIC ON ISSUES RELATED TO REFUNDS

(I) Circular No. 14/14/2017-GST dated 06.11.2017 – Procurement of goods from DTA by EOU/EHTP/STP/ BTP

(II) Circular No. 125/44/2019-GST dated 18.11.2019 – Electronic Refund process and single disbursement.

(III) Circular No.134/04/2020-GST dated 23.03.2020 – Refund in respect of companies under Insolvency & Bankruptcy Code, 2016.

(IV) Circular No. 135/05/2020-GST dated 31.03.2020 – Clarification on refund related issues.

(V) Circular No.139/09/2020-GST dated 10.06.2020 – Clarification on refund related issues.

(VI) Circular No.147/03/2021-GST dated 12.03.2021 – Refund claim by recipient of deemed export supply, zero-rated supplies.

(VII) Circular No.166/22/2021-GST dated 17.11.2021 – No time limit for refund of balance in Cash Ledger.

(VIII) Circular No. 160/16/2021-GST dated 20.09.2021 – Clarification on restriction imposed under proviso to Section 54(3) of CGST Act, 2017

(IX) Circular No. 173/05/2022-GST dated 06.07.2022 – Clarification on refund claim under Inverted Duty Structure.

(X) Circular No.174/06/2022-GST dated 06.07.2022 – Re-credit of sanctioned excess or erroneous refund in Electronic Credit Ledger

(XI) Circular No.176/08/2022-GST dated 06.07.2022 – Refund of taxes paid on inward supply of indigenous goods when supplied to outgoing international tourist.

(XII) Circular No. 188/20/2022-GST dated 27.12.2022 – Refund for unregistered person.

(XIII) Circular No.197/09/2023-GSTdated17.07.2023 – Refund of accumulated input tax credit.

FLOW CHART FOR REFUND APPLICATION

*****

Source: Handbook of GST Law and Procedures for Departmental Officers issued by Ministry of Finance