Applicability : Whenever there is a Movement of Goods of Consignment Value > Rs. 50,000.

– In relation to Supply

– In relation to Other Than Supply

– Inward Supply from Unregistered Person

Movement Of Goods : E-way Bill is not required for all transactions, only required for those which involves movement of goods whether by way of Supply or not.

Some transactions through involving movement of Goods are deemed to be a supply of Services such as Leasing of Goods, supply of food and beverages etc, so in these cases, E- Way bills are required.

Consignment Value : —- Value determined as per Sec 15 (declared in Invoice/BOS/Delivery Challan)

Exceptional Situatuions, where EWB needs to be issued even if the Value of Consignment Value is less than Rs. 50,000 :-

— Inter State Transfer of Goods by Principal to Job Worker

— Inter State Transfer of Handicraft Goods by a Person exempted from obtaining Registration

Exceptional Situatuions, where EWB is not required irrespective of there Consignment Value :-

– 8 Items listed in annexure – Non Motorised Conveyance

– Port to Port Transfer – State List of EWB Exemption

– Goods Exempt from GST – 6 Items of Non GST Goods

– Empty Cargo – Empty LPG Cylinder

– Wheightment and Back less than 20KMS

– Schedule III Goods – Transport under Custom Control

– Transit Cargo –Nepal/ Bhutan – Transpot between CSD Stations/Nuclear Power Co.

– Transport under Min of Defense Control & Formation

– Railway Transport by CG/SG/LA

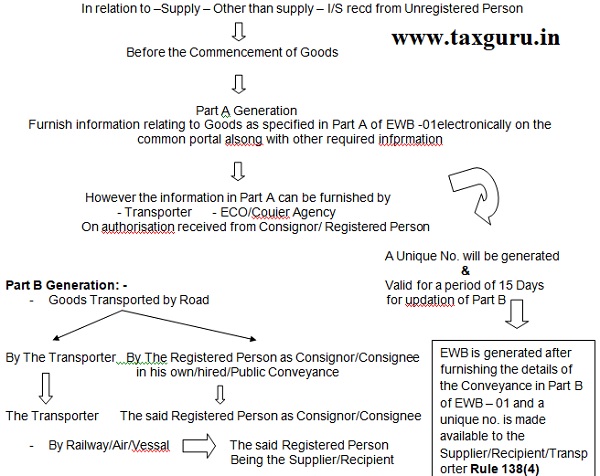

At what point of time, E-Way Bill need to be generated – Before the commencement of Goods Information to be furnished in E- Way Bill : E-Way Bill (EWB -01) shall be in Two Parts –

Part A — Information related to said Goods (Supplier & Recipient Details, Place of Delivery, Document No/Date, HSN Code, Value & Tax amount and Reason for Transportation)

Part B — Transporter Details ( Transport Document No. & Vehicle No. in case of Road Transport)

Generation of EWB by Whom –

Part A – furnished by Registered Person who cause Movement of Goods **

Part B – furnished by the Person who is transporting the Goods **

Rule 138(1) :- Every Registered Person who cause movement of goods Of Consignment Value >Rs. 50,000

Part B Generation:-

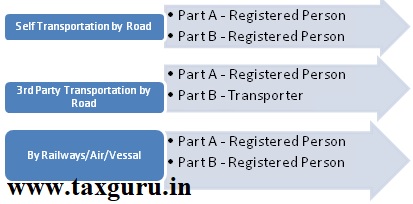

A) Where the Goods are transported by a Registered Person whether as Consignor/Consignee whether in his own/hired/public conveyance by Road, then the said Registered Person shall generate the E-Way Bill after furnishing the Information in Part B. Rule 138(2) (Self Transportation)

B) Where the E-Way Bill is not generated under R-138(2) and Goods are handed over to the Transporter for transportation of Goods by road, then the Registered Person shall furnish the information relating to the Transporter on the common portal and EWB shall be generated by the Transporter on the said portal. Rule 138(3) (3rd Party Transportation)

C) Where the goods are transported by Railway/Air/Vessal ,EWB shall be generated by the Registered Person being the Supplier/ Recipient furnish information in Part B. Rule 138(2A)

| Supplier

A |

Recipient

B |

EWB Liability |

| Registered | Registered | A or B |

| Registered | Unregistered | A |

| Unregistered | Registered | B |

| Unregistered | Unregistered | Optional for A & B but required for Transporter ** |

Who cause Movement of Goods :-

– If the Supplier/Recipient is registered and undertakes to transport the Goods, Movement is caused by the said Supplier/Recipient.

– If the Goods supplied by an Unregistered Supplier to a Registered Recipient, the Movement shall be caused by such Recipient.

Where the movement is caused by an Unregistered Person either in his own/hired conveyance or through the Transporter, then he or transporter at their option generate EWB. Proviso to Rule 138(3)

**Where neither the Consignor or Consignee generates the EWB and the value of Goods is more than Rs.50,000, it shall be the responsibility of the Transporter to generate it.

Eway bill information required