ELECTRONIC WAY BILL i.e. E-WAY BILL

In order to monitor the movements of goods for controlling any tax evasion, e-way bill system has been introduce in GST regime. Under this system wherein any registered person prior to movements of goods via conveyance would inform each transactions details to the tax department.

WHAT IS E-WAY BILL?

A e-way bill is a electronic receipt or a document issued by a carrier giving details and instruction relating to the shipment of consignment of goods and the details include:

-Name of consignor

– Consignee

-The point of origin of consignment

-Destination of consignment, route etc.

PROVISION OF E-WAY BILL:

Whenever there is a movement of goods of consignment value** exceeding rupee 50000:

√ in relation to a supply (e.g. Sale, Purchase, etc.); or

√ for reasons other than supply (e.g. Job Work, goods sent on approval basis, exhibition purpose, demo, SKD/CKD, etc); or

√ due to inward supply from an unregistered person,

The registered person who causes such movement of goods shall furnish the information relating to the said goods as specified in Part A of Form GST EWB-01 before commencement of such movement.

The pre-requisite for generation of e way bill is that the person who generate e-way bill should be –

1. A registered person on GST portal and

2. He should register on e way bill portal.

**CONSIGNMENT VALUE (RULE 138(1):

√ Consignment value of goods would be the value, determined in accordance with the provision of section 15.

√ Consignment value of goods would be the value declared in an invoice, a bill of supply or a delivery challan, as the case may be issued in respect of the said consignment.

√ Consignment value would also include central tax, state or union territory tax, integrated tax and cess charged, if any, in the document.

√ Consignment value shall exclude the value of exempt supply of goods where the invoice is issued in respect of both exempt and taxable supply of goods.

For certain specified Goods, the E-way bill need to be generated mandatorily even if the value of the consignment of Goods is less than Rs. 50,000:

√ Inter-State movement of Goods by the Principal to the Job-worker by Principal/ registered Job-worker,

√ Inter-State Transport of Handicraft goods by a dealer exempted from GST registration.

*Handicraft goods are the goods specified in Notification No. 56/2018 CT dated 23.10.2018 which exempts the casual taxable persons making inter-State taxable supplies of such handicraft goods from obtaining registration upto specified turnover limit.

DIFFERENT TYPE OF TRANSACTION ON E- WAY BILL PORTAL:

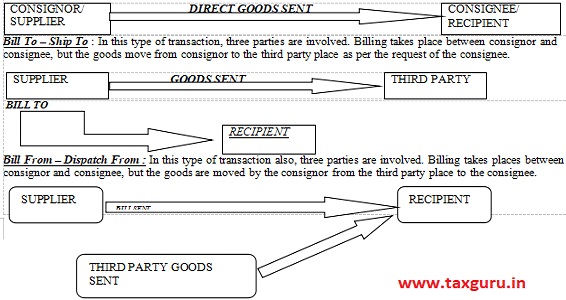

Regular This is a regular or normal transaction, where Billing and goods movement are happening between two parties – consignor and consignee. That is, the Bill and goods movement from consignor to consignee takes place directly.

Combination of both : This is the combination of above two transactions and involves four parties. Billing takes places between consignor and consignee, but the goods are moved by the consignor from the third party place to the fourth party place, as per the consignee’s request.

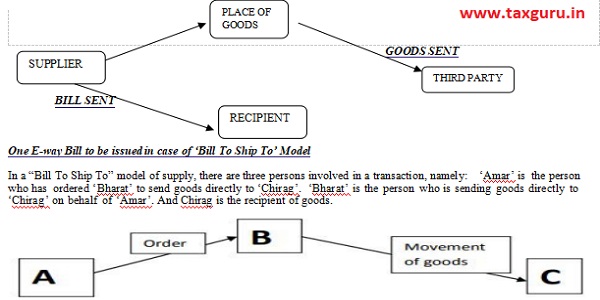

One E-way Bill to be issued in case of ‘Bill To Ship To’ Model

In a “Bill To Ship To” model of supply, there are three persons involved in a transaction, namely:

‘Amar’ is the person who has ordered ‘Bharat’ to send goods directly to ‘Chirag’. ‘Bharat’ is the person who is sending goods directly to ‘Chirag’ on behalf of ‘Amar’. And Chirag is the recipient of goods.

In this complete scenario. two supplies are involved and accordingly two tax invoices are required to be issued:

Invoice -1: which would be issued by ‘Bharat’ to ‘Amar’?

Invoice -2: which would be issued by ‘Amar’ to ‘Chirag’.

It is clarified that as per the CGST Rules, 2017, either Amar or Bharat can generate the e-Way Bill but it may be noted that only one e-Way Bill is required to be generated [Press Release dated 23.04.2018]

Part of E-way bill: An e-way bill Form GST EWB-01 contains two parts:

| Part A [comprising of details of GSTIN of supplier & recipient, place of dispatch & delivery (indicating PIN Code also), document (Tax invoice, Bill of Supply, Delivery Challan or Bill of Entry) number and date, value of goods, HSN code, and reasons for transportation, etc.]to be furnished by the registered person who is causing movement of goods of consignment value exceeding ` 50,000/- | Part B (transport details) [Transporter document number (Goods Receipt Number or Railway Receipt Number or Airway Bill Number or Bill of Lading Number) and Vehicle number, in case of transport by road]: to be furnished by the person who is transporting the goods. |

Cancellation of e-way bill:

Where an e-way bill has been generated, but goods are either not transported or are not transported as per the details furnished in the e-way bill, the e-way bill may be cancelled electronically on the common portal within 24 hours of generation of the e-way bill [Rule 138(9)].

However, an e-way bill cannot be cancelled if it has been verified in transit in accordance with the provisions of rule 138B [First proviso to rule 138(9)].

Validity period of E-way bill :

| S.no. | Distance within country | Validity period from relevant date* |

| 1 | Up to 100 km | One day in cases other than Over Dimensional Cargo** |

| 2. | For every 100 km or part thereof thereafter | One additional day in cases other than Over Dimensional Cargo |

| 3. | Up to 20 km | One day in case of over dimensional cargo |

| 4. | For every 20 km or part thereof thereafter | One additional day in case of over dimensional cargo |

**Over dimensional cargo means a cargo carried as a single indivisible unit and which exceeds the dimensional limits prescribed in rule 93 of the Central Motor Vehicle Rules, 1989, made under the Motor Vehicles Act, 1988.

Who is mandatorily required to generate e-way bill?

Where the goods are transported by a registered person – whether as consignor or recipient as the consignee (whether in his own conveyance or a hired one or a public conveyance, by road), the said person shall have to generate the e-way bill (by furnishing information in part B on the common portal) [Rule 138(2)].

Where the e-way bill is not generated by the registered person and the goods are handed over to the transporter, for transportation of goods by road, the registered person shall furnish the information relating to the transporter in Part B on the common portal and the e-way bill shall be generated by the transporter on the said portal on the basis of the information furnished by the registered person in Part A [Rule 138(3)].

Where the goods are transported by railways or by air or vessel, the e-way bill shall be generated by the registered person, being the supplier or the recipient, who shall, either before or after the commencement of movement, furnish, information in part B [viz transport document number (Goods Receipt Number or Railway Receipt Number or Airway Bill Number or Bill of Lading Number)] on the common portal [Rule 138(2A)].

Other important points:

Where the goods are transported by railways: there is no requirement to carry e-way bill along with the goods, but railways has to carry invoice or delivery challan or bill of supply as the case may be along with goods. Further, e-way bill generated for the movement is required to be produced at the time of delivery of the goods. Railways shall not deliver goods unless the e-way bill required under rules is produced at the time of delivery [Proviso to rule 138(2A)].

The registered person or, the transporter may, at his option, generate and carry the e-way bill even if the value of the consignment is less than ` 50,000 [First proviso to rule 138(3)].

Where the movement is caused by an unregistered person either in his own conveyance or a hired one or through a transporter, he or the transporter may, at their option, generate the e-way bill [Second proviso to rule 138(3)]

Where the goods supplied by unregistered supplier to a recipient who is registered, the movement shall be said to be caused by such recipient if the recipient is known at the time of commencement of the movement of goods [Explanation 1 to rule 138(3)].

When is it not mandatory to furnish the details of conveyance in Part-B?

Explanation 2 to rule 138(3) stipulates that e-way bill is valid for movement of goods by road only when the information in Part-B is furnished. However, details of conveyance may not be furnished in Part-B of the e-way bill where the goods are transported for a distance of upto 50 km within the State/Union territory:

Documents to be carried by person in charge of conveyance

The person-in-charge of a conveyance shall carry –

√ the invoice or bill of supply or delivery challan, as the case may be; and

√ a copy of the e-way bill in physical form or the e-way bill number in electronic form or mapped to a Radio Frequency Identification Device used for identification (RFID) embedded on to the conveyance [except in case of movement of goods by rail or by air or vessel] in such manner as may be notified by the Commissioner [Rule 138A(1)].

However, in case of imported goods, the person-in-charge of a conveyance shall also carry a copy of the bill of entry filed by the importer of such goods and shall indicate date & no. of bill of entry in Part A of Form GST EWB 01.

E- Way Bill – When not required:

Certain categories of movements where E-waybill shall not be required to be generated and carried are as under:

1) 8 Notified goods in Annexure to Rule 138 including LPG, postal baggage, jewellery, currency, used personal and household effects, etc.

2) Where goods are transported in non-motorised conveyance

3) From Port/ Airport/ Air cargo complex/ Land customs station to ICD/Container Freight station (for clearance by Customs)

4) From ICD/container freight station to port/ airport/ air cargo complex/ and customs station under custom bond, or from one customs station or customs port to another customs station or customs port, or movement anywhere in India under customs supervision or under customs seal

5) Specific areas to be notified

6) Exempted goods other than de-oiled cake

7) Alcoholic liquor for human consumption, petroleum crude, high speed diesel, motor spirit, natural gas or aviation turbine fuel

8) Movement of goods from or to Nepal and Bhutan

9) Supply of goods falling under Schedule III

10) Intra-state movement of goods from Canteen Store Department (CSD) to unit run canteen and authorized customers, and from unit run canteen to authorized customers.

11) Intra-state movement of heavy water and nuclear fuels, as mentioned in Notification No. 26/2017 dated September 21, 2017 by the Department of Atomic Energy to the Nuclear Power Corporation of India Ltd

12) Movement of goods caused by defence formation under Ministry of defence as a consignor or consignee;

13) where the consignor of goods is the Central Government, Government of any State or a local authority for transport of goods by rail;

14) where empty cargo containers are being transported;

15) Movement of goods from place of business of consignor to weighbridge and vice-versa, where the distance is upto twenty kilometers, however goods in this case must be accompanied by a delivery challan.

Inspection and verification of Goods

After inspection of goods in transit, the proper officer shall prepare online, a summary report in Part A of Form EWB-03 within 24 hours of inspection and final report in Part B of Form EWB-03 within three days of such examination.

No further verification shall be done again in the state or union territory, where verification has been done during transit in the same state or union territory, except in case of specific information relating to evasion of tax is made available subsequently.

If Detention of vehicles for more than half an hour

Where a vehicle has been intercepted and detained for a period exceeding thirty minutes, the transporter may upload the said information in Form EWB-04 on the common portal.

Following are the enhancements in e-Way Bill System:

- Auto calculation of distance based on PIN Codes for generation of e-Way Bill.

- Knowing the distance between two PIN codes

- Blocking the generation of multiple e-Way Bills on one Invoice/Document.

- Extension of e-Way Bill in case the consignment is in Transit/Movement.

- Report on list of e-Way Bills about to expire.

Vehicle Number Verification:

E-Way Bill system is now integrated with Vaahan system of Transport Department. Vehicle (RC) number entered in e-waybill will be verified with Vaahan data for its existence/correctness. If the vehicle number does not exist, then system will alert the user to check and correct, if required. If the vehicle (RC) number is correct as per the tax payer, then he can continue with generation of E-Way Bill. However, he needs to get the vehicle number updated in the vaahan database so that in future E-Way Bill generation will not be affected.

THANKING YOU

Author Bio