Understanding the complexities of blocked Input Tax Credit (ITC) in real estate construction. Explore implications for businesses dealing with raw materials in real estate projects. Stay informed on GST regulations and ITC eligibility.

In the realm of real estate construction, the utilization of Input Tax Credit (ITC) is a critical aspect that can significantly impact businesses. This article delves into the complexities surrounding blocked credits for a real estate and infrastructure company.

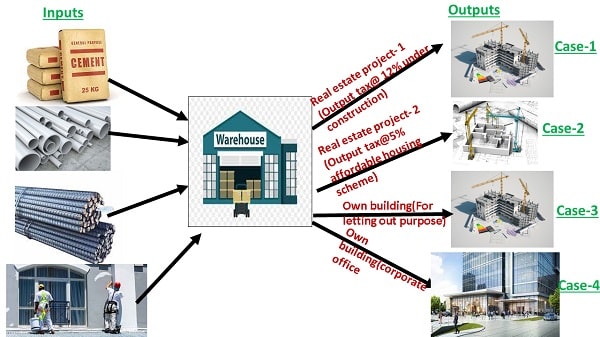

1. Real estate Company (RE Ltd) is into the construction of real estate projects across the country, it purchases various raw materials like cement, TMT rods, Bricks, Tiles, Marble, Granite etc.

2. Summary

3. Following are the movements happened in the warehouse register from warehouse to the projects.

| Case | Movement type | Description | ITC |

|---|---|---|---|

| 1 | 101 | Consumption made for real-estate project 1 | Can be availed (Output tax @ 12%/18%) |

| 2 | 102 | Consumption made for real-estate project 2 | Cannot be availed (Output tax @ 5%/1%) |

| 3 | 103 | Consumption made for Own Building (For renting out) | Can be availed as per HC judgement |

| 4 | 104 | Consumption for Own building (for corporate office) | Cannot be availed (as per 17(5) on own account) |

4. Inputs consumed in the construction business would not be eligible for availing ITC as per the definition of ITC u/s 17(5) except in case of further supply or furtherance of business

The relevant provision of Section 17(5) of CGST Act, 2017 is reproduced below: – Notwithstanding anything contained in sub-section (1) of section 16 and sub-section (1) of section 18, input tax credit shall not be available in respect of the following, namely: –

(a) motor vehicles . . .

(b) – – –

(c) – – – –

(d) goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

Explanation: For the purposes of clauses (c) and (d), the expression “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property.

As per the Section 17 (5) of CGST Act mentioned above, the Input tax credit shall not be available on the goods and services, or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

The definition of immovable property is not provided under GST Act. According to section 3(26) of the General Clauses Act, 1882, “Immovable property shall include land, benefits to arise out of land and things attached to the earth, or permanently fastened to anything attached to the earth”. According to section 3 of the Transfer of Property Act, 1882, Immovable property means “Immovable property does not include standing timber, growing crops or grass”.

5. In the instance, the RE ltd is consuming the raw material in totality in a bulk and storing in a Godown/Warehouse and later its movement from Godown/warehouse involves consuming for construction of real estate projects and few of which are consumed for construction of its own Building (corporate office).

Consumption done exclusively for each project need to be identified and that would be the big task and the same can be identified by tracking the Consumption of raw-material for respective project using filters for the movement type- say, 103, we get consumption made for own building.

Applicability of GST on providing Works contract and sub-contract: Works contract is a composite supply as it is a construction where goods as well as services are given. For the purpose of levying GST, principal supply is considered to be supply of service. Construction service is just a part of works contract. Therefore, construction of a residential unit in various housing projects and other than housing projects shall be taxed at 12%. When any contract is further sub-contracted then the GST shall also be levied at 12%.

Applicability of GST on sale of Flats/ Properties: GST is not leviable on sale to ready-made homes. On completion of its construction and after receiving the occupancy certificate, a property is categorized as to ready-made homes. Such kind of property does not come under the purview of GST. GST would be applicable only of the sale of under-construction properties that have yet to receive the occupancy certificate. When an arrangement is made with the builder for construction of Floors/Flats, (other than approved housing projects) and where the some of the floors/flats are given to the builder as consideration for the construction then GST shall not be applicable on undivided share of land, but GST shall be taxable at the rate of 18% on the transfer of the floors/flats by the builder to the landowner.

Applicability of GST on earning Rental Income: No GST is levied on rental income as long as residential property is rented out. However, 18% GST is applicable if such property is on rent for business purposes or rent amount per year exceeds the registration limit. 18% GST is applicable on renting commercial properties.

Non-Applicability of GST on Sale of Land: As per Schedule III of the CGST Act sale of land shall be treated neither as a supply of goods nor a supply of services. Since, sale of land is not a supply under GST and hence falls outside its purview. GST on sale of Plot No GST will be levied on sale of Plot. However, a plot with any kind of construction on it will attract GST.

6. Case-1 as per general interpretation of the provision ITC can be availed

Case -2 is such a project where RE ltd collects GST @ 5%/1% without ITC from its prospective customers and therefore ITC with respect to real estate project – 2 would also be not eligible and all the purchases made for the consumption for Project-2 would be blocked and such purchases would be identified by the same exercise as that of Own building.

Case-3 It was held by Orrisa High Court in case of Safari Retreats (P.) Ltd. vs Chief Commissioner of Central Goods & Service Tax [W.P. (C) NO. 20463 OF 2018] [(2019) 105 taxmann.com 324 (Orissa)] Where petitioner had not sold shops in mall but had let out same, petitioner was not liable to pay huge amount of GST on rent received and was entitled to utilize input credit tax charged on purchases made in construction. Safari Retreats Pvt. Ltd. (“Safari Retreat”) was in the business of constructing shopping malls and then letting out different units in the constructed mall on rent or under a lease to other businesses.

Condition in Section 17(5) (d) of both the aforesaid Act which reads as when such goods or services or both are used in the course or furtherance of business’ this condition is applicable only when the immovable property is constructed ‘on his own account’ as appearing in those sections, which means that the taxable person on whose account the said immovable property is constructed.

The said condition cannot be applied to any other cases far less when the construction of the immovable property is intended for letting out.

Therefore, ITC can be availed in case-3

Case-4: Section 17 sub-section (5) Clause (d) restricts input tax credit of goods and services used by a person for construction of an immovable property (except plant and machinery) on his own account.

ON HIS OWN ACCOUNT: The phrase “On his own account” has not been defined anywhere. The GST Laws whether CGST or SGST or IGST nowhere defines the said phrase. Therefore, general meaning of the expression should be derived. The plain and simple meaning of the said term according to my limited understanding should be “for his own purposes”.

This phrase was tested at the Authority for Advance Ruling – Andhra Pradesh (AAR-AP) in case of M/s Karthikeya Projects [AAR No. 09/AP/GST/2021] [2021-VIL-333-AAR]

All these consumptions used for construction of its own building would not be qualified for availing ITC as per section 17(5) and accordingly the purchases of these raw-material which are consumed and used for Own building would be not eligible for claiming ITC even if the registered person is into the business of construction and real estate, which is why RE ltd need to reverse the ITC to the extent of such raw material if it has availed earlier.