In the dynamic landscape of corporate governance in India, managerial personnel (MPs) hold a pivotal role in shaping the direction of companies. The Companies Act, 2013, meticulously outlines the statutory obligations and regulations concerning the appointment and remuneration of these crucial individuals. Understanding the nuances of these legal provisions is essential for both corporate professionals and organizations to ensure compliance and foster transparent corporate practices.

In this comprehensive guide, we embark on an in-depth exploration of 45 frequently asked questions (FAQs) that shed light on the intricacies of statutory obligations for managerial personnel in India. From the appointment of MPs under Section 196 to the computation of managerial remuneration in accordance with Section 198 and Schedule V of the Companies Act, 2013, we leave no stone unturned in providing clarity on this vital subject.

Whether you are a seasoned corporate professional seeking to navigate the complexities of managerial appointments and remuneration or an organization aiming to ensure strict adherence to the legal framework, this article is your go-to resource. Join us on this journey as we dissect the key aspects, provide insightful analysis, and offer conclusive takeaways to empower you with the knowledge needed to navigate the realm of statutory obligations for managerial personnel in India.

Page Contents

- (A) Statutory Obligations for appointment of MPs in India (Section 196) Companies Act, 2013.

- (B) Managerial Remuneration for MPs in India (Section 197) CA, 2013

- 6. Applicability for Remuneration to MPs

- 7. Non Applicability for Remuneration to MPs

- 8. Permitted Automatic Route for remuneration to MPs

- 9. Required Shareholder’s Approval for remuneration to MPs

- 10. Required Shareholder’s Approval + approval (both) for remuneration

- 11. Not permitted for Remuneration beside adequate profits

- 12. Not permitted for stock options to Independent Directors (IDs)

- 13. Required for MPs to refund against extra paid remuneration by co.

- 14. Permitted for meeting fee to IDs over and above 11% or 5% or 3% or 1%

- 15. Permitted for professional fee for professional services to company

- 16. Permitted for meeting fee to IDs within prescribed limit

- 17. Permitted for monthly payment for managerial remuneration to MPs

- 18. Permitted for meeting fees + expenses reimbursement + commission

- 19. Required for disclosure in BoD’s report for remuneration to MPs

- 20. Permitted for insurance premium for indemnifying MP’s liability

- 21. Not Permitted for insurance premium for indemnifying MP’s liability

- 22. Permitted for remuneration + commission (both) from holding company

- 23. Liability for fine against specified contraventions made under section 197

- (C) Computation for Managerial Remuneration for MPs in India (Sec 198) CA, 13

- (D) Appointment + Managerial Remuneration for MPs in India (Schedule V) CA, 2013

- 26. Appointment for MPs (Part-I of Schedule-V)

- 27. Remuneration for MPs (section-I of Part-II of Schedule-V)

- 28. Remuneration for MPs (section II of Part II, of Schedule V)

- 30. Remuneration for non-professional MPs (Sec.-III of Part-II of Sch.-V)

- 31. Permitted for excess remuneration (Sec.-III of Part-II of Schedule-V)

- 32. Perquisites for MPs (Section-IV of Part-II of Sch.-V)

- 33. Not Perquisites for resident of India (Sec-IV of Part-II of Sch.-V)

- 34. Not Perquisites for non-resident of India (Sec-IV of Part-II of Sch.-V)

- 35. Meaning for effective capital of company (Section-IV of Part-II of Sch.-V)

- 36. Meaning for not effective capital of company (Sec.-IV of Part-II of Sch.-V)

- 37. Meaning for family of MPs (Sec.-IV of Part-II of Sch.-V)

- 38. Meaning for nomination & remuneration committee (Sec.-IV of Part-II of Sch.-V)

- 39. Meaning for negative effective capital + Remuneration (Sec.-IV of Part-II of Sch.-V)

- 40. Permitted for remunerations from 2 companies (Sec.-V of Part-II of Sch.-V)

- 41. Role for auditor or CS in service or CS in whole time practice (Part-III of Sch.-V)

- 42. Govt’s powers for exemption to class(s) of company (Part-IV of Sch.-V)

- (E) Conclusion on Appointment + Remuneration for MPs (Sec. 196 to 198 + Sch. V)

- (F) Provisions for appointment + remuneration (section 196 to 198 + schedule V)

(A) Statutory Obligations for appointment of MPs in India (Section 196) Companies Act, 2013.

1. Introduction for MPs (Section 196)

(i) MP’s be appointed referred under section 196 of Companies Act (CA), 2013 + also MP’s definition referred under section 2(53) + 2(54) (both).

(ii) MPs to include certain persons like:

(a) Managing Director (MD)

(b) Whole-time Director (WTD)

(c) Manager (1 only)

- MD + WTD + Manager (all) commonly known MPs

(iii) Managerial remuneration + Managerial remuneration’s computations referred under section 197 + 198 of CA, 2013 respectively + Article of Association (AoA) (all).

(iv) (a) MP’s appointment referred under section 196 of CA, 2013

+ (plus)

(b) Also applicable for Private Limited Companies (Private Companies) + Public Limited Companies (Public Companies) (both)

(v) Managerial remuneration referred under section 197 + 198 + Part II schedule V of CA, 2013 (all 3) not applicable for private companies.

(vi) Managerial remuneration referred under section 197 + 198 + Part I + Part II schedule V of CA, 2013 (all 4) applicable for public companies (only).

2. Appointment for MPs (Section 196)

(i) Companies not permitted for appointment of MPs

(a) 100% companies not permitted to appoint 1 MD + also 1 Manager

= 2 at same time therefore permitted to appoint either 1 MD or 1 Manager (any) = 1 at same time.

+ (plus)

(b) Also 100% companies not permitted to appoint or re-appoint MPs exceeding for 5 year at 1 time therefore re-appointment be required for renewal for 5 year at 1 time but permitted to appoint in multiple of 5 years say may be appointed + re-appointed (both) maximum for 9 time like for 45 (5 @ 9 = 45) year.

+ (plus)

(c) Also 100% companies not permitted to appoint MPs below age 21 year + also exceeding age 70 year (both)

+ (plus)

(d) Also 100% companies not permitted to appoint MPs those still un-discharged insolvent or already adjudged insolvent (any).

+ (plus)

(e) Also 100% companies not permitted to appoint MPs those suspended payments to creditors or made composition with creditors (any).

+ (plus)

(f) Also 100% companies not permitted to appoint MPs those convicted by court for offence + also sentenced for imprisonment even for 1 hour (both together).

(ii) Companies permitted for appointment for MPs

(a) 100% Companies permitted to appoint 1 MP beside age exceeding 70 year through passing Special Resolution (SR) in Annual General Meeting (AGM) or Extraordinary General Meeting (EGM) + also to justify for appointment.

+ (plus)

(b) Also 100% companies permitted to appoint MPs after satisfying provisions referred under section 197 or schedule V (any) CA, 2013.

+ (plus)

(c) 100% companies permitted to appoint 1 MP with terms + conditions specified for appointment + remuneration + be approved by Board of Directors (BoDs) + also be seconded by AGM or EGM through passing Ordinary Resolution (OR) (all together).

+ (plus)

(d) Also 100% companies permitted to appoint 1 MP after approval from Central Govt. (govt.) when terms + conditions referred under section 197 or schedule V (any) CA, 2013 not matching with each other.

+ (plus)

(e) Also 100% companies permitted to appoint 1 MP after filling form MR-1 with ROC in 60 day from date of appointment.

+ (plus)

(f) Also 100% companies permitted to appoint 1 MP + also permitted to regularize 100% actions exercised by MPs till date of AGM or EGM when appointment of MPs not approved in AGM or EGM

3. Meaning for Manager (Section 2(53))

(i) Meaning to include when individual managing 100% or almost 100% (substantially) affairs of company.

+ (plus)

(ii) Also manager managing under superintendence’s + controls + directions (all) from company’s BoDs.

+ (plus)

(iii) Also include director or other person who occupying position equivalent to manager with or without formal contract (any) for services.

4. Meaning for Managing Director (MD) (Section 2(54))

(i) Meaning to include when director employed under articles of company or agreement with company or passed OR in AGM or EGM or through BoDs (any) which entrusted with substantial powers for management of affairs of company.

+ (plus)

(ii) Also to include director who occupying position of MD through other name.

5. Meaning for Whole Time Director (WTD) (Section 2(94))

- Meaning to include director who is in whole time employment for company therefore part time director not treated WTD.

(B) Managerial Remuneration for MPs in India (Section 197) CA, 2013

6. Applicability for Remuneration to MPs

(i) Introduction on Remuneration for MPs

Remuneration for MPs by corporate in India defined under section 197 + also word Managerial remuneration defined under section 2(78) of CA, 2013 (both).

(ii) Applicability for Remuneration for MPs:

(a) For Public Companies

(b) For Private Companies

But

Be subsidiaries of Public Companies

7. Non Applicability for Remuneration to MPs

- Remuneration for MPs not applicable on Private Companies (only).

8. Permitted Automatic Route for remuneration to MPs

- Automatic route for managerial remunerations permitted when adequate profits existed + also managerial remunerations not exceeding specified limits like 11% or 5% or 3% or 1% (any) Adjusted Net Profits (ANP) companies

+ (plus)

(i) Shareholders’ approval required through passing OR in AGM or EGM beside remuneration already permitted under automatic route referred under section 197 of CA, 2013 for adequate profits.

+ (plus)

(ii) Shareholders’ approval required through passing OR in AGM or EGM when managerial remuneration not exceeding 100% referred under part II of schedule V of CA, 2013 for losses or inadequate profits.

+ (plus)

(iii) Also shareholders’ approval required through passing SR in AGM or EGM when managerial remuneration not exceeding 200% referred under part II of schedule V of CA, 2013 for losses or inadequate profits.

- Shareholders’ approval + govt.’s approval (both) required for managerial remuneration to MPs when managerial remuneration exceeding limits referred under section 197 like 11% or 5% or 3% or 1% (any) beside adequate profits existed + also permitted under schedule V of CA, 2013 (all)

11. Not permitted for Remuneration beside adequate profits

(i) 100% companies not permitted to pay managerial remuneration to MPs exceeding 11% of ANP computed under section 198 of CA, 2013 without approval from govt.

+ (plus)

(ii) Also 100% companies not permitted to pay managerial remuneration to 1 MP exceeding 5% + also to 2 MPs or more than 2 MPs exceeding 10% of ANP computed under section 198 of CA, 2013

+ (plus)

(iii) Also 100% companies not permitted to pay managerial remuneration to non MPs (Independent Directors) exceeding 1% of ANP computed under section 198 of CA, 2013.

+ (plus)

(iv) Also 100% companies not permitted to pay managerial remuneration to non MPs (Independent Directors) exceeding 3% of ANP computed under section 198 of CA, 2013 beside more than 3 non MPs existed (@ 1% per non MPs).

+ (plus)

(v) Also 100% companies not permitted to pay managerial remuneration to MPs exceeding limits referred under schedule V of CA, 2013 when companies having no profits or inadequate profits (any)

12. Not permitted for stock options to Independent Directors (IDs)

- 100% companies not permitted to give stock options to IDs beside permitted to give stock options to non IDs (MPs).

13. Required for MPs to refund against extra paid remuneration by co.

- 100% companies not permitted to waive recovery for refund from extra paid managerial remuneration referred under section 197(9) of CA, 2013 without approval from govt.

14. Permitted for meeting fee to IDs over and above 11% or 5% or 3% or 1%

- 100% companies permitted to pay meeting fee to IDs for attending meetings for BoDs + also for meetings for management committee(s) over and above limit like 11% or 5% or 3% or 1% (any) therefore permitted to pay meeting fee excluding abovementioned limit.

15. Permitted for professional fee for professional services to company

- 100% companies permitted to pay managerial remuneration to professional for providing professional services when nomination and remuneration committee or BoDs (any) approved requisites professional qualifications of directors without application of limits like 11% or 5% or 3% or 1% (any).

16. Permitted for meeting fee to IDs within prescribed limit

- 100% companies permitted to pay fee for attending meetings of BoDs + management committees not exceeding amount prescribed for class of companies (both).

17. Permitted for monthly payment for managerial remuneration to MPs

- 100% companies permitted to pay managerial remuneration on monthly on specified % (percentage) of ANP being partly on monthly + also partly on percentage basis.

18. Permitted for meeting fees + expenses reimbursement + commission

(i) 100% companies permitted to pay meeting fee for attending meetings of BoDs + also meeting of management committees on different matters (both) to IDs.

+ (plus)

(ii) Also permitted to pay for reimbursement of expenses to attend meetings of BoDs + also meetings of management committees constituted on different matters (both) to IDs.

+ (plus)

(iii) Also permitted to pay commission not exceeding 1% or 3% of ANP (as case may be) to IDs after passing OR in AGM or EGM.

19. Required for disclosure in BoD’s report for remuneration to MPs

- 100% companies required to disclose payments for managerial remuneration to MPs in BoD’s report + ratios for remuneration to MPs + also other prescribed details (all).

- 100% companies not permitted to treat managerial remuneration for insurance premium paid on behalf of MPs for indemnifying against liability for negligence or default or misfeasance or breach of duty or breach of trust (any) for purpose + also welfare of companies (both).

- 100% companies not permitted to treat managerial remuneration for insurance premium paid on behalf of MPs for indemnifying against liability for negligence or default or misfeasance or breach of duty or breach of trust (any) for purpose + welfare of companies (both) when proved that MP was guilty.

22. Permitted for remuneration + commission (both) from holding company

- MPs permitted to receive remuneration + commission (both) from holding company or subsidiary companies after disclosing in BoDs report.

23. Liability for fine against specified contraventions made under section 197

- Responsible MPs required to pay minimum fine INR 1 lac

Or

Required to pay maximum fine INR 5 lac for each contravention referred under section 197 of CA, 2013.

(C) Computation for Managerial Remuneration for MPs in India (Sec 198) CA, 13

24. Computation for remuneration to MPs

(i) Computation for eligible CSR’s or managerial remuneration amount (any) treated important for corporate.

(ii) Computation for managerial remuneration of ANP (sec 198)

- Section 198 of CA, 2013 guiding for computing ANP through adding 2 items and subtracting 20 items from net profits computed under schedule III of CA , 2013 like on March 31st, 2023.

(iii) Companies required to compute ANP taking help from CA or CS or ICWA or other professional to decide eligible amount for CSR or managerial remuneration (any).

25. Computation for Adjusted Net Profits (ANPs) for Remuneration to MPs

- Net profits computed under schedule III of CA, 2013 on March 31st 2023.

+ (plus)

(i) 100% amounts received for bounties + subsidies from govt. + also public authority (all) constituted or authorized on behalf of govt.

(ii) 100% amounts received for profits on sale of fixed assets over and above Written Down Value (WDV)

(-) minus

(iii) 100% amounts received for premium on shares or debentures issued or sold by company

(iv) 100% amounts received for profits on forfeiture of shares by company

(v) 100% amounts claimed for losses of capital in nature + also losses on sale of undertaking (both) by company.

+ (plus)

(vi) 100% amounts paid for expenses on business’s purpose

(vii) 100% amounts paid for director’s remuneration to MPs

(viii) 100% amounts paid for bonus + commission (both) to employees

(ix) 100% amounts paid for tax notified by govt.

(x) 100% amounts paid for tax imposed on business profits

(xi) 100% amounts paid for interest on debentures

(xii) 100% amounts paid for interest on secured loans

(xiii) 100% amounts paid for interest on unsecured loans + advances (both)

(xiv) 100% amounts paid for expenses on repairs

(xv) 100% amounts paid for contributions referred under section 181 of CA, 2013

(xvi) 100% amounts allowed for depreciation referred under section 123 of CA, 2013

(xvii) 100% amounts paid for excess of expenditures over incomes

(xviii) 100% amounts paid for compensation + damages (both) for legal liability

(xix) 100% amounts paid for insurance premium

(xx) 100% amounts allowed for debts considered bad + also written off or adjusted

(D) Appointment + Managerial Remuneration for MPs in India (Schedule V) CA, 2013

26. Appointment for MPs (Part-I of Schedule-V)

(i) Appointment for MPs permitted without approval from govt. after satisfying certain terms + conditions (both) when MPs not sentenced to imprisonment for even 1 hour or imposed fine exceeding 1 thousand (any) for conviction of offence referred under followings 19 Acts like:

(a) Fugitive Economic Offenders (FEO) Act, 2018

(b) Goods and Services Tax (GST) Act, 2017

(c) Insolvency and Bankruptcy Code (IBC), 2016

(d) Companies Act (CA) 2013 + 1956 (both)

(e) Prevention of Money-Laundering Act (PMLA), 2002

(f) Competition Act, 2002

(g) Foreign Exchange Management Act (FEMA) Act 1999

(h) Securities and Exchange Board of India (SEBI) Act, 1992

(i) Sick Industrial Companies (Special Provisions) Act, 1985

(j) Customs Act, 1962

(k) Income-tax Act, 1961

(l) Wealth-tax Act, 1957

(m) Securities Contracts (Regulation) Act, 1956

(n) Essential Commodities Act, 1955

(o) Prevention of Food Adulteration Act, 1954

(p) Industries (Development and Regulation) Act, 1951

(q) Central Excise Act, 1944

(r) Foreign Trade (Development and Regulation) Act, 1922

(s) Indian Stamp Act, 1899

(ii) Appointment for MPs permitted without approval from govt. when not detained even for 1 day under Conservation of Foreign Exchange and Prevention of Smuggling Activities Act, 1974.

- Govt.’s approval not needed for 2nd (subsequent) appointment when MP’s original appointment made with govt.’s approval.

- Govt.’s approval needed for 2nd appointment for MPs beside original appointment made with govt.’s approval when MPs convicted or detained after 1st appointment.

(iii) (a) Govt.’s approval not required when MPs completed 21 year or not completed 70 year of age (any).

+ (plus)

(b) Also govt.’s approval not required when MP’s age completed 70 year

But

Company passed SR in AGM or EGM.

(iv) Govt. approval not required when MPs appointed + also drawing remuneration from 1 or more than 1 companies where remuneration not exceeding limit provided in Part II (section V) of schedule V of CA, 2013

(v) Govt. approval not required when MPs is non-resident + certain terms + also conditions (all) satisfied for treating him resident of India like:

(a) When MPs staying in India for minimum 12 month in immediate preceding year from date of appointment

+ (plus)

(b) Also MPs staying with VISA for taking employment or carrying on business or vocation (any) in India.

- Above condition not applicable for companies those conducting business in Special Economic Zones (SEZ) notified by deptt. of commerce govt. of India.

- Non resident permitted to enter in India after obtaining proper employment VISA from Indian embassy which located outside India.

27. Remuneration for MPs (section-I of Part-II of Schedule-V)

♦ Remuneration for MPs when adequate profits existed ♦

- 100% companies permitted under Automatic Route for remunerations to MPs when adequate profits existed like 11% or 5% or 3% or 1% (any) prescribed under section 197 of CA, 2013

28. Remuneration for MPs (section II of Part II, of Schedule V)

♦ Remuneration for MPs when adequate profits not existed ♦

- 100% companies permitted to pay managerial remuneration to MPs within following limits:

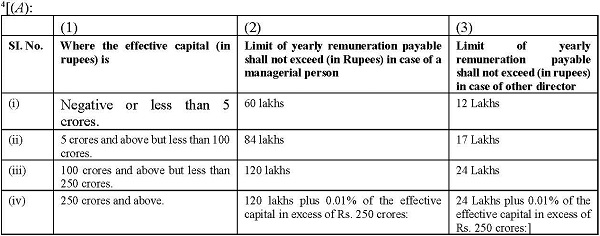

| SI. No | Amount of effective capital | Maximum Remuneration to MPs | Maximum Remuneration to Non MPs |

| (a) | When losses or profits not exceeding 5 crore | 60 lac | 12 lac |

| (b) | When profits not exceeding 100 crore | 84 lac | 17 lac |

| (c) | When profits not exceeding 250 crore | 120 lac | 24 lac |

| (d) | When profits exceeding 250 crore | 120 lac + 0.01% of effective capital when profits exceeding 250 crore | 24 lac + 0.01% of effective capital when profits exceeding 250 crore |

- 100% companies permitted to pay managerial remuneration not exceeding 200% over and above abovementioned limits after passing SR in AGM or EGM (any)

- 100% companies permitted to pay managerial remuneration on proportionate basis when MPs appointed for less than 12 month.

29. Remuneration for professional MPs (section II of Part II, of Schedule-V)

(i) Remuneration for professional MPs not having interest in capital of company

(a) 100% companies permitted to pay remuneration to MPs employed in professional capacity + also not having any interest in capital of company or holding company or subsidiary companies directly or indirectly or through other statutory structures (any)

+ (plus)

(b) Also MPs employed in professional capacity + not having direct or indirect interest or related to directors or promoters or holding company or subsidiary companies any time during last 2 year before or after appointment’s date + possesses minimum graduate level qualification + having expertise + also specialized knowledge in field of company’s operations (all).

(ii) Meaning of MPs employed in professional capacity + not having interest in capital

(a) When MPs owned paid up share capital not exceeding 5% under scheme formulated for allotment of shares to MPs like Employees Stock Option Plan (ESOP) + qualification shares (both) treated not having interest in capital of company

+ (Plus)

(b) When companies approved payment for remuneration through passing resolution by BoDs or by nomination and remuneration committee + also formation of nomination and remuneration committee which referred under section 178 (1) of CA, 2013

(c) (ca) When companies not committed default in payment for dues to banks or financial institution or Non Convertible Debenture (NCD) holder or other secured creditors (any)

+ (plus)

(cb) Also companies required to obtain No Objection Certificate (NOC) from lenders before passing OR in AGM or EGM when companies defaulted in payment for lender’s dues.

(ii) 100% companies required to pass OR or SR (as case may be) for payment of remuneration in AGM or EGM for period not exceeding 3 year.

30. Remuneration for non-professional MPs (Sec.-III of Part-II of Sch.-V)

(i) 100% companies permitted to pay managerial remuneration to MPs beside not having profits or inadequate profits + also in excess of limits which prescribed under section I or II of part II of schedule V of CA, 2013 but after satisfying certain terms + conditions (all) like:

(a) When Indian companies or foreign companies passed SR in AGM or EGM (any)

+ (plus)

(b) Also 100% companies permitted to treat remuneration paid within permissible limit which referred under section 197 of CA, 2013

31. Permitted for excess remuneration (Sec.-III of Part-II of Schedule-V)

(i) For 100% newly companies incorporated + also excess managerial remuneration permitted up to 7 year from date of incorporations

(ii) For 100% sick companies + also schemes of revival or rehabilitation ordered by Board for Industrial and Financial Reconstruction (BIFR) up to 5 year from date of sanction of scheme.

(iii) When resolution plan approved by National Company Law Tribunal (NCLT) under Insolvency and Bankruptcy Code (IBC) 2016 (31 of 2016) up to 5 year from date of resolution plan approved.

(iv) When managerial remuneration fixed by BIFR or NCLT (as case may be)

(v) Certain additional conditions to be satisfied like :

(a) Statutory auditor(s) or employee Company Secretary (CS) or CS engaged in Whole-Time Practice (WTP) (any) required to issue certificate that 100% secured creditors + terms lenders already confirmed in writing that they have no objection for appointment of MPs + quantum of remuneration + also above certificate (all) to be submitted with return which prescribed under section 196(4).

+ (plus)

(b) Also to certify in certificate that 100% payments already settled on time to 100% creditors + depositors + also certificate (all) to be submitted with return which prescribed under section 196 (4).

32. Perquisites for MPs (Section-IV of Part-II of Sch.-V)

- Certain perquisites treated managerial remuneration to MPs like:

(i) Value for rent-free accommodation provided to MPs by employer.

(ii) Value for concession rent provided to MPs by employer.

(iii) Value for benefits + amenities (both) provided to MPs at free of cost or at concessional rate (any) + also they have substantial interest in company except certain exceptions.

(iv) Actual amount paid by employer for MP’s obligations.

(v) Actual amount paid for assurance on life + also paid for contracts of annuities (both) by employer.

(vi) Value for sweat equity shares allotted or transferred (any) by present employer + also by former employer (both).

(vii) Actual amount paid for contribution to approve superannuation fund by employer up to INR 1 lac applicable from year ending on March 31, 2010.

(viii) Value for other fringe benefits + amenities (both) may be prescribed in future under CA, 2013

(ix) Actual amount paid for insurance + pension + annuity + gratuity for self + spouse + also children (all) by employer.

33. Not Perquisites for resident of India (Sec-IV of Part-II of Sch.-V)

- Certain perquisites not treated managerial remuneration given to resident MPs:

(ii) Amount paid by employer for contribution to Provident Fund (PF) or superann-uation fund or annuity fund (any) may be singly or jointly with other employees

(ii) (a) Amount paid by employer for gratuity for maximum 15 day’s salary (per year) for completed years of service

+ (plus)

(b) Also 26 day in month be accepted instead 30 day

(iii) Amount paid by employer for leave encashment at end of contracted term for employment.

- Abovementioned perquisites under para (i) to (iii) (all) not taxable under Income Tax Act (ITA), 1961

34. Not Perquisites for non-resident of India (Sec-IV of Part-II of Sch.-V)

- Certain perquisites not treated managerial remuneration given to non-resident MPs:

(i) (a) Amount paid by employer for Children’s Education Allowance (CEA) up to INR 12000 per month per child or actual expenses whichever lower when children staying outside India (not in India)

+ (plus)

(b) Also CEA not permitted for more than 2 child.

(ii) (a) Paid for return holiday passage be up to 1 time in 1 year in economic class

Or

(b) Paid for return holiday be up to 1 time in 2 year in 1st class when children staying outside India (not in India).

(iii) Amount paid by employer for Leave travel concession (LTC) for self + also family under rules specified by company when leave be spent in home country located outside India (not in India).

35. Meaning for effective capital of company (Section-IV of Part-II of Sch.-V)

(i) Meaning for effective capital

(a) Aggregate total for paid-up share capital

But

(b) Not included certain items like share application money or advances for shares (if any).

+ (plus)

(b) Aggregate total for share premium account reserves and surplus

But

Not included revaluation reserves or long-term loans or deposits (any) payable after 1 year.

But

Included borrowed capital loans + overdrafts + interest due on loans + bank guarantees + etc. (all)

(c) Other short-term arrangements

– (Minus)

Aggregate total for investments

But

Not included investments made by investment companies those have principal business for acquisition of shares + stocks + debentures + other securities (all).

– (Minus)

Accumulated losses – preliminary expenses not written off .

36. Meaning for not effective capital of company (Sec.-IV of Part-II of Sch.-V)

(i) Effective capital to be computed on date of incorporation for MP’s appointment in year of incorporation for new company.

+ (plus)

(ii) Effective capital to be computed on last date of financial year preceding to financial year in which MP’s appointment made.

37. Meaning for family of MPs (Sec.-IV of Part-II of Sch.-V)

- To include spouse + depended children + also depended parents (all).

38. Meaning for nomination & remuneration committee (Sec.-IV of Part-II of Sch.-V)

- Nomination and remuneration committee permitted to approve managerial remuneration which referred under section II + III of part-II of schedule-V of CA, 2013 with certain criteria’s like:

(i) Nomination and remuneration committee required to take financial position of company + also certain factors like:

(a) Industry’s Trend

(b) Appointee MP’s qualification

(c) Appointee MP’s Experience

(d) Appointee MP’s performance

(e) Appointee MP’s past remuneration

(f) Appointee MP’s etc.

(ii) Nomination and remuneration committee required to maintain balance between interest of company and shareholders (both) with object for determining MPs remuneration’s package.

39. Meaning for negative effective capital + Remuneration (Sec.-IV of Part-II of Sch.-V)

(i) Meaning for negative effective capital

- To include negative effective capital when net capital is lower than zero

(ii) Meaning for managerial remuneration

- To include managerial remuneration which defined under section 2(78) of CA, 2013 + also reimbursement made for direct taxes to MPs (both)

40. Permitted for remunerations from 2 companies (Sec.-V of Part-II of Sch.-V)

(i) MPs permitted to receive managerial remuneration from 2 companies

But

(ii) Aggregate remuneration from 2 companies not to exceed maximum limit permitted for any 1 company out of 2 companies (whichever higher).

41. Role for auditor or CS in service or CS in whole time practice (Part-III of Sch.-V)

(i) 100% companies required to pass OR or SR (as case may be) in AGM or EGM for appointment + remuneration which specified under Part-I + Part-II (all) Schedule-V of CA, 2013

+ (plus)

(ii) (a) Also statutory auditor(s) or CS in service of company or CS engaged in Whole Time Practice (WTP) (any) required to issue certificate that 100% compliances already completed by company which specified under Part-I + Part-II (both) of Schedule-V of CA, 2013

+ (plus)

(b) Also required to submit abovementioned certificate with return to be filed with ROC which referred under section 196(4) of CA, 2013

42. Govt’s powers for exemption to class(s) of company (Part-IV of Sch.-V)

- Govt. permitted to notify for exemption to class(s) of company from any requirement which specified under Part-I to Part-IV of Schedule V of CA, 2013

(E) Conclusion on Appointment + Remuneration for MPs (Sec. 196 to 198 + Sch. V)

43. Conclusion on appointment for MPs (Section 196 of CA, 2013)

(i) Appointment of MPs permitted by passing resolution in BoD’s meeting or in nomination and remuneration committee’s meeting whichever applicable

+ (plus)

(ii) Also by passing OR in AGM or EGM for MP’s appointment.

+ (plus)

(iii) Also to obtain approval from Govt. for MP’s appointment when already not permitted which referred under section 196 to 198 + schedule V (both).

44. Conclusion on remuneration for MPs with adequate profits (Sec. 197)

(i) MP’s remuneration permitted under automatic route when adequate profits existed by passing resolution in BoD’s meeting or nomination and remuneration committee’s meeting whichever applicable

+ (plus)

(ii) Also by passing OR in AGM or EGM for MP’s appointment.

+ (plus)

(iii) Also to obtain approval from Govt. for MP’s remuneration when exceeding monetary limits which prescribed under section 197 of CA, 2013 like 11% or 5% or 3% or 1% (any).

45. Conclusion on remuneration for MPs with inadequate profits (Sch. V)

(i) MP’s remuneration permitted beside profits not existed or inadequate profits existed (any) by passing resolution in BoD’s meeting or nomination and remuneration committee’s meeting whichever applicable

+ (plus)

(ii) (a) Also by passing OR in AGM or EGM for remuneration when not exceeding 100% of monetary limits which prescribed under schedule V of CA, 2013

or

(b) By passing SR in AGM or EGM for remuneration when not exceeding 200% of monetary limits which prescribed under schedule V of CA, 2013

+ (plus)

(iii) Also to obtain approval from Govt. for remuneration when exceeding 200% of monetary limits which prescribed under schedule V of CA, 2013.

(F) Provisions for appointment + remuneration (section 196 to 198 + schedule V)

-

Provisions for appointment + remuneration (Sec. 196 to 198 of Chapter XIII)

CHAPTER XIII

APPOINTMENT AND REMUNERATION OF MANAGERIAL PERSONNEL

196. Appointment of managing director, whole-time director or manager. (1) No company shall appoint or employ at the same time a managing director and a manager.

(2) No company shall appoint or re-appoint any person as its managing director, whole-time director or manager for a term exceeding five years at a time:

Provided that no re-appointment shall be made earlier than one year before the expiry of his term.

(3) No company shall appoint or continue the employment of any person as managing director, whole-time director or manager who

(a) is below the age of twenty-one years or has attained the age of seventy years:

Provided that appointment of a person who has attained the age of seventy years may be made by passing a special resolution in which case the explanatory statement annexed to the notice for such motion shall indicate the justification for appointing such person;

(b) is an undischarged insolvent or has at any time been adjudged as an insolvent;

(c) has at any time suspended payment to his creditors or makes, or has at any time made, a composition with them; or

(d) has at any time been convicted by a court of an offence and sentenced for a period of more than six months.

(4) Subject to the provisions of section 197 and Schedule V, a managing director, whole-time director or manager shall be appointed and the terms and conditions of such appointment and remuneration payable be approved by the Board of Directors at a meeting which shall be subject to approval by a resolution at the next general meeting of the company and by the Central Government in case such appointment is at variance to the conditions specified in that Schedule:

Provided that a notice convening Board or general meeting for considering such appointment shall include the terms and conditions of such appointment, remuneration payable and such other matters including interest, of a director or directors in such appointments, if any:

Provided further that a return in the prescribed form shall be filed within sixty days of such appointment with the Registrar.

(5) Subject to the provisions of this Act, where an appointment of a managing director, whole-time director or manager is not approved by the company at a general meeting, any act done by him before such approval shall not be deemed to be invalid.

197. Overall maximum managerial remuneration and managerial remuneration in case of absence or inadequacy of profits.— (1) The total managerial remuneration payable by a public company, to its directors, including managing director and whole-time director, and its manager in respect of any financial year shall not exceed eleven per cent. of the net profits of that company for that financial year computed in the manner laid down in section 198 except that the remuneration of the directors shall not be deducted from the gross profits:

Provided that the company in general meeting may, with the approval of the Central Government, authorise the payment of remuneration exceeding eleven per cent. of the net profits of the company, subject to the provisions of Schedule V:

Provided further that, except with the approval of the company in general meeting,

(i) the remuneration payable to any one managing director; or whole-time director or manager shall not exceed five per cent. of the net profits of the company and if there is more than one such director remuneration shall not exceed ten per cent. of the net profits to all such directors and manager taken together;

(ii) the remuneration payable to directors who are neither managing directors nor whole-time directors shall not exceed,

(A) one per cent. of the net profits of the company, if there is a managing or whole-time director or manager;

(B) three per cent. of the net profits in any other case.

(2) The percentages aforesaid shall be exclusive of any fees payable to directors under sub-section (5).

(3) Notwithstanding anything contained in sub-sections (1) and (2), but subject to the provisions of Schedule V, if, in any financial year, a company has no profits or its profits are inadequate, the company shall not pay to its directors, including any managing or whole-time director or manager, by way of remuneration any sum exclusive of any fees payable to directors under sub-section (5) hereunder except in accordance with the provisions of Schedule V and if it is not able to comply with such provisions, with the previous approval of the Central Government.

(4) The remuneration payable to the directors of a company, including any managing or whole-time director or manager, shall be determined, in accordance with and subject to the provisions of this section, either by the articles of the company, or by a resolution or, if the articles so require, by a special resolution, passed by the company in general meeting and the remuneration payable to a director determined aforesaid shall be inclusive of the remuneration payable to him for the services rendered by him in any other capacity:

Provided that any remuneration for services rendered by any such director in other capacity shall not be so included if-

(a) the services rendered are of a professional nature; and

(b) in the opinion of the Nomination and Remuneration Committee, if the company is covered under sub-section (1) of section 178, or the Board of Directors in other cases, the director possesses the requisite qualification for the practice of the profession.

(5) A director may receive remuneration by way of fee for attending meetings of the Board or Committee thereof or for any other purpose whatsoever as may be decided by the Board:

Provided that the amount of such fees shall not exceed the amount as may be prescribed:

Provided further that different fees for different classes of companies and fees in respect of independent director may be such as may be prescribed.

(6) A director or manager may be paid remuneration either by way of a monthly payment or at a specified percentage of the net profits of the company or partly by one way and partly by the other.

(7) Notwithstanding anything contained in any other provision of this Act but subject to the provisions of this section, an independent director shall not be entitled to any stock option and may receive remuneration by way of fees provided under sub-section (5), reimbursement of expenses for participation in the Board and other meetings and profit related commission as may be approved by the members.

(8) The net profits for the purposes of this section shall be computed in the manner referred to in section 198.

(9) If any director draws or receives, directly or indirectly, by way of remuneration any such sums in excess of the limit prescribed by this section or without the prior sanction of the Central Government, where it is required, he shall refund such sums to the company and until such sum is refunded, hold it in trust for the company.

(10) The company shall not waive the recovery of any sum refundable to it under sub-section (9) unless permitted by the Central Government.

(11) In cases where Schedule V is applicable on grounds of no profits or inadequate profits, any provision relating to the remuneration of any director which purports to increase or has the effect of increasing the amount thereof, whether the provision be contained in the company’s memorandum or articles, or in an agreement entered into by it, or in any resolution passed by the company in general meeting or its Board, shall not have any effect unless such increase is in accordance with the conditions specified in that Schedule and if such conditions are not being complied, the approval of the Central Government had been obtained.

(12) Every listed company shall disclose in the Board’s report, the ratio of the remuneration of each director to the median employee’s remuneration and such other details as may be prescribed.

(13) Where any insurance is taken by a company on behalf of its managing director, whole-time director, manager, Chief Executive Officer, Chief Financial Officer or Company Secretary for indemnifying any of them against any liability in respect of any negligence, default, misfeasance, breach of duty or breach of trust for which they may be guilty in relation to the company, the premium paid on such insurance shall not be treated as part of the remuneration payable to any such personnel:

Provided that if such person is proved to be guilty, the premium paid on such insurance shall be treated as part of the remuneration.

(14) Subject to the provisions of this section, any director who is in receipt of any commission from the company and who is a managing or whole-time director of the company shall not be disqualified from receiving any remuneration or commission from any holding company or subsidiary company of such company subject to its disclosure by the company in the Board’s report.

(15) If any person contravenes the provisions of this section, he shall be punishable with fine which shall not be less than one lakh rupees but which may extend to five lakh rupees.

198. Calculation of profits. (1) In computing the net profits of a company in any financial year for the purpose of section 197,-

(a) credit shall be given for the sums specified in sub-section (2), and credit shall not be given for those specified in sub-section (3); and

(b) the sums specified in sub-section (4) shall be deducted, and those specified in sub-section (5) shall not be deducted.

(2) In making the computation aforesaid, credit shall be given for the bounties and subsidies received from any Government, or any public authority constituted or authorised in this behalf, by any Government, unless and except in so far as the Central Government otherwise directs.

(3) In making the computation aforesaid, credit shall not be given for the following sums, namely:

(a) profits, by way of premium on shares or debentures of the company, which are issued or sold by the company;

(b) profits on sales by the company of forfeited shares;

(c) profits of a capital nature including profits from the sale of the undertaking or any of the undertakings of the company or of any part thereof;

(d) profits from the sale of any immovable property or fixed assets of a capital nature comprised in the undertaking or any of the undertakings of the company, unless the business of the company consists, whether wholly or partly, of buying and selling any such property or assets:

Provided that where the amount for which any fixed asset is sold exceeds the written-down value thereof, credit shall be given for so much of the excess as is not higher than the difference between the original cost of that fixed asset and its written-down value;

(e) any change in carrying amount of an asset or of a liability recognised in equity reserves including surplus in profit and loss account on measurement of the asset or the liability at fair value.

(4) In making the computation aforesaid, the following sums shall be deducted, namely:

(a) all the usual working charges;

(b) directors’ remuneration;

(c) bonus or commission paid or payable to any member of the company’s staff, or to any engineer, technician or person employed or engaged by the company, whether on a whole-time or on a part-time basis;

(d) any tax notified by the Central Government as being in the nature of a tax on excess or abnormal profits;

(e) any tax on business profits imposed for special reasons or in special circumstances and notified by the Central Government in this behalf;

(f) interest on debentures issued by the company;

(g) interest on mortgages executed by the company and on loans and advances secured by a charge on its fixed or floating assets;

(h) interest on unsecured loans and advances;

(i) expenses on repairs, whether to immovable or to movable property, provided the repairs are not of a capital nature;

(f) outgoings inclusive of contributions made under section 181;

(k) depreciation to the extent specified in section 123;

(1) the excess of expenditure over income, which had arisen in computing the net profits in accordance with this section in any year which begins at or after the commencement of this Act, in so far as such excess has not been deducted in any subsequent year preceding the year in respect of which the net profits have to be ascertained;

(m) any compensation or damages to be paid in virtue of any legal liability including a liability arising from a breach of contract;

(n) any sum paid by way of insurance against the risk of meeting any liability such as is referred to in clause (m);

(o) debts considered bad and written off or adjusted during the year of account.

(5) In making the computation aforesaid, the following sums shall not be deducted, namely:

(a) income-tax and super-tax payable by the company under the Income-tax Act, 1961 (43 of 1961), or any other tax on the income of the company not falling under clauses (d) and (e) of sub- section (4);

(b) any compensation, damages or payments made voluntarily, that is to say, otherwise than in virtue of a liability such as is referred to in clause (m) of sub-section (4);

(c) loss of a capital nature including loss on sale of the undertaking or any of the undertakings of the company or of any part thereof not including any excess of the written-down value of any asset which is sold, discarded, demolished or destroyed over its sale proceeds or its scrap value;

(d) any change in carrying amount of an asset or of a liability recognised in equity reserves including surplus in profit and loss account on measurement of the asset or the liability at fair value.

- Provisions for appointment of MPs without approval from govt. (Sch. V)

SCHEDULE V

(See sections 196 and 197)

PART I

CONDITIONS TO BE FULFILLED FOR THE APPOINTMENT OF A MANAGING OR WHOLE-TIME DIRECTOR OR A MANAGER WITHOUT THE APPROVAL OF THE CENTRAL GOVERNMENT APPOINTMENTS

No person shall be eligible for appointment as a managing or whole-time director or a manager (hereinafter referred to as managerial person) of a company unless he satisfies the following conditions, namely:

(a) he had not been sentenced to imprisonment for any period, or to a fine exceeding one thousand rupees, for the conviction of an offence under any of the following Acts, namely:

(i) the Indian Stamp Act, 1899 (2 of 1899);

(ii) the Central Excise Act, 1944 (1 of 1944);

(iii) the Industries (Development and Regulation) Act, 1951 (65 of 1951);

(iv) the Prevention of Food Adulteration Act, 1954 (37 of 1954);

(v) the Essential Commodities Act, 1955 (10 of 1955);

‘[(vi) the Companies Act, 2013 (18 of 2013) or any previous company law;]

(vii) the Securities Contracts (Regulation) Act, 1956 (42 of 1956);

(viii) the Wealth-tax Act, 1957 (27 of 1957);

(ix) the Income-tax Act, 1961 (43 of 1961);

(x) the Customs Act, 1962 (52 of 1962);

(xi) the Competition Act, 2002 (12 of 2003);

(xii) the Foreign Exchange Management Act, 1999 (42 of 1999);

(xiii) the Sick Industrial Companies (Special Provisions) Act, 1985 (1 of 1986);

(xiv) the Securities and Exchange Board of India Act, 1992 (15 of 1992);

(xv) the Foreign Trade (Development and Regulation) Act, 1922 (22 of 1922);

(xvi) the Prevention of Money-Laundering Act, 2002 (15 of 2003);

2[(xvii) the Insolvency and Bankruptcy Cod; 2016 (31 of 2016);

(xviii) the Goods and Services Tax Act, 2017 (12 of 2017);

(xix) the Fugitive Economic Offenders Act, 2018 (17 of 2018).]

(b) he had not been detained for any period under the Conservation of Foreign Exchange and Prevention of Smuggling Activities Act, 1974 (52 of 1974):

Provided that where the Central Government has given its approval to the appointment of a person convicted or detained under sub-paragraph (a) or sub-paragraph (b), as the case may be, no further approval of the Central Government shall be necessary for the subsequent appointment of that person if he had not been so convicted or detained subsequent to such approval.

(c) he has completed the age of twenty-one years and has not attained the age of seventy years:

Provided that where he has attained the age of seventy years; and where his appointment is approved by a special resolution passed by the company in general meeting, no further approval of the Central Government shall be necessary for such appointment;

(d) where he is a managerial person in more than one company, he draws remuneration from one or more companies subject to the ceiling provided in section V of Part II;

(e) he is resident of India.

Explanation I.—For the purpose of this Schedule, resident in India includes a person who has been staying in India for a continuous period of not less than twelve months immediately preceding the date of his appointment as a managerial person and who has come to stay in India,

(i) for taking up employment in India; or

(ii) for carrying on a business or vacation in India.

Explanation H.—This condition shall not apply to the companies in Special Economic Zones as notified by Department of Commerce from time to time:

Provided that a person, being a non-resident in India shall enter India only after obtaining a proper Employment Visa from the concerned Indian mission abroad. For this purpose, such person shall be required to furnish, along with the visa application form, profile of the company, the principal employer and terms and conditions of such person’s appointment.

PART II

REMUNERATION

Section I. Remuneration payable by companies having profits:

Subject to the provisions of section 197, a company having profits in a financial year may pay remuneration to a managerial person or persons l[or other director or directors] not exceeding the limits specified in such section.

2[Section IL—Remuneration payable by companies having no profit or inadequate profit 3***:

Where in any financial year during the currency of tenure of a managerial person 1[or other director], a company has no profits or its profits are inadequate, it may, 3***, pay remuneration to the managerial person l[or other director] not exceeding the limits under (A) and (B) given below:

5[Provided that the remuneration in excess of above limits may be paid] if the resolution passed by the shareholders is a special resolution.

Explanation. It is hereby clarified that for a period less than one year, the limits shall be pro-rated.

(B) In case of a managerial person who is functioning in a professional capacity, Iremuneration as per item (A) may be paid], if such managerial person is not having any interest in the capital of the company or its holding company or any of its subsidiaries directly or indirectly or through any other statutory structures and not having any direct or indirect interest or related to the directors or promoters of the company or its holding company or any of its subsidiaries at any time during the last two years before or on or after the date of appointment and possesses graduate level qualification with expertise and specialised knowledge in the field in which the company operates:

Provided that any employee of a company holding shares of the company not exceeding 0.5% of its paid up share capital under any scheme formulated for allotment of shares to such employees including Employees Stock Option Plan or by way of qualification shall be deemed to be a person not having any interest in the capital of the company:

Provided further that the limits specified under items (A) and (B) of this section shall apply, if-

(i) payment of remuneration is approved by a resolution passed by the Board and, in the case of a company covered under sub-section (1) of section 178 also by the Nomination and Remuneration Committee;

(ii) 2[the company has not committed any default in payment of dues to any bank or public financial institution or non-convertible debenture holders or any other secured creditor, and in case of default, the prior approval of the bank or public financial institution concerned or the non-convertible debenture holders or other secured creditor, as the case may be, shall be obtained by the company before obtaining the approval in the general meeting;]

(iii) an ordinary resolution or a special resolution, as the case may be, has been passed for payment of remuneration as per 3*** item (A) or a special resolution has been passed for payment of remuneration as per item (B), at the general meeting of the company for a period not exceeding three years.

(iv) a statement along with a notice calling the general meeting referred to in clause (iii) is given to the shareholders containing the following information, namely:-

I. General information:

(1) Nature of industry

(2) Date or expected date of commencement of commercial production

(3) In case of new companies, expected date of commencement of activities as per project approved by financial institutions appearing in the prospectus

(4) Financial performance based on given indicators

(5) Foreign investments or collaborations, if any.

II. Information about the appointee:

(1) Background details

(2) Past remuneration

(3) Recognition or awards

(4) Job profile and his suitability

(5) Remuneration proposed

(6) Comparative remuneration profile with respect to industry, size of the company, profile of the position and person (in case of expatriates the relevant details would be with respect to the country of his origin)

(7) Pecuniary relationship directly or indirectly with the company, or relationship with the managerial personnel, if any.

III. Other information:

(1) Reasons of loss or inadequate profits

(2) Steps taken or proposed to be taken for improvement

(3) Expected increase in productivity and profits in measurable terms

IV. Disclosures:

The following disclosures shall be mentioned in the Board of Director’s report under the heading “Corporate Governance”, if any, attached to the financial statement:

(i) all elements of remuneration package such as salary, benefits, bonuses, stock options, pension, etc., of all the directors;

(ii) details of fixed component and performance linked incentives along with the performance criteria;

(iii) service contracts, notice period, severance fees; and

(iv) stock option details, if any, and whether the same has been issued at a discount as well as the period over which accrued and over which exercisable.

Explanation: For the purposes of Section II of this part, “Statutory Structure” means any entity which is entitled to hold shares in any company formed under any statute. ]

Section III. Remuneration payable by companies having no profit or inadequate ‘***profit in certain special circumstances:

In the following circumstances a company may, ‘***, pay remuneration to a managerial person 2[or other director] in excess of the amounts provided in Section II above:

(a) where the remuneration in excess of the limits specified in Section I or Section II is paid by any other company and that other company is either a foreign company or has got the approval of its shareholders in general meeting to make such payment, and treats this amount as managerial remuneration for the purpose of section 197 and the total managerial remuneration payable by such other company to its managerial persons including such amount or amounts is within permissible limits under section 197.

3[(b) where the company-

(i) is a newly incorporated company, for a period of seven years from the date of its incorporation, or

(ii) is a sick company, for whom a scheme of revival or rehabilitation has been ordered by the Board for Industrial and Financial Reconstruction for a period of five years from the date of sanction of scheme of revival, or

(iii) is a company in relation to which a resolution plan has been approved by the National Company Law Tribunal under the Insolvency and Bankruptcy Code, 2016 (31 of 2016) for a period of five years from the date of such approval,

it may pay 4[any remuneration to its managerial persons 2[or other directors]].]

(c) where remuneration of a managerial person 2[or other director] exceeds the limits in Section II but the remuneration has been fixed by the Board for Industrial and Financial Reconstruction or the National Company Law Tribunal:

Provided that the limits under this Section shall be applicable subject to meeting all the conditions specified under Section II and the following additional conditions:-

(i) except as provided in para (a) of this Section, the managerial person is not receiving remuneration from any other company;

(ii) the auditor or Company Secretary of the company or where the company has not appointed a Secretary, a Secretary in whole-time practice, certifies that all secured creditors and term lenders have stated in writing that they have no objection for the appointment of the managerial person jor other director] as well as the quantum of remuneration and such certificate is filed along with the return as prescribed under sub-section (4) of section 196.

(iii) the auditor or Company Secretary or where the company has not appointed a secretary, a secretary in whole-time practice certifies that there is no default on payments to any creditors, and all dues to deposit holders are being settled on time.

2* * * * *

1[Explanation.-For the purposes of Section I, Section II and Section III, the term “or other director” shall mean a non-executive director or an independent director.]

Section IV.— Perquisites not included in managerial remuneration:

1. A managerial person shall be eligible for the following perquisites which shall not be included in the computation of the ceiling on remuneration specified in Section II and Section III:

(a) contribution to provident fund, superannuation fund or annuity fund to the extent these either singly or put together are not taxable under the Income-tax Act, 1961(43 of 1961);

(b) gratuity payable at a rate not exceeding half a month’s salary for each completed year of service;

and

(c) encashment of leave at the end of the tenure.

2. In addition to the perquisites specified in paragraph 1 of this section, an expatriate managerial person (including a non-resident Indian) shall be eligible to the following perquisites which shall not be included in the computation of the ceiling on remuneration specified in Section II or Section III

(a) Children’s education allowance: In case of children studying in or outside India, an allowance limited to a maximum of Rs. 12,000 per month per child or actual expenses incurred, whichever is less.

Such allowance is admissible up to a maximum of two children.

(b) Holiday passage for children studying outside India or family staying abroad: Return holiday passage once in a year by economy class or once in two years by first class to children and to the members of the family from the place of their study or stay abroad to India if they are not residing in India, with the managerial person.

(c) Leave travel concession: Return passage for self and family in accordance with the rules specified by the company where it is proposed that the leave be spent in home country instead of anywhere in India.

Explanation I.— For the purposes of Section II of this Part, “effective capital” means the aggregate of the paid-up share capital (excluding share application money or advances against shares); amount, if any, for the time being standing to the credit of share premium account; reserves and surplus (excluding revaluation reserve); long-term loans and deposits repayable after one year (excluding working capital loans, overdrafts, interest due on loans unless funded, bank guarantee, etc., and other short-term arrangements) as reduced by the aggregate of any investments (except in case of investment by an investment company whose principal business is acquisition of shares, stock, debentures or other securities),accumulated losses and preliminary expenses not written off.

Explanation II.— (a) Where the appointment of the managerial person is made in the year in which company has been incorporated, the effective capital shall be calculated as on the date of such appointment;

(b) In any other case the effective capital shall be calculated as on the last date of the financial year preceding the financial year in which the appointment of the managerial person is made.

Explanation III.— For the purposes of this Schedule, “family” means the spouse, dependent children and dependent parents of the managerial person.

Explanation IV.— The Nomination and Remuneration Committee while approving the remuneration under Section II or Section III. shall—

(a) take into account, financial position of the company, trend in the industry, appointee’s qualification, experience, past performance, past remuneration, etc.;

(b) be in a position to bring about objectivity in determining the remuneration package while striking a balance between the interest of the company and the shareholders.

Explanation V.__ For the purposes of this Schedule, “negative effective capital” means the effective

capital which is calculated in accordance with the provisions contained in Explanation I of this Part is less than zero.

Explanation VI.— For the purposes of this Schedule:-

1* * * *

(B) “Remuneration” means remuneration as defined in clause (78) of section 2 and includes reimbursement of any direct taxes to the managerial person.

Section V. —Remuneration payable to a managerial person in two companies:

Subject to the provisions of sections Ito IV, a managerial person shall draw remuneration from one or both companies, provided that the total remuneration drawn from the companies does not exceed the higher maximum limit admissible from any one of the companies of which he is a managerial person.

PART III

Provisions applicable to Parts I and II of this Schedule

1. The appointment and remuneration referred to in Part I and Part II of this Schedule shall be subject to approval by a resolution of the shareholders in general meeting.

2. The auditor or the Secretary of the company or where the company is not required to appointed a Secretary, a Secretary in whole-time practice shall certify that the requirement of this Schedule have been complied with and such certificate shall be incorporated in the return filed with the Registrar under subsection (4) of section 196.

PART IV

The Central Government may, by notification, exempt any class or classes of companies from any of the requirements contained in this Schedule.

******

(Author can be reached at email address satishagarwal307@yahoo.com or on Mobile No. 9811081957)

Disclaimer : The contents of this article are solely for informational purpose. Neither this article nor the informations as contained herein constitutes a contract or will form the basis of a contract. The material contained in this article does not constitute or substitute professional advice that may be required before acting on any matter. While every care has been taken in the preparation of this article to ensure its accuracy at the time of publication. Satish Agarwal assumes no responsibility for any error which despite all precautions may be found herein. We shall not be liable for direct, indirect or consequential damages if any arising out of or in any way connected with the use of this article or the informations as contained herein.

(Republished with amendments)

Author Bio