The Disciplinary Committee of the Institute of Chartered Accountants of India (ICAI) has reprimanded CA. Mohan Lal Jain for professional misconduct. The Committee found him guilty under Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949, for failing to exercise due diligence in his professional duties. The case centered on the audit report of Capital18 Fincap Private Limited for the financial year 2013-14. The company was engaged in Non-Banking Financial Company (NBFC) activities but did not possess a mandatory Certificate of Registration (CoR) from the Reserve Bank of India (RBI), as required by Section 45IA of the RBI Act, 1934. CA. Jain, as the statutory auditor, failed to report this non-compliance in his audit report and did not submit an exception report to the RBI, a requirement under the ‘Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008’. Despite the Respondent’s plea for leniency, citing a warning from the RBI, the Committee concluded that the professional misconduct was clearly established due to the company meeting the Principal Business Criteria for an NBFC in FY 2013-14 without the necessary registration. Consequently, the Committee ordered a reprimand, considering the gravity of the oversight.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

[DISCIPLINARY COMMITTEE [BENCH-IV (2024-2025)]

[Constituted under Section 218 of the Chartered Accountants Act, 1949]

ORDER UNDER SECTION 218(31 OF THE. CHARTERED ACCOUNTANTS ACT, 1949 READ WITH RULE 19(1) OF THE CHARTERED ACCOUNTANTS (PROCEDURE OF INVESTIGATIONS OF PROFESSIONAL AND OTHER MISCONDUCT AND CONDUCT OF CASES) RULES, 2007.

[PPR&IP/104/16/10101341/161F/17/0C/1548/2022]

In the matter of:

CA. Mohan (al Jain

M/s. Mohan L Jain & Co.,…..Respondent

MEMBERS PRESENT:

1. Ranjeet Kumar Agarwal, Presiding Officer (In person)

2. Shri Jiwesh Nandan, I.A.S (Retd.), Government Nominee (In person)

3. Dakshita Das, I.R.A.S. (Retd.), Government Nominee (Through VC)

4. Mangesh P Kinare, Member (Through VC)

5. Abhay Chhajed, Member (In person)

DATE OF HEARING : 19th MARCH, 2024

DATE OF ORDER :16th May, 2024

1. That vide Findings dated 16.01.2024 under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007, the Disciplinary Committee was inter-alia of the opinion that Mohan Lai Jain (hereinafter referred to as the Respondent”) is GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part I of Second Schedule to the Chartered Accountants Act, 1949.

2. That pursuant to the said Findings, an action under Section 218(3) of the Chartered Accountants (Amendment) Act, 2006 was contemplated against the Respondent and a communication was addressed to him thereby granting an opportunity of being heard in person/ through video conferencing and to make representation before the Committee on 19th March 2024.

3. The Committee noted that on the date of hearing on 19th March 2024, the Respondent was present through video conferencing and made his verbal representation on the Findings of the Committee. The Respondent stated that Reserve Bank of India (Informant) had closed the case against him after giving him a warning and had stated that it would not pursue the present matter before Disciplinary Committee. The Respondent pleaded to the Committee to take a lenient view in the matter.

4. The Committee considered the reasoning as contained in Findings holding the Respondent ‘Guilty’ of Professional Misconduct vis-a-vis verbal representation of the Respondent.

5. Thus, keeping in view the facts and circumstances of the case, material on record including verbal representation of the Respondent on the Findings, the Committee noted that the Company was carrying the business of NBFC and was falling under the Principle Business Criteria (PBC) for financial year 2013-2014. The Committee held that the Respondent in his Audit Report of the Company for the financial year 2013-14 had failed to report that the Company was engaged in the business of NBFC without certificate of registration. The Respondent was required to submit Exception Report but he failed to submit exception report to comply with paragraph 5 of ‘Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008.

6. Further, as per Section 451A of the RBI Act, 1934, it is mandatory for a Company to obtain Certificate of Registration (CoR) from Reserve Bank of India before commencing or to carry on business of a non-banking financial institution. But in the instant matter, the Company failed to get Certificate of Registration (CoR) and the Respondent as statutory auditor did not report the same. Hence, the Professional Misconduct on the part of the Respondent is clearly established as spelt out in the Committee’s Findings dated 16th January 2024, which is to be read in consonance with the instant Order being passed in the case.

7. Accordingly, the Committee was of the view that the ends of justice would be met if punishment is given to him in commensurate with his Professional Misconduct.

8. Thus, the Committee ordered that the Respondent i.e., CA. Mohan Lal Jain, New Delhi, be REPRIMANDED, under 218(3)(a) of the Chartered Accountants Act,1949.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(SHRI JIWESH NANDAN, I.A.S. {RETD.})

GOVERNMENT NOMINEE

Sd/-

(MS. DAKSHITA DAS, 1.12.A.S.{RETD.})

GOVERNMENT NOMINEE

Sd/-

(CA. MANGESH P KINARE)

MEMBER

Sd/-

(CA. ABHAY CHHAJED)

MEMBER

CONFIDENTIAL

DISCIPLINARY COMMITTEE BENCH – IV (2023-2024)]

(Constituted under Section 2113 of the Chartered Accountants Act, 1949]

Findings under Rule 18(17) of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of Cases) Rules, 2007.

File No.: PPR/P/104/16/DD/341/INF/17/DC/1548/2022

In the matter of:

CA. Mohan Lal Jain

M/s. Mohan L. Jain & Co.,

MEMBERS PRESENT:

CA. Ranjeet Kumar Agarwal, Presiding Officer (In person)

Ms. Dakshita Das, I.R.A.S (Retd.), Govt. Nominee (In person)

CA. Mangesh P. Kinare, Member (In person)

CA. Cotha S Srinivas, Member (In person)

DATE OF FINAL HEARING : 25th August,2023

PARTIES PRESENT:

CA. Mohan Lal Jain: Respondent (through VC mode)

CA. Lakshya Gupta: Counsel for the Respondent (through VC mode)

1. Background of the Case:

The balance sheets as on 31st March, 2014 and 31St March, 2015 of Capital18 Fincap Private Limited (hereinafter referred to as the “Company’) audited by the Respondent firm, The Company was carrying on Non Banking Financial Institution (NBFI) activity without obtaining Certificate of Registration (CoR) from the Reserve Bank of India.

2. Charges in Brief: –

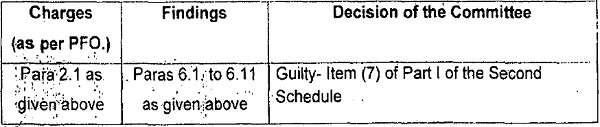

2.1 The Respondent firm audited the financial statements of M/s. Capital18 Fincap Private Limited (hereinafter referred as “the Company”). As per the balance sheets of the Company as on 31st March, 2014 and 31st March, 2015 audited by the Respondent firm, the Company was carrying on Non Banking Financial Institution (NBFI) activity without obtaining Certificate of Registration (CoR) from the Reserve Bank of India, which was in violation of provisions of Section 45-IA of the Reserve Bank of India Act, 1934. The Respondent has not submitted any exception report in the matter to the RBI, as per Section 5 of “Not-Banking” Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008, in terms of which the Statutory Auditors was required to send an Exception Report to the RBI.

3. The relevant issues discussed in the Prima fade opinion dated 06th July 2020 formulated by Director (Discipline) in the matter in brief is given below:-

3.1 As per RBI circular RBI/2011-12/446 DNBS (PD)CC.No.259 /03.02.59/2011- 12 dated March 15, 2012 “Investments in fixed deposits cannot be treated as financial assets and receipt of interest income on fixed deposits with banks cannot be treated as income from financial assets as these are not covered under the activities mentioned in the definition of “financial Institution” in Section 451(c) of the RBI Act 1934.”

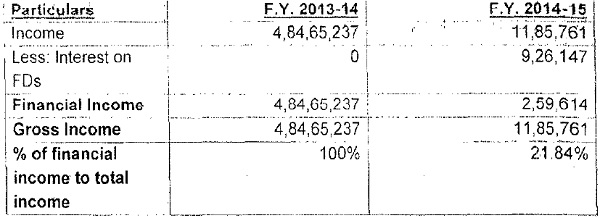

3.2 In view of the said RBI circular, fixed deposits only with commercial bank cannot be treated as financial assets and accordingly, interest on fixed deposit with commercial banks only cannot be treated as financial income, In the instant matter, the Respondent brought on record that interest on fixed deposit for the financial year 2014-15 was Rs.9,26,147/-. After receipt of the allegation letter dated 9th August 2016 from the RBI, the Respondent provided details of interest on fixed deposit vide his letter dated 1st August 2017 to the RBI. The RBI appears to be satisfied with the said reply of the Respondent in respect of the financial year 2014-15 as the RBI, after issuance of Information letter to the Respondent by the Disciplinary Directorate, vide its letter dated 25th October 2017 did not raise question in respect of financial year 2014-15 and it raised the question in respect of the financial year 2013-14 only.

3.3 Further, the Company was not fulfilling the principal business criteria for being NBFC for the financial year 2014-15 as the financial income from the financial assets was less than 50% of the total income. Hence, with respect to the financial year 2014-15, it cannot be stated that the Company was required to obtain a Certificate of Registration from the RBI and accordingly, there was no need for the Respondent to submit an exception report to the RBI.

3.4 In respect of the financial year 2013-14, it is noted that the financial assets of the Company are more than 50% of total assets, as well as income from financial assets is also more than 50% of the gross total income. Hence, it can be opined that both the conditions were satisfied by the Company and accordingly the Company was required to get itself registered as NBFC with RBI.

3.5 In the financial year 2013-14, the Company was carrying the business of NBFC and was falling under the Principle Business Criteria (PBC). The Respondent did not claim that he has mentioned in his audit report that the Company is carrying out the activity of NBFI. The Respondent in his Audit Report of the Company for the financial years 2013-14 failed to report that the Company was carrying an NBFC without a registration certificate. The Company had not applied for registration and the Respondent was required to submit an Exception Report. He failed to submit an exception report to comply with ‘Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008 (now para 5 of NBFC Auditor’s Report (Reserve Bank) Directions, 2016 in terms of Section 451A of the RBI Act 1934, it is mandatory for a Company to obtain Certificate of Registration (CoR) from Reserve Bank of India before commencing or to carry on business of a non-banking financial institution.

3.6, The Director (Discipline) in the Prima Facie Opinion dated 06th July,2020 has held the Respondent prima facie guilty of Professional Misconduct falling within the meaning Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949, The said Item of the Schedule to the Act, states as under: –

Item (7) of part of Second Schedule

“A chartered accountant in practice shall be deemed to be guilty of professional misconduct if he —

(7) does not exercise due diligence or is grossly negligent in the conduct of his professional duties”.

3.7 The Prima Facie Opinion formed by the Director (Discipline) dated 61h July 2020 was considered by the Disciplinary Committee at its meeting held on 8th April 2022, at New Delhi. The Committee on consideration of the same, concurred with the reasons given against the charges and thus, agreed with the prima facie opinion of the Director (Discipline) that the Respondent is GUILTY of Professional Misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants Act, 1949 and accordingly, decided to proceed further under Chapter V of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of cases) Rules 2007. The Committee also directed the Directorate that in terms of the provisions of sub-rule (2) of Rule 18, the prima facie opinion formed by the Director be sent to the Respondent including particulars or documents relied upon by the Director, if any, during the course of formation of prima fade opinion and the Respondent be asked to submit his Written Statement in terms of the aforesaid Rules, 2007.

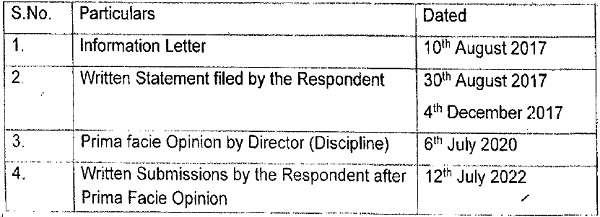

4. Date(s) of written submissions/pleadings by parties:

The relevant details of the filing of documents in the instant case by the parties are given below: –

Brief Facts of the Proceedings:

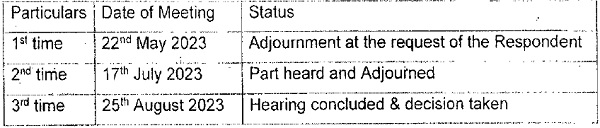

5.1 The details of the hearing fixed and held/adjourned in said matter are given as under:

5.2 On the day of the First Hearing of the case on 22nd May 2023, the Committee noted that the Respondent was not present. The Respondent sought adjournment over the phone stating that he was in hospital and even unable to connect through video conferencing. The Committee acceded to his request and adjourned the case to the next date.

5.3 On the next date of the hearing on 171h July 2023, the Committee noted that the Respondent was present through Video conferencing mode and was put on oath. The Committee enquired from the Respondent as to whether he was aware of the charges and charges against the Respondent were read out. On the same, the Respondent replied in the affirmative and pleaded Not Guilty to the charges levelled against him. Thereafter, as per Rule 18 (9) of the Chartered Accountants (Procedure of Investigation of Professional and Other Misconduct and Conduct of CaseS) Rules, 2007, the Committee adjourned the case to later date and accordingly, the matter was part heard and adjourned.

5.4 On the day of the final hearing on 25th August 2023, the Committee noted that the Respondent along with Counsel were present through Video conferencing mode. The case was part-heard, and the Respondent was already on oath. The Committee asked the Counsel for the Respondent to make his submissions in the matter. The Counsel for the Respondent submitted that the Company has not accepted any public deposits during the year. Further, he referred to an Order of Disciplinary Committee dated 29/01/2019 bearing reference no: PPR/P/15/1\1/13/DD/6/N/INF/13/DC/573/2017 in case of CA Dinesh Kumar, Gupta, where facts were identical to this, case arid the Respondent had been held not guilty of professional misconduct by the Committee in that particular case.

5.5 The Counsel for the Respondent further submitted that Reserve Bank of India Act, 1934 was not applicable in the instant matter as the Company had not lent any business loan during the. period nor had accepted external borrowing from public which were the requirements to be met so as to get covered within the provisions of said Act; and it merely had certain investments in group concerns and’ booked certain gains on transfer of investment during that period.

5.6 Further, the Counsel for the Respondent referred to a letter of the Reserve Bank of India (Informant) and submitted that vide letter dated 22/03/2018 addressed to the Respondent, the RBI itself had stated that it had decided not to pursue further the case pending with the Disciplinary Committee of ICAI.

5.7 After detailed deliberations, and on consideration of the facts of the case, various documents on record as well as oral submissions and written submissions made by the Counsel of the Respondent before it, the Committee concluded the hearing in the instant case.

6. Findings of the Committee:

The Committee noted the background of the case as well as oral and written submissions made by the Respondent, documents/material on record and gives its findings as under:

6.1 The Committee noted that in prima facie opinion, the Respondent has been held guilty in respect of financial year 2013-14 as financial assets of the Company were more than 50% of total assets, as well as income from financial assets is also more than 50% of the gross total income. Hence, the Committee gives its findings in respect of financial year 2013-2014.

6.2 The Committee refers press release bearing No. 1269 dated 08th April 1999 which states as under:

“The Reserve Bank of India today announced that in order to identify a particular company as a non- banking financial company (NBFC), it will consider both, the assets and the income pattern as evidenced from the last audited balance sheet of the company to decide its principal business. The company will be treated as an NBFC if its financial assets are more than 50 percent of its total assets (netted off by intangible assets) and income from financial assets should be more than 50 percent of the gross income. Both these tests are required to be satisfied as the determinant factor for principal business of a company.”

6.3 Further, the Committee noted that the provision of Section 45-IA of the Reserve Bank of India Act,1934, relevant paragraph of which states as under: –

“(1) Notwithstanding anything contained in this Chapter or in any other law for the time being in force, no non-banking financial company shall commence or carry on the business of a non-banking financial institution without—

(a) obtaining a certificate of registration issued under this Chapter and

(b) having the net owned fund of twenty-five lakh rupees or such other amount, not exceeding two hundred lakh rupees, as the Bank may, by notification in the Official Gazette, specify.”

6.4 Further, as per para 15 of Non-Banking Financial (Non-deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007, the Statutory auditor has to submit a certificate to RBI, relevant paragraph of which states as under: –

‘Every non-banking financial company shall submit a Certificate from its Statutory Auditor that it is engaged in the business of non-banking financial institution requiring it to hold a Certificate of Registration under Section 45-IA of the RBI Act. A certificate from the Statutory Auditor in this regard with reference to the position of the company as at end of the financial year ended March 31 may be submitted to the Regional Office of the Department of Non-Banking Supervision under whose jurisdiction the non-banking financial company is registered, (within one month from the date of finalization of the balance sheet and in any case not later than December 30th of that year] Such certificate Shall also indicate the asset / income pattern of the non-banking financial company for making it eligible for classification as Asset Finance Company, Investment Company, or Loan Company’.

6.5 Moreover, in terms of NBFC Regulations – certificate of Registration (COR) issued under Section 45-IA of the RBI Act, 1934 – continuation of business of NBFC submission of Statutory Auditors’ Certificate,. “The company will be treated as a non-banking financial company (NBFC) if its financial assets are more than 50 per cent of its total assets (netted off by intangible assets) and income from financial assets is more than 50 per cent of the gross income. Both these tests are required to be satisfied as the determinant factor for principal business of a company”. (Emphasis Provided)

Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008″ cast duty on the Auditor of an NBFC to report the following in his audit report: ”3. Matters to be included in the auditor’s report

The auditor’s report on the accounts of a non-banking financial company shall include a statement on the following matters, namely:

(A) In the case of all non-banking financial companies

“I, Whether the company is engaged in the business of non-banking financial institution and whether it has obtained a Certificate of Registration (CoR) from the Bank

II. In the case of a company holding CoR issued by the Bank, whether that company is entitled to continue to hold such CoR in terms of its asset/income pattern as on March 31 of the applicable year “

It further states as under: –

“5. Obligation of auditor to submit an exception report to the Bank

(I) Where, in the case of a non-banking financial company, the statement regarding any of the items referred to in paragraph 3 above, is unfavorable or qualified, or in the opinion of the auditor the company has not complied with:

(a) the provisions of Chapter III B of Reserve Bank of India Act, 1934 (Act 2 of 1934); or

(b) the Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 1998; or

(c) Non-Banking Financial (Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007; or

(d) Non-Banking Financial (Non- Deposit Accepting or Holding) Companies Prudential Norms (Reserve Bank) Directions, 2007;

it shall be the obligation of the auditor to make a report–containing the details of such unfavorable or qualified statements and/or about the non-compliance, as the case may be, in respect of the company to the concerned Regional Office of the Department of Non-Banking Supervision of the Bank under whose jurisdiction the registered office of the company is located as per Second Schedule to the Non-Banking Financial Companies Acceptance of Public .Deposits (Reserve Bank) Directions, 1998.”

6.6 The Committee noted that as per press release bearing No. 1269 dated 08th April 1999, assets and income pattern have to be considered from the last audited balance sheet of the Company to decide principal business. And as per the audited balance sheet for the year ended 31st March 2014, the bifurcation of the financial Assets and Income pattern of the Company were as under: –

Financial Assets Pattern:

| 31.03.2014 | 31.03.2015 | |

| Non Current Investment

Current Investment |

1,16,30,89,196 | 1,25,33,93,325 |

| 8,00,000 | 8,82,902 | |

| Short term loans & Advance (excluding income tax paid) | 2,01,253 | 1,03,72,608 |

| Other Current Assets |

1,57,36,400 | 1,01,11,111 |

| Total | 1,180,922,629 | 1,265,124,626 |

| Total Assets as per B/S | 1,179,826,849 | 1,274,759,946 |

| % to Total Assets | 99.88% | 99 15% |

Financial Income Pattern:-

6.7 In view of above, the Committee noted that the Company was not fulfilling the principal business criteria for being NBFC for the financial year 2014-15 as the financial income from the financial assets were less than 50% of the total income; however, in respect of the financial year 2013-14, both the conditions were satisfied by the Company thereby falling under the Principal Business Criteria and accordingly the Company was required to get itself registered as NBFC with RBI.

6.8 The Committee noted that at this stage the Counsel of the Respondent referred to an Order of Disciplinary Committee dated 29th January 2019 bearing reference no. PPR/P/15/N/13/DD/6/N/INF/13/DC/573/2017 in case of CA. Dinesh Kumar Gupta, claiming that facts were identical to this case and the Respondent had been held not guilty of professional misconduct by the Committee in that particular case. In this respect, the Committee was of the view that each case is independent having different facts and merits and this plea is not applicable to this case.

6.9. The Committee further noted that the Counsel for the Respondent has made reference to a letter dated 22nd May 2018 of RBI, wherein it was stated that “We have examined the submissions made in the above letter. Since you have assured that you will be more strict and careful in future, the Bank has decided not to pursue further the case pending with the Disciplinary Committee of CAI. You are advised to exercise your judgement and strictly adhere to the directions of the Bank.” The Committee observed that RBI had neither written in this regard to ICAI nor marked a copy of letter addressed to Respondent to ICAI. Moreover, the Committee was of the view that it was an Information case treated as per Rule 7 of the Chartered Accountants (Procedure of Investigations of Professional and Other Misconduct and Conduct of cases) Rules 2007 and Rule 6 (i.e. withdrawal of Complaint) of said Rules permit withdrawal of complaint cases only and not applicable to the Information cases, hence, said pleas of the Counsel is not maintainable.

6.10. On the basis of above, the Committee was of the opinion that the Company was carrying the business of NBFC and was falling under the Principle Business Criteria (PBC) for financial year 2013-2014. The Respondent in his Audit Report of the Company for the financial years 2013-14 had failed to report that the Company was engaged in the business of NBFC without certificate of registration and accordingly the Respondent was required to submit Exception Report. The Respondent failed to submit exception report to comply with paragraph 5 of ‘Non-Banking Financial Companies Auditor’s Report (Reserve Bank) Directions, 2008.

6.11. Further, as per Section 451A of the RBI Act, 1934, it is mandatory for a Company to obtain Certificate of Registration (CoR) from Reserve Bank of India before commencing or to carry on business of a non-banking financial institution. But in instant matter, the Company failed to get CoR and Respondent as Statutory auditor did not report the same. Accordingly, it is Viewed by the Committee that the Respondent has failed to exercise due diligence in reporting and thus is GUILTY of professional misconduct falling within the meaning of Item (7) of Part I of the Second Schedule to the Chartered Accountants, Act, 1949.

7. Conclusion

In view of the above findings stated in the above paras; vis-a-vis material on record, the, Committee gives its charge-wise findings as under:

8. In view of the above observations. considering the submissions of the Respondent and documents on record, the Committee held the Respondent GUILTY of Professional Misconduct falling within the meaning of item (7) of Part 1 of Second Schedule to the Chartered Accountants Act, 1949.

Sd/-

(CA. RANJEET KUMAR AGARWAL)

PRESIDING OFFICER

Sd/-

(MS. DAKSHITA DAS, LR.A.S {RETD.})

GOVERNMENT NOMINEE

Sdl-

(CA. MANGESH P KINARE)

MEMBER

Sd/-

(CA. COTHA S SRINIVAS)

MEMBER

DATE: 16.01.2024

PLACE: New Delhi