A defective return under Section 139(9) of the Income Tax Act, 1961 occurs when crucial information is either omitted or inaccurately entered in an income tax return. This triggers the issuance of a defective return notice by the IT Department, aimed at rectifying the inaccuracies.

Reasons and Situations Leading to Defective Return Notices:

1. Incomplete ITR: This encompasses instances of name mismatches, missing personal information, or incomplete bank details on the income tax return.

2. Missing Tax Information: Failing to provide essential tax details such as TDS (Tax Deducted at Source), TCS (Tax Collected at Source), or Advance tax information.

3. TDS Claimed Without Corresponding Income: When TDS is claimed, but the associated income (e.g., interest from Fixed Deposits or Bank Interest) is not declared for taxation.

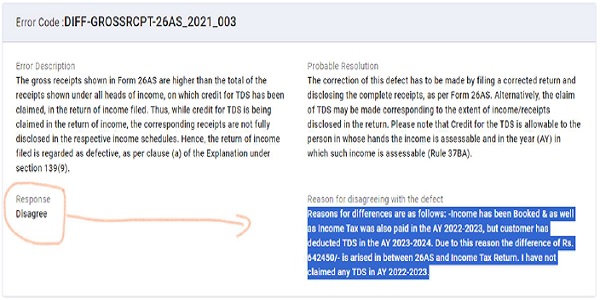

4. Discrepancy in Gross Receipts: If the gross receipts cited in Form 26AS, for which TDS credit has been claimed, surpass the total receipts declared across all income heads in the return.

5. Nil Income but Tax Liability: When “Gross Total Income” and all income heads are listed as “nil” or “0”, despite tax liability having been calculated and paid.

6. Incomplete Business or Profession Details: Taxpayers with income under the “Profits and gains of Business or Profession” category are expected to provide a Balance Sheet and Profit and Loss Account, which might be missing.

Receiving and Responding to Defective Return Notices:

The IT Department communicates defective return notices via the email ID provided during the income tax return filing. Typically sent by the Central Processing Centre (CPC), the subject line includes ‘Communication u/s 139(9) for PAN AWZXXXXXXX for the A.Y.2023-24’.

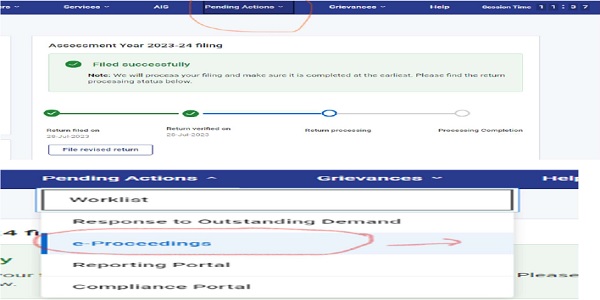

Alternatively, taxpayers can access these notices on the Income Tax portal, under the “Pending Action” tab and “E-Proceedings” section.

Responding within a 15-day timeframe is crucial. Taxpayers must rectify the defects identified by the Income Tax Department by revising their return within this period. In case the revision cannot be completed within 15 days, an extension can be requested from the local Assessing Officer.

How to revise your income tax return in response to the notice:

Step 1: Check the reason for defective notice. –

An income tax return (ITR) may be marked defective for various reasons. Say you have received a defective notice because there is a mismatch between income in Form 26AS and your ITR. Download Form 26AS from the IT portal and check if you have earned any income on which tax has been deducted, for e.g.:

1. Transfer- Capital Gain etc

2. Any other Income Interest income from term deposits;

3. dividend income or

4. Digital Currency-115BAH

Step 2: Agree or Disagree

Agree:

If you have identified the error and want to correct that you need to first prepare Revised return/Correct return in the Excel template as available at Income Tax official Portal- Link-

https://www.incometax.gov.in/iec/foportal/downloads/income-tax-returns

or

Prepare revised return in any other software tool available to you and generate a Json file.

Disagree- If you think the return is ok then Mark as Disagree and mention reasons thereof like

Reasons for differences are as follows: -Income has been Booked & as well as Income Tax was also paid in the AY 2022-2023, but customer has deducted TDS in the AY 2023-2024. Due to this reason the difference of Rs. 642450/- is arises in between 26AS and Income Tax Return. I have not claimed any TDS in AY 2022-2023.

Step 3: Once you prepare your Revised return or ready with the Reasons as applicable, log in to Income Tax Portal and respond.

– Click on pending action tab and e-proceeding under sub head

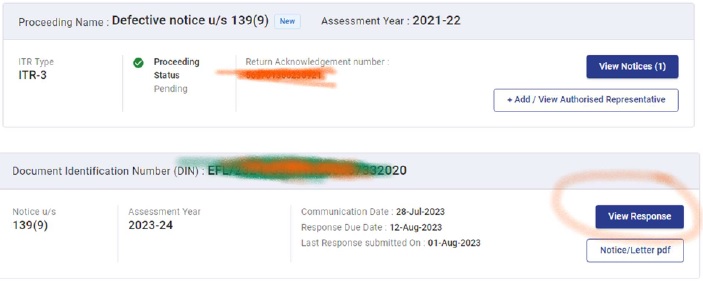

After that you will find the Notice like below:

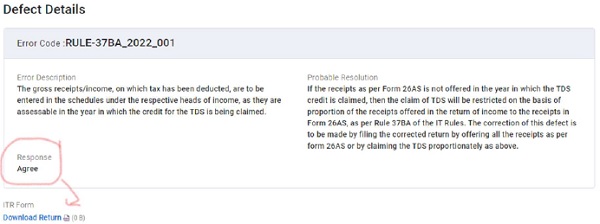

If you disagree then mention reply as like below

If agree, then upload revised returns after valid correction:

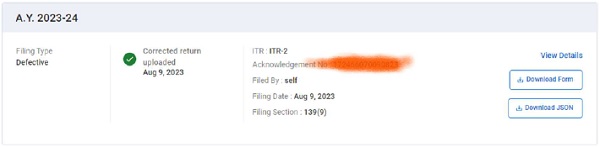

After Submission of the Response u/s 139(9).

Conclusion: Section 139(9) of the Income Tax Act offers a mechanism to rectify errors in filed returns. This guide empowers taxpayers to navigate the process effectively, ensuring accurate tax compliance. Professional assistance is recommended for complex cases. Avoid penalties by understanding and acting upon defective return notices promptly.

Note- It is advisable for taxpayers to seek professional guidance when dealing with complex rectification cases to ensure a smooth and successful resolution.

Author Bio