Karnataka State Chartered Accountants Association ® has submitted its Suggestions, views & comments on comprehensive changes in GSTR-3B vide its representation dated October 1st, 2022 to The GST Policy Wing, Central Board of Excise and Customs, New Delhi.

Relevant Text of Their Representation Is As Follows: –

Karnataka State Chartered Accountants Association ®

CA. Pramod Srihari

President

CA. Vijay Kumar M

Patel Secretary

Date: Saturday, October 1st, 2022

To,

The GST Policy Wing,

Central Board of Excise and Customs,

New Delhi

Dear Sir/Madam,

SUBJECT: Suggestions, views & comments on comprehensive changes in GSTR-3B

The Karnataka State Chartered Accountants Association (R) (in short ‘KSCAA’) is an Association of Chartered Accountants, registered under the Karnataka Societies Registration Act, in the year 1957. KSCAA is primarily formed for the welfare of Chartered Accountants and represents before various regulatory authorities to resolve the problems / hardships faced by Chartered Accountants and business community.

At the outset, we applaud your efforts not only in opening limitless possibilities to the country’s economic system by rolling out tax reforms, but also for taking up the task of making it a simpler one to comply with. The GSTR3B concept paper is a foot in this direction.

We wish to state that our members have been working in close liason with your office over the years. Through this representation, we intended to give our feedback and suggestion on GSTR3B concept paper. For every issue listed, we have highlighted challenges and have also suggested solutions to address them.

|

Sl |

Table Reference& Coverage |

Issue | Suggestion |

| 1 | Instructions – Sl. No. 2 Table 3 will capture information related to outward supplies and inward supplies liable to reverse charge: | Instructions in Para 2 on matters relating to Part A, lists table 4, 6, 8, 11 and proposed table 14 of Form GSTR 1 other than row (f) which will be partly auto-populated from FORM GSTR-2B and partly user entry.

However, said instruction has omitted reference to table 5 & 7 of Form GSTR 1, which contains B2C details. Clarity is needed that even B2C transactions (net of credit notes) should also be part of Part A. |

It is suggested to draw reference to table 5 & 7 in the instruction relating Table 3 the objective of Table 3 is to determine the total output liability for that particular month under GST laws |

|

|||

| 2 | Table 3, Part A, (f) | Inward supplies (liable to reverse charge)

(1) Import of services (Manual) (2) Others (Auto) |

Inward supplies (liable to reverse charge)

(1) Import of services (Manual) – No suggestion (2) Others (Auto) – Instead of Auto population, manual may be allowed for the following reasons a) Time of supply provisions for paying RCM liability is 60 days from date of invoice or the date of payment, whichever is earlier. However, auto-population to liability in GSTR 3B is based on GSTR 1 filing status by the supplier who is providing such supplies. In most of the situations, liability may arise based on time of supply provisions only in subsequent months and not in the month in which supplier has uploaded his GSTR 1. b) Unregistered dealer related supplies attracting RCM has to be manually entered. |

|

|||

| 3 | Table 3, Part A, (g) and (h)

|

(g) Supplies on which ECO is required to pay tax u/s 9(5) [To be furnished by ECO]

(h) Supplies made through ECO on which ECO is required to pay tax u/s 9(5) [To be furnished by the supplier]

|

The data here is for reporting purposes only and is auto populated with an option to edit. There could be scope for mistakes while reporting. It is suggested to move this to a separate table in GSTR3B to avoid confusion for others who may not deal in such transactions and not to club the same with Part A. Further, there should be an edit option to rectify if any error has crept in at the time of filing of GSTR 1

|

| 4 | Table 3, Part A, (k) | Advances received/Advances adjusted in the current tax period

Clarity is needed whether to report net value of advance received & adjustment OR whether both these are to be submitted separately as there is a separation in form of “/” is used between the terms received and adjusted. As the current usage in the concept paper is ambiguous

|

Either suitable inputs be provided through Instructions

OR Amend the Form to reflect each of the item separately i.e., Advances Received – Advances Adjusted in Current Tax Period (Positive Number Only Advances adjusted in current tax period (Negative Number Only) |

|

|||

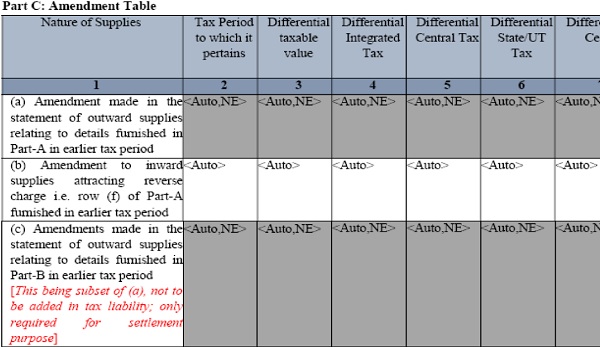

| 5 | Table 3, Part C, Amendment Table, (a) & (c) | Row (a) and (c) of Part C is noneditable data which will auto populates from GSTR-1. However, said row will not allow assessee to modify or change the figures even though there are clerical errors in GSTR-1. This will mandate assessee to accept error and file incorrect GSTR-3B. Further, it also leads to excess payment / short payment of GST. | Section 39(9) r/w CBIC vide circular No. 26/2017 dated 29-12-2017 provided guidelines for rectification of Error in GSTR 3B provides if any taxable person after furnishing a return discovers any omission or incorrect particulars therein, he can rectify such omission or incorrect particulars.

It is suggested make this row as editable. It would benefit the assessee to rectify the clerical mistake in the same month in which error occurs. |

|

|||

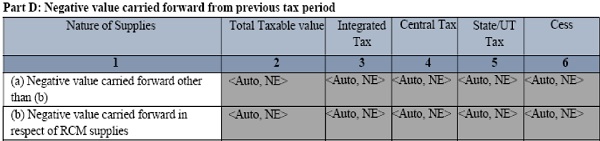

| 6 | Table 3, Part D: Negative value carried forward from previous tax period | As the table name suggests, non-editable negative values are carried forwarded only from the previous tax period.

It does not have a provision to carried-forward the accumulated negatives value from July 2017 up until the date the new form was implemented. |

It is suggested to include a row that reads, “Accumulated negative value carried over from July 2017 to the date the new form was implemented.”

This will make it clear how much negative value has been accumulated as of the implementation and how much has occurred since then. It allows effective tracking and reconciliation. It will also be helpful for the taxpayer and the department during reconciliation. |

| 7 | Table 4. Eligible and ineligible ITC | ITC related information for the current year and the prior year is currently reported in table 4(A)(5), “All Other ITC.” As GSTR-2B only contains data for the current month, the aforementioned table might not match ITC claims made by the assessee in past months.

A new transitional row could be included as to disclose and claim ITC-related prior periods. This will be useful during reconciliation for both the taxpayer and the department. |

GSTR 3B ought to feature a separate row for reporting transactions from the previous year. This can address a various reporting issue.

If assessee wants to report ITC related to FY 21-22 in GSTR 3B by September 2022 / by the time of implementation of new form, it is essential to have a separate row to disclose transactions from the previous tax period. This would resolve various reporting and auditing issues. Further, separate column like “Not belonging ITC” may be provided to report those entries which do not pertain to the person filing the retun. |

| 8 | Other Suggestion | – | 1) Foot-note/remarks column may be allowed in the form that can be used by the assesee. This is in line with the remarks column allowed in erstwhile regime.

2) Instructions may provide a clarity on appropriate table to be used for transactions which are out of GST levy and Schedule III covered transactions. 3) IGST Credits on import of goods are not auto-populating for few months in the recent past, which is creating a working capital issue for business. Seamless flow of credit into the GSTR 3B may be ensured. |

We are presenting before you the above-enumerated issues, challenges and wherever required, we have also given recommendations for your consideration.

We the members of Karnataka State Chartered Accountants Association, on behalf of the entire Chartered Accountants fraternity and also on behalf of the trade and industry appeal you to consider our above recommendations on various issues populated as above. GST intends to simplify tax compliance, and we believe that implementation of the above suggestions will take us a step closer towards achieving ‘Ease of doing Business’.

Yours sincerely,

For Karnataka State Chartered Accountants Association ®

CA PRAMOD SRIHARI

President

CA VIJAYKUMAR M PATEL

Secretary

CA SIDDESH NAGARAJ GADDI

Chairman Representation Committee

CC –

1. Nirmala Sitharaman, Hon’ble Minster of Finance

2. Basavraj Bommai, Hon’ble Chief Minister of Karnataka

3. The Commissioner of Commercial Taxes, State of Karnataka

4. The Principal Chief Commissioner of Central Tax, Karnataka