Introduction:

The Provisions relating to the form of appeal to Commissioner (Appeals) are contained under Rule 45 of the Income Tax Rules. As per the said rule 45, an appeal to the Commissioner of Income Tax (Appeals) needs to be made in Form No. 35.

Rule 45 of Income Tax Rules, 1962:

(1) An appeal to the Commissioner (Appeals) shall be made in Form No. 35.

(2) Form No. 35 shall be furnished in the following manner, namely:

(a) In the case of a person who is required to furnish return of income electronically under sub- rule (3) of rule 12,—

(i) By furnishing the form electronically under digital signature, if the return of income is furnished under digital signature;

(ii) By furnishing the form electronically through electronic verification code in a case not covered under sub-clause (i);

(b) In a case where the assessee has the option to furnish the return of income in paper form, by furnishing the form electronically in accordance with clause (a) of sub-rule(2) or in paper form.

(3) The form of appeal referred to in sub-rule (1), shall be verified by the person who is authorised to verify the return of income under section 140 of the Act, as applicable to the assessee.

(4) Any document accompanying Form No. 35 shall be furnished in the manner in which the said form is furnished.

- The method of verification of the return is specified in Rule 12 & varies depending on the nature of the assessee and the turnover/audit requirements.

| S.No. | Person | Condition | Manner of furnishing Return of Income |

| 1 | Individual or Hindu undivided family | · Accounts are required to be audited under section 44AB of the Act. | · Electronically under digital signature; |

| · Where total income assessable under the Act during the previous year of a person, being an individual of the age of eighty years or more at any time during the previous year, and who furnishes the return in Form number SAHAJ (ITR-1) or Form number SUGAM (ITR-4). | · Electronically under digital signature; or

· Transmitting the data electronically in the return under electronic verification code; or · Transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V; or · Paper form; |

||

| · In any other case | · Electronically under digital signature; or

· Transmitting the data electronically in the return under electronic verification code; or · Transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V; or |

||

| 2 | Company | · All Cases | Electronically under digital signature; |

| 3 | A person required to furnish the return in Form ITR-7 | · In case of a political party;

· In any other case |

· Electronically under digital signature; or

· Transmitting the data electronically in the return under electronic verification code; or · Transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V; or |

| 4 | Firm or limited liability partnership or any person (other than a person mentioned in Sl. 1 to 3 above) who is required to file return in Form ITR-5

|

· Accounts are required to be audited under section 44AB of the Act

· In any other case |

· Electronically under digital signature;

· Electronically under digital signature; or · Transmitting the data electronically in the return under electronic verification code; or · Transmitting the data in the return electronically and thereafter submitting the verification of the return in Form ITR-V; |

Steps to file Form 35:

1. Visit site https://www.incometaxindiaefiling.gov.in/home.

2. Already registered user click on ‘Login here’ and provide appropriate user id and password.

3. Navigate the following path – e-File > Income Tax Forms

4. Select Form Name as ‘FORM NO. 35 – Appeal’ from the drop-down list.

5. Select submission Mode as ‘Prepare and Submit Online’ from the drop- down list.

6. Select appropriate option as per the date of order.

Documents Required to file Form 35:

1) Scan Copy of Assessment order for the specific AY for which Form 35 Filing in PDF Format

2) Scan copy of Demand Notice for the specific AY for which Form 35 Filing in PDF Format.

- Ensure active Email Address & Mobile no. is entered in Form 35.

- Make a choice for correspondence i.e. through email or physical.(Yes/No)

Point No.1:

- All the details are mentioned in the copy of Assessment order only.

Point No. 2:

- All the details are mentioned in the copy of Assessment order only.

- Date of order means the date on which order is passed.

- Date of service and date of order can be different.

- Date of sevice of order/ notice of demand means the date on which the order or notice is received by assessee.

Point No. 3:![]()

- For the Income authority passing the order refer the Assessment Order copy.

Point No. 4

- Mention the details of all the pending appeals with CIT(A).

Point No. 5, 6 & 7:

- Almost all the appeals are covered in Section 246A.(Appeals related to TDS under Section 195 Appeal only covered in Section 248)

- Section 246A explains that the assessee can file appeal against the orders mentioned.

- Amount of Income assessed is the total Income assessed after the additions/disallowances. (Refer Computation Sheet attached with AO Order)

- Amount of Disputed Demand & Amount of Penalty disputed in Appeal (Refer Demand Notice as per Section 156)

Point No 8 & 9:

- In Point No. 8 for Acknowledgement No. & date of Filing refer Copy of ITR-V.

- In Point No. 8 for Total Tax Paid mention the Self-assessment Tax Paid.

- In point No. 9 mentioned the details of advance tax paid (Refer Advance Tax Challan).

- For point 8 & 9 Refer Section 249 of Income Tax Act, 1961.

Note: Always paid the taxes due on income tax returned before filing the appeal otherwise appeal is not admitted.

Point No. 10:

- When Appeal in Section 248 then only the point no.10 is applicable.

- Section 248:

Where under an agreement or other arrangement, the tax deductible on any income, other than interest, under section 195 is to be borne by the person by whom the income is payable (deductor), and such person having paid such tax to the credit of the Central Government, claims that no tax was required to be deducted on such income, he may appeal to the Commissioner (Appeals) for a declaration that no tax was deductible on such income.

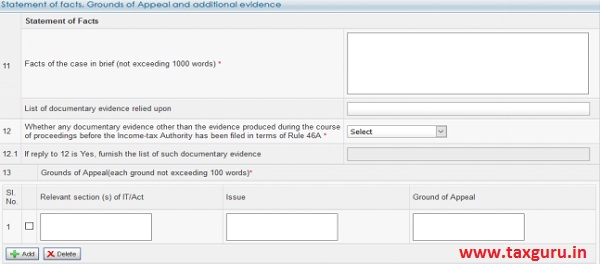

Point No. 11, 12 & 13:

Point 11:

- Statement of Facts should be descriptive and detailed.

- It should not be argumentative

- Basic details should be always given like ROI filed date, returned income, heads of income, about the assesse.

- Ensure to add only those facts which are disclosed in the assessment proceedings

- Add every minute details and facts with dates and sequence of how it happened in earlier proceedings.

- If too many grounds, better to classify Statements of Facts based on each ground taken up.

- Statement of facts must not exceed 1000 words

- Do not use special characters like (‘-’, ‘/’, ‘@’, ‘&’ etc.)

Point 12:

- It requires to mention reliance on any additional evidences.

- Specify if any evidences while filing form itself.

- Mention the same in Statement of Facts as well as why the same could not be submitted.

- Make a prayer to allow additional evidences in Grounds of Appeal

- Keep application under Rule 46A ready while filing the appeal itself.

- The Commissioner (Appeals) has a discretionary power to admit fresh or additional evidence subject to conditions in Rule 46A i.e.

a) The AO has refused to admit evidence which ought to have been admitted.

b) The assessee was prevented by sufficient cause from submitting the evidence in the assessment proceedings.

c) The AO has made assessment order without giving sufficient opportunity to the assessee.

Rule 46A:

The appellant shall not be entitled to produce before the Deputy Commissioner (Appeals)or, as the case may be, the Commissioner (Appeals), any evidence, whether oral or documentary, other than the evidence produced by him during the course of proceedings before the Assessing Officer, except in the following circumstances, namely :—

- where the [Assessing Officer] has refused to admit evidence which ought to have been admitted ; or

- where the appellant was prevented by sufficient cause from producing the evidence which he was called upon to produce by the Assessing Officer; or

- where the appellant was prevented by sufficient cause from producing before the Assessing Officer any evidence which is relevant to any ground of appeal; or

- where the Assessing Officer has made the order appealed against without giving sufficient opportunity to the appellant to adduce evidence relevant to any ground of appeal.

(2)No evidence shall be admitted under sub-rule (1) unless the Deputy Commissioner (Appeals) or, as the case may be, the Commissioner (Appeals) records in writing the reasons for its admission.

(3)The Deputy Commissioner (Appeals) or, as the case may be, the Commissioner (Appeals) shall not take into account any evidence produced under sub-rule (1) unless the Assessing Officer has been allowed a reasonable opportunity.

(a) To examine the evidence or document or to cross-examine the witness produced by the appellant, or

(b) To produce any evidence or document or any witness in rebuttal of the additional evidence produced by the appellant.

(4) Nothing contained in this rule shall affect the power of the Deputy Commissioner (Appeals) or, as the case may be, the Commissioner (Appeals) to direct the production of any document, or the examination of any witness, to enable him to dispose of the appeal, or for any other substantial cause including the enhancement of the assessment or penalty whether on his own motion or on the request of the Assessing Officer under clause (a) of sub-section (1) of section 251 or the imposition of penalty under section 271.

Point No. 13:

- Expected relief should be clearly mentioned.

- In case of more than one issues involved, preference of grounds should be decided.

- Avoid using long sentences.

- In case of opportunity of being heard not granted, the same should be clearly taken in grounds.

- All grounds needs to be adjudicated in the order so ensure that the grounds are not repetitive or too many.

- Grounds should be precise, concise, simple and without any ambiguity.

- Should be wide and not restrictive.

- Should not be argumentative.

- Avoid multiple grounds for single issue unless every ground is distinct.

- Always add prayer at the end with specific requests.

- Last ground should be to grant leave to add, amend, withdraw any ground.

- Use of clear and simple language and avoid jargons.

- Nature of dispute and relief expected should be highlighted.

- Grounds of appeal must not exceed 100 words per ground.

- It is required to mention the relevant Section under which the addition/ disallowance has been made.

Point No. 14, 15 & 16:

Point No. 14 & 15:

- As per Section 249(2) an appeal shall be filed within 30 days from the date of service of notice of demand when appeals related to any assessment or penalty.

- As per Section 249(2) an appeal shall be filed within 30 days from the date of payment of the tax when appeals related to Section 248.

- If there is delay in filing then enter grounds for condonation of Delay.

- Grounds for Condonation of Delay must not exceed 500 words.

- Eg: If there is any medical reason for delay in filing appeal then attach Affidavit along with medical certificate.

Point 16:

- As per Section 249 Appeal fees are as follows:

| S.No. | Particulars | Appeal Fees |

| A. | Total income of the assessee as computed by the Assessing Officer ≥ Rs.1,00,000/- | Rs. 250/- |

| B. | Total income of the assessee as computed by the Assessing Officer >Rs.1,00,000/- & ≤ Rs. 2,00,000/- | Rs. 500/- |

| C. | Total income of the assessee as computed by the Assessing Officer >Rs. 2,00,000/- | Rs. 1,000/-

|

| D. | If subject matter of an appeal not Covered in A,B and C | Rs 250/- |

- Details of challan for appeal fees paid should be correctly filled. (eg. BSR Code, Date of payment, Challan Serial No., Amount of Challan etc.)

****

Author: Sahil Dhingra | Sahildhingra9697@gmail.com | 7042226920

Author Bio

In the Attachments Section of Form 35, an error message is displayed below the file name after attaching the file. Hence I am not able to save that page and file Form 35. How do I find out the reason for the error message?