Yashish Sharma

Whenever a group of people are discussing about taxation, the first question that comes to our mind about any Income Tax section is “whether is it applicable on me?” This article will be beneficial for you in case you want information on taxation on foreign companies. The Finance Act 2015 amended the test of residence of companies by inserting a concept called “Place of Effective Management (POEM)”. Let us first find out what the section tells us and then let’s interpret it.

Section 6(3) of Income Tax Act, 1961 – Prior to Finance Act, 2015

‘A company is said to be resident in India in any previous year, if

√ It is an Indian company; or

√ During that year, the control and management of its affairs is situated wholly in India.

Section 6(3) of Income Tax Act, 1961 – As per Finance Act, 2015

‘A company is said to be resident in India in any previous year, if

√ It is an Indian company; or

√ It’s place of effective management, at any time in that year, is in India.

Why was this required?

a) The erstwhile provision required to have a company to have its entire control and management in India. This meant that the companies could avoid being classified as resident if one of its board meetings are held outside India. Thus, it provided an opportunity for the companies to avoid tax by shifting or organising some of its events outside India.

b) The initial provision facilitated the creation of shell companies outside India which in reality were controlled from India. The amendment brought such shell companies into the tax bracket using the concept of ‘POEM’.

c) This tax evasion was pretty much seen in the decision of Delhi Tribunal in the case of Radha Rani Holdings v ACIT.

Meaning and Determination of POEM

“Place of effective management” (POEM) has been defined to mean a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made.

POEM has to be determined on year to year basis. It can be determined on the basis of the below mentioned categories:

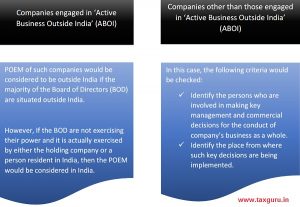

Concept of ‘Active Business Outside India’ (ABOI)

A company shall be said to be engaged in “active business outside India” if

√ its passive income is not more than 50% of its total income; and

√ less than 50% of its total assets are situated in India; and

√ less than 50% of the total number of employees are situated in India or are resident in India; and

√ the payroll expenses incurred on such employees is less than 50% of its total payroll expenditure.

For the purpose of determining whether an entity is engaged in ABOI or not, the average data of the previous three years should be considered. For example, if POEM is determined for AY 2020-21, i.e., FY 2019-20, then average data of FY 2018-19, FY 2017-18 and FY 2016-17 are to be considered. If in case the company has been in existence for less than three years, then the average data of the period for which the company has been in existence will be considered.

Examples of Active Business Outside India (ABOI)

Case 1:

A Co., incorporated in country X, is a wholly owned subsidiary of Indian company B. Details of Co. A include the following:

- The warehouses & stock are the only assets of A Co. & are located in country X.

- All the employees are also in Country X.

- The average income wise breakup of the company’s total income for 3 years is:

(i) 30% – Purchases from non-associated enterprise & sales to associated enterprise.

(ii) 30% – Both purchases and sales from/to associated enterprise

(iii) 30% – Purchases from associated enterprise & sales to non-associated enterprise.

(iv) 10% – Interest Income.

Therefore, in this case, since the passive income is 40% i.e. not more than 50%, taking into consideration points (ii) & (iv), Co. A is engaged in ABOI.

Case 2:

In this case, an Indian parent company A has 3 wholly owned subsidiaries as follows:

(i) B and Co. C incorporated in Country X.

(ii) D incorporated in Country Y.

- Co. A receives income from its subsidiaries only by way of dividend and interest from an investment.

- POEM of Co. A is in India.

- The subsidiaries are engaged in ABOI and majority of the BOD meetings are held in their respective countries of incorporation.

Therefore, merely because of the POEM of the holding company is in India, the POEM of all of its subsidiaries cannot be taken to be in India. Since the subsidiaries are engaged in ABOI and also the majority of the board meetings are held in their respective countries, POEM shall be presumed to be outside India.

CONCLUSION

Like every good pill has its side effects, the concept of POEM also has it’s negative impact on some entities who genuinely are operating from outside India. Though the said provisions have tried to capture the entities operating from India but having no substance outside India, but still there is a long way to go.

(Author is associated with ‘International Business Advisors, Delhi’ as Analyst-Direct Tax.)

is it also apply on companies , which are not in nature of holding & subsidiary for example Mr A a resident of India incorporate a company in Canada ie stand alone company in Canada does POEM would be applicable to him?

is there is limit of 50crores for applicability of POEM?