♦ Export of goods means taking goods out of India to a place outside India (Sec 2(5) of IGST Act)

♦ Export of services means the supply of any service when:

- the supplier of service is located in India;

- the recipient of service is located outside India;

- the place of supply of service is outside India;

- the payment for such service has been received by the supplier of

- service in convertible foreign exchange; and

- the supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in Section 8 of IGST Act

♦ Section 16 of the IGST Law defines “zero rated” supply which means export of goods or services or both and it includes supply of goods and services to Special Economic Zone (SEZ).

♦ Section 16 of the IGST Law defines “zero rated” supply which means export of goods or services or both and it includes supply of goods and services to Special Economic Zone (SEZ).

♦ Regarding zero rated supply the procedures are prescribed and according to which the goods can be exported either without payment of IGST and the unutilized Input Tax Credit (ITC) can be refunded. Another way is that the exporter may supply goods or services or both on payment of integrated tax and claim refund in accordance with the provisions of Section 54 of the CGST Act, 2017 and the rules made their under.

♦ Regarding the first option, the exporter claiming the refund of unutilized Input Tax Credit will filed an application through the common portal and the same shall be accompanied by the documents prescribed i.e. copy of invoice, shipping bill, BRC etc.

♦ Regarding the second option the copy of the shipping bills shall be deemed to be an application for the refund of the IGST and the applicant will have to furnish a valid return in FORM GSTR-3 from the common portal.

♦ In the new regime new format of shipping bill is required to be filled considering the IGST Law. However ARE-1 procedure which was followed in earlier tax regime is dispensed with.

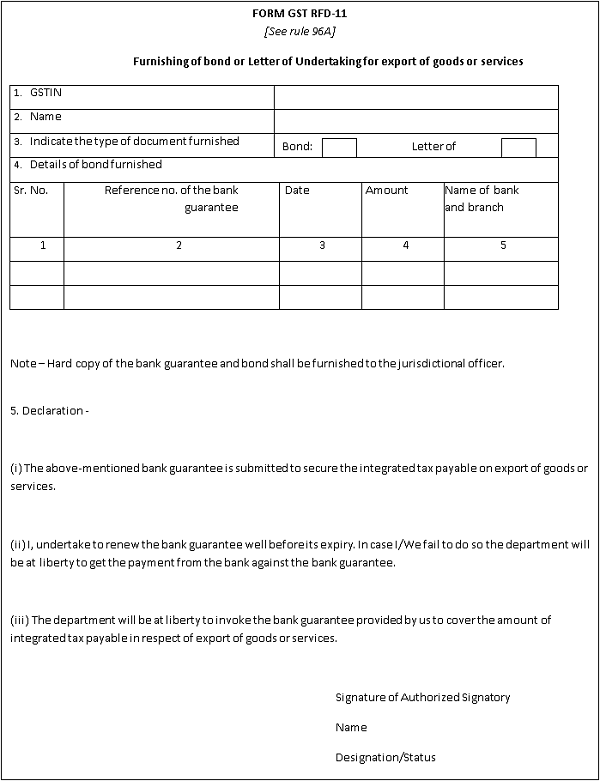

♦ As per rule 96A of the CGST Rules, 2017 any registered person exporting goods or services or both without payment of integrated tax is required to furnish a bond or a Letter of Undertaking (LUT) in FORM GST RFD-11.

|

Extract of Rule 96A is as follows:- Rule 96A: Refund of integrated tax paid on export of goods or services under bond or Letter of Undertaking: – 1. Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export, a bond or a Letter of Undertaking in FORM GST RFD-11 to the jurisdictional AC/DC, binding himself to pay the tax due along with the interest specified under sub-section (1) of section 50 within a period of — a. 15 days after the expiry of 3 months from the date of issue of the invoice for export, if the goods are not exported out of India; or b. 15 days after the expiry of 1 year, or such further period as may be allowed by the Commissioner, from the date of issue of the invoice for export, if the payment of such services is not received by the exporter in convertible foreign exchange. 2. The details of the export invoices contained in FORM GSTR-1 furnished on the common portal shall be electronically transmitted to the system designated by Customs and a confirmation that the goods covered by the said invoices have been exported out of India shall be electronically transmitted to the common portal from the said system. 3. Where the goods are not exported within the time specified in sub-rule (1) and the registered person fails to pay the amount mentioned in the said sub-rule, the export as allowed under bond or Letter of Undertaking shall be withdrawn forthwith and the said amount shall be recovered from the registered person in accordance with the provisions of section 79. 4. The export as allowed under bond or Letter of Undertaking withdrawn in terms of sub-rule 3 shall be restored immediately when the registered person pays the amount due. 5. The Board, by way of notification, may specify the conditions and safeguards under which a Letter of Undertaking may be furnished in place of a bond. 6. The provisions of sub rule (1) shall apply, mutatis mutandis, in respect of zero-rated supply of goods or services or both to a Special Economic Zone developer or a Special Economic Zone unit without payment of integrated tax. |

♦ Furnishing of Bond/ Letter of Undertaking (LUT) in FORM GST RFD-11

Any registered person availing the option to supply goods or services for export without payment of integrated tax shall furnish, prior to export, a bond or a Letter of Undertaking. This bond or Letter of Undertaking is required to be furnished in FORM GST RFD-11 on the common portal, binding himself to pay the tax due along with the interest specified under sub-section (1) of section 50 within a period of:

a. 15 days after the expiry of 3 months from the date of issue of the invoice for export, if the goods are not exported out of India; or

b. 15 days after the expiry of 1 year, or such further period as may be allowed by the Commissioner, from the date of issue of the invoice for export, if the payment of such services is not received by the exporter in convertible foreign exchange.

Please note-

1. Exporter need not submit separate bond for each consignment / export and shall furnish a running bond, in case he is required to furnish a bond, in FORM GST RFD -11.

2. The bond would cover the amount of tax involved in the export based on estimated tax liability as assessed by the exporter himself.

♦ Withdrawal of bond/ LUT

If the goods are not exported within the specified time and the registered person fails to pay the mentioned amount, the export as allowed under bond or Letter of Undertaking shall be withdrawn forthwith and the said amount shall be recovered from the registered person accordingly.

♦ Restoration of bond/ LUT

The bond/ LUT which are withdrawn shall be restored immediately when the registered person pays the amount due.

♦ To whom the bond/ LUT is required to be furnished

As per Rule 96A, exporter shall be required to furnish bond/ Letter of undertaking to jurisdictional Deputy/Assistant Commissioner till the administrative mechanism for assigning of taxpayers to respective authority is implemented.

♦ Bond/ LUT can be furnished manually also

As per Rule 96A, bond/ LUT may be furnished manually to the jurisdictional Deputy/Assistant Commissioner in the format specified in FORM RFD-11 till the module for furnishing of FORM RFD-11 is available on the common portal.

◊ LETTER OF UNDERTAKING (LUT)

♦ Eligibility of Furnishing LUT

Not every registered person supplying goods or services for exports are eligible for furnishing LUT. Following registered person shall be eligible for submission of Letter of Undertaking in place of a bond:

i. Status Holder: A registered person shall be a status holder as specified in paragraph 5 of the Foreign Trade Policy 2015- 2020; or

ii. Received due foreign inward remittances (minimum 10%): A registered person who has received the due foreign inward remittances amounting to a minimum of 10% of the export turnover which should not be less Rs 100, 00,000 in the preceding financial year.

iii. Not prosecuted for any offence: A registered person shall not be prosecuted for any offence under the Central Goods and Services Tax Act, 2017 (12 of 2017) or under any of the existing laws in case where the amount of tax evaded exceeds Rs. 2,50,00,000.

Please note that those who does not satisfy above mentioned conditions, would submit bond.

♦ List of documents required to furnish LUT

i. Copy of Status Holder certificate issued by DGFT/ Development Commissioner

ii. Bank FIRC of 10% of the export turnover which should not less than 1 crore in financial year

iii. Letter of Undertaking to be executed on letter head- to be provided in duplicate; (also to be signed by witnesses)

iv. Declaration required that the registered has not been prosecuted for any offence involving tax, where the tax evaded is above Rs. 250 lakhs;

v. GSTIN certificate copy;

vi. Proof to indicate principle place of business- preferably copy of application for registration for GST;

vii. FORM RFD- 11 to be provided in duplicate;

viii. If the taxpayer is a public or private limited company than board resolution for appointment of Authorized signatory is required.

♦ Who shall execute the LUT

The Letter of Undertaking shall be furnished in duplicate for a financial year in the annexure to FORM GST RFD – 11 and it shall be executed by the working partner, the Managing Director or the Company Secretary or the proprietor or by a person duly authorised by such working partner or Board of Directors of such company or proprietor on the letter head of the registered person.

♦ Validity of LUT

Letter of undertaking shall be valid for 12 months.

♦ What if an exporter fails to comply with the conditions of LUT

If an exporter fails to comply with the conditions of the LUT he may be asked to furnish a bond. Exports may be allowed under existing LUTs/Bonds till 31st July 2017.

◊ BOND

♦ Running bond or One time bond

Now the question arises as to what kind of a bond is to be furnished. It is observed consignment wise bond would be a significant compliance burden on the exporters. It is directed that the exporters shall furnish a running bond (with debit / credit facility), instead of one-time bond (separate bond for each consignment / export), in case he is require to furnish a bond, in FORM GST RFD -11. The bond would cover the amount of tax involved in the export based on estimated tax liability as assessed by the exporter himself. The exporter shall ensure that the outstanding tax liability on exports is within the bond amount. In case the bond amount is insufficient to cover the tax liability in yet to be completed exports, the exporter shall furnish a fresh bond to cover such liability.

♦ Furnishing of bank guarantee

Rule 96A of CGST requires to furnish bank guarantee with bond. Field formations have requested for clarity on the amount of bank guarantee as a security for the bond.

♦ Furnishing of bond on Non- Judicial Stamp paper

The bond shall be furnished on non- judicial stamp paper of the value as applicable in the State in which bond is being furnished.

♦ What shall be the amount of Guarantee?

In this regard it is directed that the jurisdictional Commissioner may decide about the amount of bank guarantee depending upon the track record of the exporter. If Commissioner is satisfied with the track record of an exporter then furnishing of bond without bank guarantee would suffice. In any case the bank guarantee should normally not exceed 15% of the bond amount.

Exporters shall submit the LUTs/bond in the revised format latest by 31st July, 2017.

Click here to know about GSTR 3B

Conclusion

With the Introduction of Rule 96A Exporters can export Goods &Services by Paying IGST on the same and can claim refund after paying the same or can Export the same without payment of IGST under Undertaking or Bond.

|

Bond for export of goods or services without payment of integrated tax I/We ……………… of ………………,hereinafter called “obligor(s)”, am/are held and firmly bound to the President of India (hereinafter called “the President”) in the sum of rupees to be paid to the President for which payment will and truly to be made. I/We jointly and severally bind myself/ourselves and my/our respective heirs/ executors/ administrators/ legal representatives/successors and assigns by these presents; Dated this day ………………of ……………… ; WHEREAS the above bounden obligor has been permitted from time to time to supply goods or services for export out of India without payment of integrated tax; and whereas the obligor desires to export goods or services in accordance with the provisions of clause (a) of sub-section (3) of section 16; AND WHEREAS the Commissioner has required the obligor to furnish bank guarantee for an amount of rupees endorsed in favour of the President and whereas the obligor has furnished such guarantee by depositing with the Commissioner the bank guarantee as afore mentioned; The condition of this bond is that the obligor and his representative observe all the provisions of the Act in respect of export of goods or services, and rules made thereunder; AND if the relevant and specific goods or services are duly exported; AND if all dues of Integrated tax and all other lawful charges, are duly paid to the Government along with interest, if any, within fifteen days of the date of demand thereof being made in writing by the said officer, this obligation shall be void; OTHERWISE and on breach or failure in the performance of any part of this condition, the same shall be in full force and virtue: AND the President shall, at his option, be competent to make good all the loss and damages, from the amount of bank guarantee or by endorsing his rights under the above-written bond or both; I/We further declare that this bond is given under the orders of the Government for the performance of an act in which the public are interested; IN THE WITNESS THEREOF these presents have been signed the day hereinbefore written by the obligor(s).

Accepted by me this…………..day of………..(month)…………… (Year)

………………………of …………………………………… (Designation) for and on behalf of the President of India |