Month: April 2026

1,943 articlesGoods and Services Tax

Goods and Services Tax

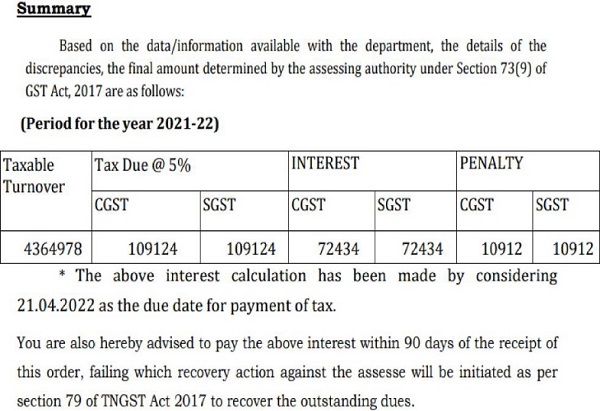

Separate SGST & CGST Penalty Invalid as It Exceeds Statutory Section 125 Limit

Goods and Services Tax

Goods and Services Tax

GST Raw Milk Exemption Dispute: From ASMT-10 to DRC-07

Finance

Finance

Loan Fraud & Regulatory Lapses: Gaps in India’s Financial Framework

Finance

Finance

Holding-Subsidiary Structures in Project Finance: Debt Parking Strategy

Goods and Services Tax

Goods and Services Tax

GSTAT: Practice And Procedure (Appellate Remedies Part-III)

Goods and Services Tax

Goods and Services Tax

GST Place of Supply Change for Intermediary Services from 30 March 2026

Income Tax

Income Tax

Bombay HC Quashes Reassessment for Invalid Section 151 Approval

Income Tax

Income Tax

CSR Reassessment & 80G Denial Based Only on Audit Objection Invalid: Bombay HC

Corporate Law

Corporate Law

FSSAI Updates Analyst List as Multiple Entries Added and Earlier Entries Omitted

Custom Duty

Custom Duty