Month: December 2025

2,753 articlesGoods and Services Tax

Goods and Services Tax

CBI Arrests CGST Superintendent in Mumbai while accepting Rs. Five Lakh Bribe

Fema / RBI

Fema / RBI

RBI Defers Phase 2 of Continuous Cheque Clearing

Goods and Services Tax

Goods and Services Tax

GSTR-9C Annual Reconciliation Statement (Self-Certified Statutory Obligation)

Corporate Law

Corporate Law

Claim Unpaid Dividends & Physical Shares in India: Step-by-Step Process

Income Tax

Income Tax

ITAT Allows TDS credit although corresponding income declared by Sister concern

Goods and Services Tax

Goods and Services Tax

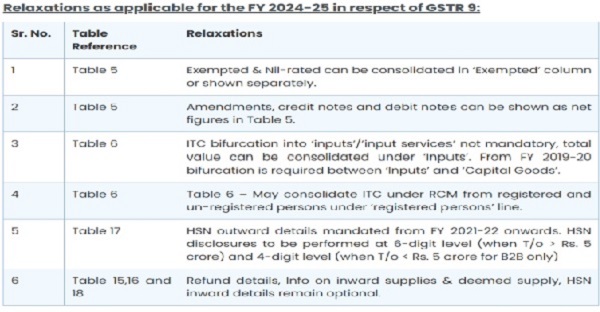

GSTR-09-Guide: Incorporating Latest Changes and FAQs

Goods and Services Tax

Goods and Services Tax

Different Types of Assessments under GST

Custom Duty

Custom Duty

Customs Litigation in 2025: Key Judicial Trends Every Importer & Practitioner Must Note

CA, CS, CMA

CA, CS, CMA

Guide: How to Conduct Stock Audits Effectively

Corporate Law

Corporate Law